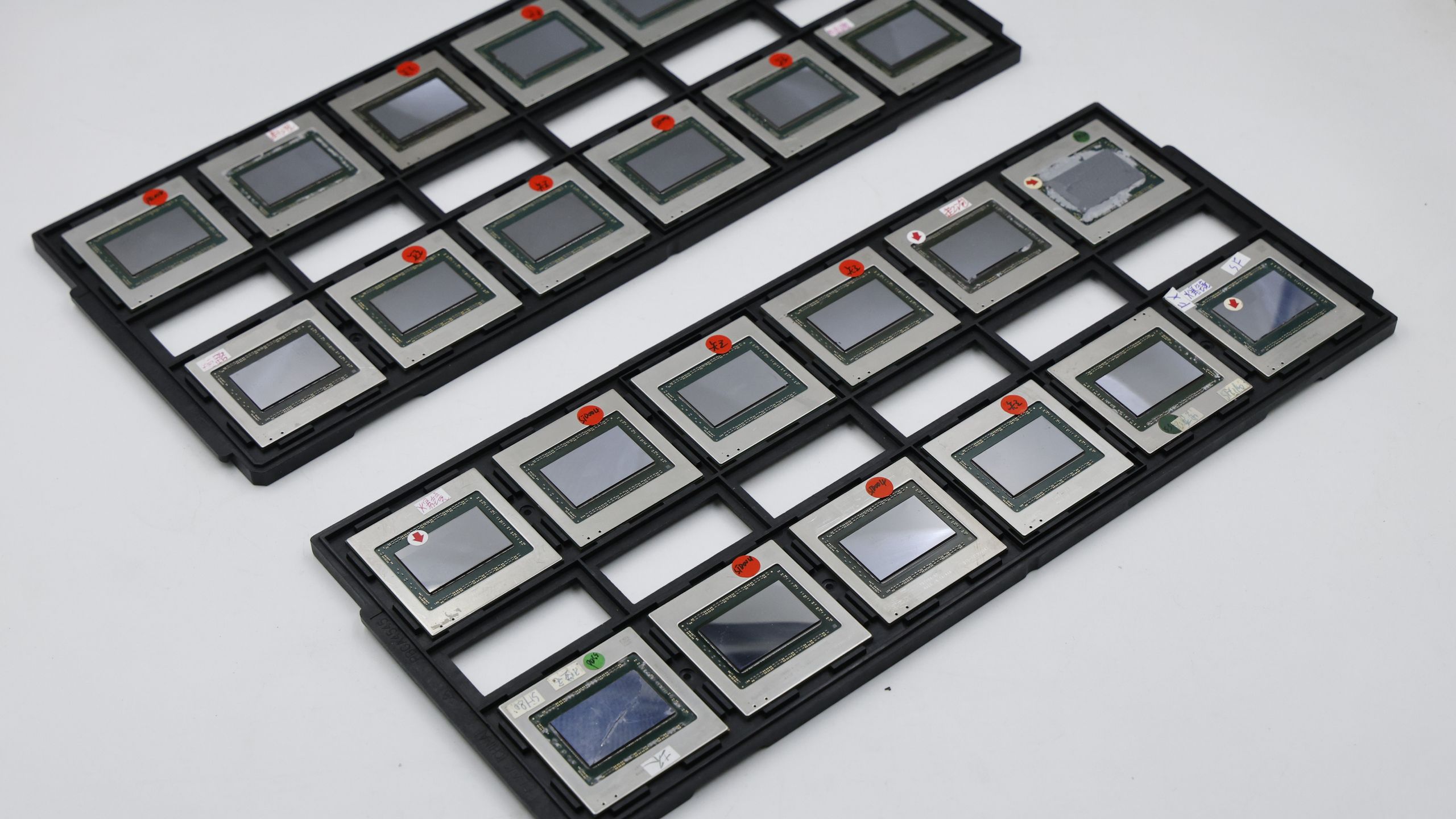

Zephyr, a Chinese GPU brand, confirmed it has RMA'd and replaced numerous dead RDNA 2 (Navi 21 / RX 6000 series) GPU dies that exhibited cracking, bulging or electrical shorting and publicly displayed the failed dies; the company says it will continue to honor warranty claims even for visibly damaged cores. While Zephyr’s disclosure underscores quality and warranty costs and revives questions about a 2022–23 failure uptick (previously attributed by a retailer to crypto-era use and high-humidity storage), the issue appears limited in scale but raises reputational and potential warranty-liability considerations for board partners and aftermarket sellers rather than immediate broad-market risk.

Market structure: This episode benefits brands that aggressively honor warranties (Zephyr-style) and manufacturers of new-generation GPUs who can pick up demand as buyers avoid suspect second‑hand RDNA2 units; used‑GPU marketplaces (eBay) are the direct losers, likely seeing a 5–15% transient drop in RX 6000 listings/volume over 1–3 months. Competitive dynamics: AIBs that absorb RMA costs will see margin pressure (est. $5–50m per mid‑tier AIB depending on installed base) while large OEMs with stronger service franchises gain pricing power for new SKUs over the next 6–12 months. Risk assessment: Tail risk is a broader manufacturing/class‑action cascade (probability <5% but could cost AMD/AIBs hundreds of millions and trigger regulatory scrutiny within 6–18 months). Immediate risk (days) is social‑media amplification that depresses used‑GPU prices; short‑term (weeks/months) is warranty accruals hitting Q/Q results; long‑term (12–24 months) is modest reputational erosion (1–2% share shift) if root causes aren’t resolved. Hidden dependency: humidity/packaging or substrate supplier faults could propagate to other GPU generations, creating correlated supplier contagion. Trade implications: Favor long exposure to companies that sell new GPUs and services (NVDA) using defined‑risk call spreads over 1–3 months while hedging/shorting used‑market exposure (EBAY) via put spreads; avoid outright large shorts against AMD unless you see >6% price move tied to concrete warranty charges. Options: implement small-ticket (1–3% NAV) call spreads on NVDA (3‑month) and put spreads on EBAY (3‑month) to express asymmetry; rotate away from pure-play used-market retail into semicap/IDM names. Contrarian angle: The consensus overstates systemic risk — Zephyr reports suggest failure is concentrated (rate ~1%/yr cited) and remediation is feasible, so any broad selloff is likely overdone. Historical parallels (past GPU reliability scares) show short‑lived price impact; set buy thresholds (e.g., AMD or AIBs down >6% on warranty news) to add long, and watch warranty accrual disclosures over next 60–90 days as the primary catalyst to re‑rate pricing.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment