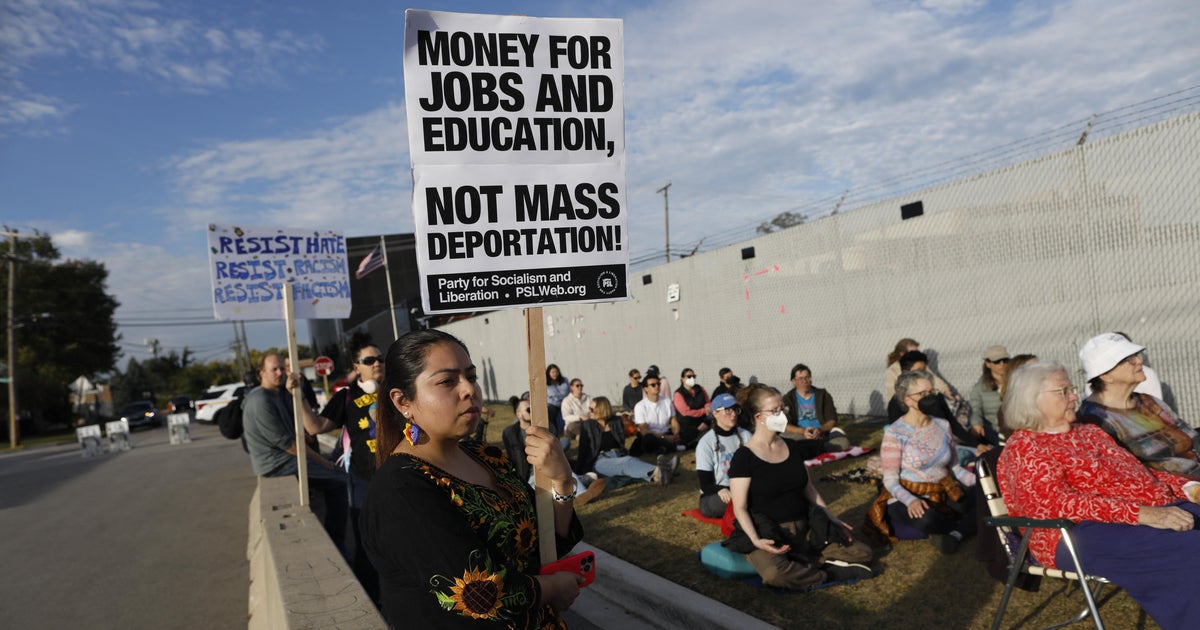

A U.S. district judge in Massachusetts ruled the Trump-era Department of Homeland Security policy permitting 'third-country' removals without prior notice or an opportunity to object unlawful and set it aside, pausing the order for 15 days to allow an appeal. The decision — stemming from a class-action and citing specific incidents involving removals to Mexico, El Salvador and an attempted transfer to South Sudan/Djibouti — constrains deportation operations, raises procedural and legal risks for DHS, and preserves the requirement to provide notice and an opportunity to raise fear-based claims while the appeals process continues.

Market structure: The ruling directly pressures private detention providers (CoreCivic CXW, GEO Group GEO) and ICE-charter logistics by increasing legal and operational uncertainty; if injunctions harden, utilization of detention beds could fall 10–30% over 3–12 months, compressing pricing power for contract renewals. Competitive dynamics shift dollars from bed-based detention to litigation, asylum processing, and non-detention enforcement tools (surveillance, data analytics), benefiting vendors who sell software/managed services to DHS rather than brick-and-mortar operators. Risk assessment: Near-term (days) the story is legal noise — a 15‑day appeal window creates volatility; short-term (weeks–months) outcomes hinge on appellate stays or Supreme Court intervention, with a plausible 20–50% chance of reversal that would reflate private‑prison revenues. Hidden dependencies include foreign-state guarantees, DHS contracting authorities and upcoming federal budgets; a political shift after elections could flip enforcement policy quickly (quarterly to multi-year impact). Trade implications: Expect elevated implied volatility in CXW/GEO options and widening credit spreads for high‑yield paper tied to detention firms; allocate volatility trades around 3–6 month legal milestones. Sector rotation should trim exposure to corrections/detention and modestly reallocate to defense IT/surveillance primes (LHX, L3Harris) and to specialist legal/consulting franchises that will win remediation contracts. Contrarian angles: Consensus short‑term negative view on private prisons may be overstated because past court reversals and emergency stays (e.g., prior Supreme Court signals) have produced snap rebounds; if government pivots to domestic detention or emergency chartering, regional airlines and temporary housing vendors can see a 10–20% revenue lift. Unintended consequence: persistent litigation raises DHS procurement spend, benefiting niche contractors while keeping CXW/GEO revenue lumpy and politically risky.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

-0.10