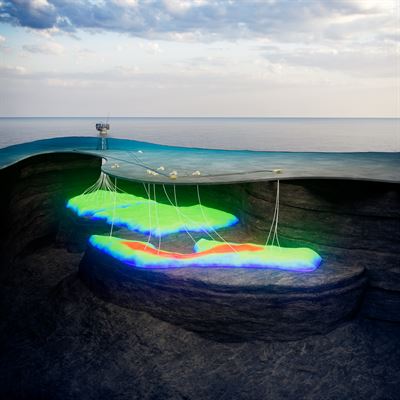

Aker BP has started production from Solveig Phase 2 in the North Sea, a subsea tie-back to the Edvard Grieg platform, delivering the project on schedule and within budget and adding approximately 39 million barrels of oil equivalent in recoverable resources. The development comprises three wells and is expected to extend plateau production while using existing Edvard Grieg capacity; Aker BP holds a 65% working interest with OMV Norge (20%) and Harbour Energy Norge (15%) as partners. Key suppliers included TechnipFMC, Moreld Apply, Odfjell Drilling and Halliburton, underscoring efficient execution and modestly positive near-term asset and production outlook for Aker BP.

Market structure: Aker BP (AKRBP) is the clear direct winner — Solveig Phase 2 adds ~39 mmboe of recoverable resources (~25.35 mmboe to AKRBP at 65% WI) and uses existing Edvard Grieg capacity, meaning low incremental opex and faster cashflow conversion. Subsea suppliers (TechnipFMC/FTI) and drilling services (Halliburton/HAL, Odfjell) also gain near-term revenue and referenceability; marginal greenfield projects with higher breakevens face relative competitive pressure. Incremental supply is small vs global markets but material regionally: expect modest local production tail extension rather than a Brent price shock. Risk assessment: Tail risks include Norwegian fiscal changes (proposals within 30–180 days), a major operational incident, or partner disputes that could impair cashflows; each would materially re-rate AKRBP given ~25 mmboe upside. Immediate (days) reaction should be muted; short-term (weeks/months) sentiment and supplier re-ratings likely; long-term (years) value accrual depends on realized EUR and oil prices (sensitivity: a $10/bbl move changes NAV of 25 mmboe by roughly $250m–$350m). Hidden dependency: continued availability of Edvard Grieg spare capacity and alliance contract terms could cap upside if capacity constrained. Trade implications: Consider establishing a 2–3% long position in AKRBP (Oslo: AKRBP) within 1–3 weeks, stop-loss 12%, take-profit 20–30% tied to quarterly results or Brent > $90 for 4+ weeks. Add a 1–2% tactical long in TechnipFMC (FTI) to play subsea execution tailwinds and pair versus a 1% short in Halliburton (HAL) to express relative benefit to subsea OEMs over broadfield drilling services. Options: buy a 3-month AKRBP call spread (buy ATM, sell +15% strike) sized to cap max loss to ~0.5–1% portfolio; roll if production guidance improves. Contrarian angles: Consensus likely underestimates partner and capacity frictions — 39 mmboe headline may be front-loaded in press but underlying production profile and uplift timing could be slower, so post-announcement rallies in AKRBP may be overdone. Historical parallels: successful tie-backs often still see 6–18 month output ramp volatility; downside if Norway tax talks (>30% probability in next 90 days) introduce windfall taxes. Action: monitor Norwegian fiscal announcements and Edvard Grieg platform utilization reports in next 60 days before adding size.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment