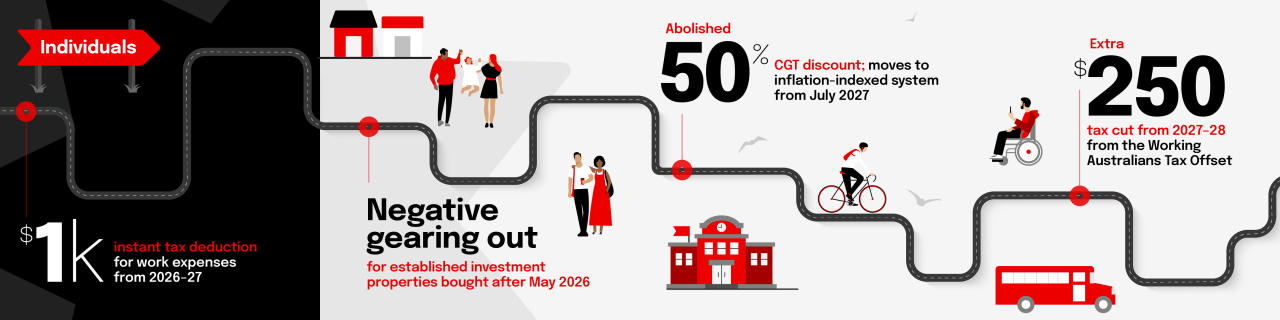

Australia's 2026 Federal Budget proposes sweeping tax changes, including replacing the 50% CGT discount with cost base indexation from 1 July 2027 and imposing a 30% minimum tax on discretionary trust gains. Negative gearing would be removed for existing residential properties bought after Budget night, while a new $250 working Australians tax offset and a permanent $1,000 instant tax deduction were also announced. The package is highly significant for investors, property owners and estate planning, with some measures still subject to consultation and parliamentary passage.

This budget is structurally bearish for levered domestic property exposure because it attacks the tax arbitrage that underpinned after-tax IRRs, not just nominal affordability. The second-order effect is a likely rerouting of capital from existing housing stock toward new-builds, listed REITs with development pipelines, and residential construction supply chains; that should widen valuation dispersion between established landlords and developers with planning inventory. The biggest near-term winner is not housing itself, but any asset class that can absorb wealth allocation from property seeking tax efficiency — especially diversified equities and private market vehicles. The CGT change matters less for day-one market pricing than for behavior into the implementation window: expect a multi-quarter realization wave ahead of 1 July 2027, then a cliff in turnover afterward as investors “lock in” gains before indexation starts. That creates a tactical tailwind for brokers, tax-adjacent software, and market liquidity providers in 2026–27, but a medium-term headwind for transaction volumes in listed property, small-cap resource names, and highly appreciated family-held businesses. The minimum tax on discretionary trusts is also a stealth de-leveraging event for private wealth, because it reduces the value of income splitting and may force more assets into corporate/fixed trust structures where governance is cleaner and disclosure is higher. The contrarian read is that the housing market impact may be less severe than headline language suggests because the exemptions are large enough to preserve much of the institutional rental and build-to-rent ecosystem. The more immediate economic effect could be on consumer confidence among leveraged high-income households, not on aggregate dwelling prices. If legislation softens during consultation, the best risk/reward is in trading the policy path rather than the final form: volatility in property, banks, and small business names should stay elevated into the next 1–2 quarters. The EV FBT extension is a slow-burn positive for fleet conversion, but the market may be overestimating the volume uplift because the benefit is delayed and still capped by luxury-threshold economics. The real beneficiaries are leasing, fleet management, and EV service businesses, while premium ICE dealers face a gradual share bleed rather than an abrupt demand shock. Over 12–24 months, this should support higher EV penetration in corporate fleets even if retail adoption remains rate-sensitive.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15