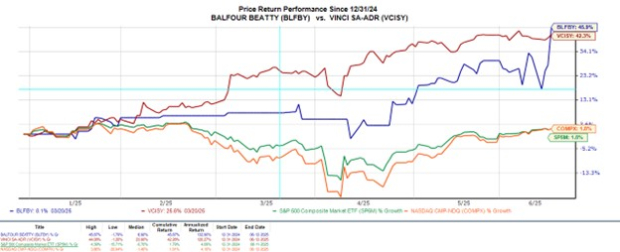

Balfour Beatty (BLFBY) and Vinci (VCISY), both Zacks Rank #1 stocks in the construction and infrastructure sectors, have outperformed the broader market this year, with ADRs soaring over 40%. Strategic expansions, including Balfour Beatty's acquisition of River Pointe and Vinci's acquisition of Peters Bros Construction, have boosted investor sentiment; furthermore, both companies trade at forward P/E ratios below the S&P 500 average and offer attractive dividend yields of 2.58% and 3.97%, respectively, with EPS estimates rising for fiscal years 2025 and 2026.

Balfour Beatty (BLFBY) and Vinci (VCISY) are presented as highly attractive investment opportunities within the construction and infrastructure sectors, particularly noteworthy as the industry enters its peak summer season. Both companies carry a Zacks Rank #1 (Strong Buy) and an overall "A" Zacks Style Scores grade, reflecting strong fundamentals across value, growth, and momentum. Their American Depository Receipts (ADRs) have demonstrated significant market outperformance, soaring over 40% year-to-date, substantially exceeding the broader indexes' 2% returns. This performance is underpinned by strategic expansion efforts, such as Balfour Beatty's May acquisition of River Pointe, a 300-unit multifamily community in Texas, and Vinci's recent acquisition of Peters Bros Construction, strengthening its presence in Western Canada. Despite these substantial gains, both BLFBY and VCISY trade at forward price-to-earnings (P/E) ratios below 15X, offering a considerable discount compared to the S&P 500's 23.2X. Crucially, annual earnings estimates for both companies are trending upwards; Balfour Beatty's fiscal 2025 EPS estimates rose 2% in the last week, with FY26 estimates up 4%, projecting a 9% earnings rise this year and a further 14% spike in FY26 to $1.36 per share. Vinci's FY25 and FY26 EPS estimates have increased by over 6% in the last 60 days, with FY26 earnings projected to grow 13% to $2.75 per share, following an anticipated flat FY25 at $2.42 EPS. Furthermore, robust operational performance has enabled both companies to offer attractive dividend yields, with Balfour Beatty at 2.58% and Vinci at 3.97%, both significantly higher than the benchmark average of 1.23%.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

extremely positive

Sentiment Score

0.90

Ticker Sentiment