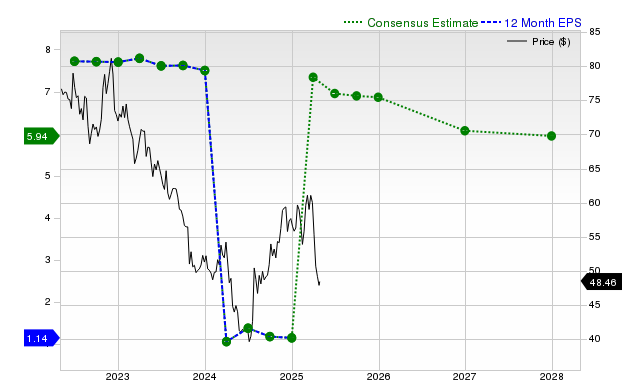

Bristol Myers Squibb (BMY) is a trending stock that has underperformed recently, with shares down 6.5% over the past month against the S&P 500's 2.9% gain. Despite this, the biopharmaceutical company has consistently surpassed consensus EPS and revenue estimates for the last four quarters. While current fiscal year EPS is forecast to jump significantly (+465.2%), subsequent periods show projected declines in both EPS and revenue, contributing to a Zacks Rank #3 (Hold) and a valuation that suggests it trades at a discount to peers.

Bristol Myers Squibb (BMY) presents a conflicting fundamental picture, characterized by significant recent stock underperformance juxtaposed with a history of strong operational execution. Over the past month, the stock has declined 6.5%, lagging both the S&P 500's 2.9% gain and its industry's 0.8% loss. This price action contrasts with the company's track record of beating consensus EPS and revenue estimates for the last four consecutive quarters, including a notable +36.45% EPS surprise and a +7.66% revenue surprise in its most recent report. However, forward-looking estimates are the primary source of concern. While the current fiscal year's consensus EPS is projected to rise an anomalous 465.2%, subsequent forecasts turn negative. For the current quarter, analysts expect an 8.3% year-over-year EPS decline and a 1% revenue contraction. More importantly, projections for the next fiscal year indicate a 6.6% drop in EPS and an 8.4% decline in revenue. This deteriorating outlook, despite stable analyst estimates over the past 30 days, has led to a neutral Zacks Rank #3 (Hold) but also contributes to a Zacks Value Style Score of 'A', suggesting the stock is trading at a discount to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.10

Ticker Sentiment