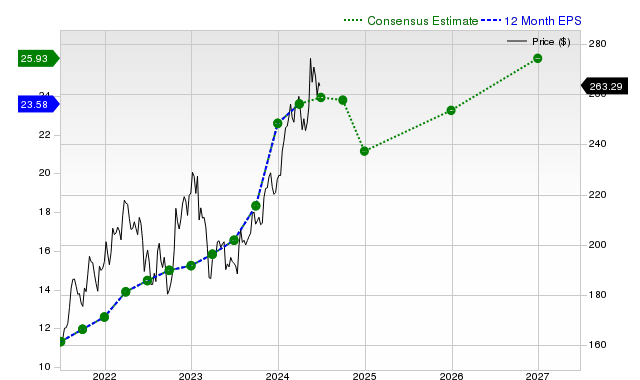

Chubb (CB) shares gained +1.9% over the past month, trailing the S&P 500 but exceeding its P&C insurance industry. Analysts project a slight EPS decline for the current fiscal year, followed by robust +17.7% growth in the next, alongside consistent revenue expansion and a track record of beating EPS estimates. Despite a Zacks Rank #3 (Hold) suggesting market-aligned near-term performance, Chubb holds a Zacks Value Style Score of "B," indicating it trades at a discount to peers.

Chubb Limited (CB) presents a mixed fundamental picture, characterized by near-term earnings pressure but a more favorable long-term outlook and valuation. The stock's +1.9% return over the past month has underperformed the S&P 500 composite's +2.7% gain, though it has slightly outpaced its Zacks Insurance - Property and Casualty industry peers (+1.0%). Analyst consensus projects a contraction in earnings for the current quarter and fiscal year, with year-over-year declines of -3.7% and -4.2% respectively. However, this is expected to be followed by a significant rebound, with next fiscal year's EPS forecast to grow by +17.7%. This earnings trajectory is underpinned by steady top-line growth, with revenue projected to increase by +5.7% this year and +6.4% next year. The company has a strong execution history, having beaten consensus EPS estimates in each of the last four quarters, including a +4.24% surprise in the most recent report. Despite the near-term headwinds reflected in its Zacks Rank #3 (Hold), the stock's valuation appears attractive, as indicated by a Zacks Value Style Score of 'B', suggesting it is trading at a discount to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.15

Ticker Sentiment