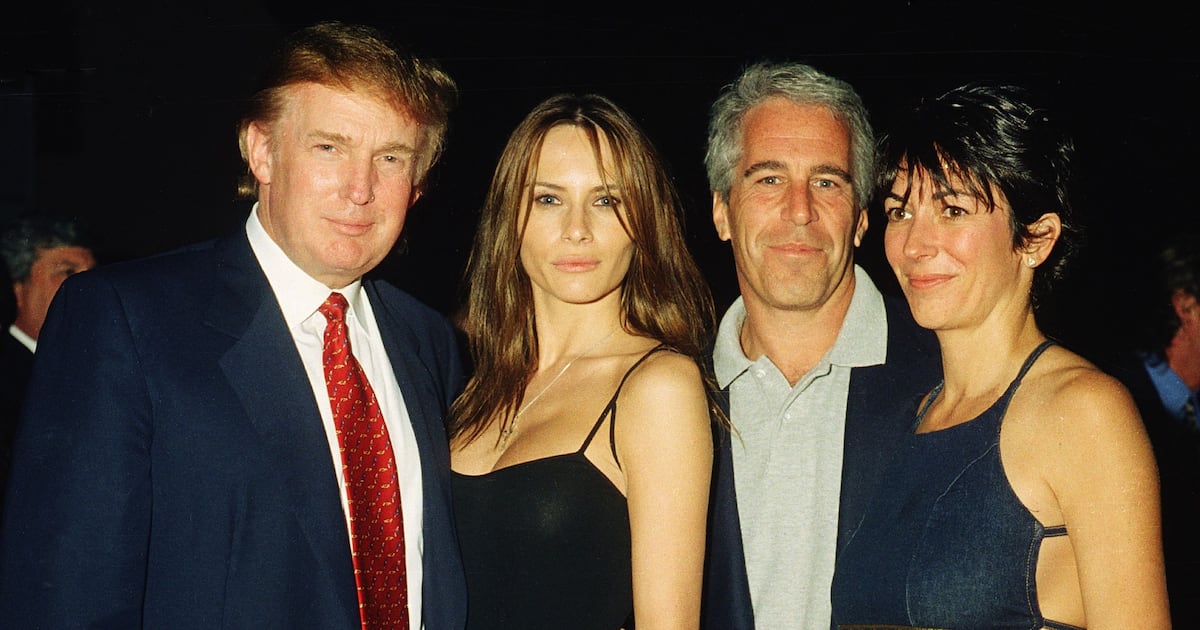

The Justice Department released a tranche of Epstein-related FBI records that includes an unverified Oct. 27, 2020 allegation accusing President Trump of rape; the DOJ cautioned the claims are unfounded. The release — part of 30,000 pages produced after passage of the Epstein Files Transparency Act — has drawn criticism from Democrats who say the department missed legal disclosure requirements and from Republicans defending or downplaying the material, raising political and reputational risks but limited direct market implications.

Market structure: This disclosure is a political shock with mostly sentiment effects — direct winners are safe-haven and volatility instruments (gold, long Treasuries, VIX products) and news/media engagement metrics; losers are reputationally exposed high-profile individuals/entities and advertiser-sensitive platforms if ad boycotts materialize. Pricing power shifts will be small and concentrated: defensive sectors may see a 1–3% relative bid over 1–8 weeks while cyclicals and ad-driven names could underperform by a similar magnitude if controversy persists. Risk assessment: Tail risks include a sustained DOJ/Congressional probe or a surprising legal escalation that raises election uncertainty (low probability, high impact) — that would push VIX >30 and 10y Treasury yields down 30–50bps in a flight-to-safety scenario. Immediate (days) risk is a volatility spike around new releases; short-term (weeks/months) risk is advertiser pullback and reputational capex; long-term (quarters) risk is policy/regulatory changes if the political balance shifts. Hidden dependencies: timing and credibility of future file releases and House hearings will be primary catalysts. Trade implications: Tactical hedges (gold/TLT/VIX) and defensive sector overweight are the highest-probability plays; options hedges keyed to threshold moves (SPY -1.5% to -4%) are efficient. Monitor two trigger metrics: VIX >25 and SPY single-day drop >2% — both should materially increase hedge sizing. Avoid structural long-term shorts on broad markets absent legal escalations that change macro policy. Contrarian angles: Markets historically shrug off personal-political scandals (2016/2019 parallels) — a 3–5% equity drawdown would likely be a buying opportunity in quality cyclicals. The consensus to overweight safety may be overdone if no legal escalation occurs; cap hedge costs by using short-dated option spreads and trim hedges after 30–90 days or once congressional activity subsides.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00