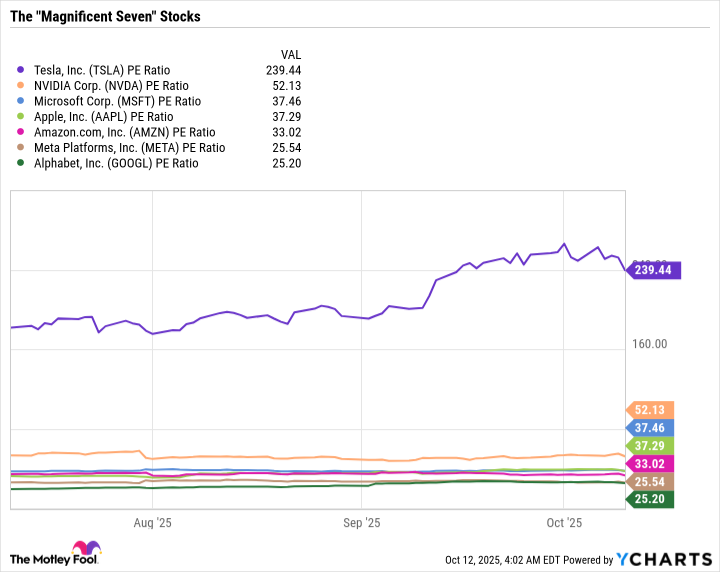

Tesla experienced a 13% decline in EV deliveries in the first half of 2025 due to intensifying competition, following a 1% decrease in 2024. However, the company reported a 7% year-over-year rebound in Q3 2025 deliveries, likely driven by U.S. consumers accelerating purchases ahead of expiring tax credits, which may pull sales from Q4. The upcoming October 22 earnings call is anticipated to focus on updates for future growth platforms, specifically the Cybercab autonomous robotaxi, slated for 2026 mass production but contingent on regulatory approval for full self-driving, and the long-term Optimus humanoid robot. Despite mixed near-term EV performance, Tesla's stock has surged 90% over the past year, resulting in a high P/E ratio of 239x, prompting caution among institutional investors due to valuation concerns and significant product uncertainties.

Tesla's core EV business faced significant headwinds, with deliveries declining 1% in 2024 and a sharper 13% in H1 2025 due to intense competition, particularly in China where market share dipped 4.2 percentage points. While Q3 2025 saw a 7% year-over-year rebound in deliveries to 497,099 units, this growth was likely driven by a one-off tailwind from the expiring $7,500 U.S. tax credit, potentially pulling sales forward from Q4. The upcoming October 22 earnings call will likely focus on updates for future growth platforms: the Cybercab robotaxi and Optimus humanoid robot. Cybercab, targeting mass production in 2026, offers a potential high-margin revenue stream but hinges on regulatory approval for full self-driving (FSD) software, which Musk hopes to secure by year-end 2025. Optimus remains a long-term, speculative venture with a five-year production target for 1 million units annually. Despite mixed operational performance and significant product uncertainties, Tesla's stock has surged 90% over the past year, resulting in an exceptionally high price-to-earnings (P/E) ratio of 239x. This valuation is seven times higher than the Nasdaq-100's 33.5x and nearly five times Nvidia's P/E, suggesting a substantial premium for unproven technologies. This premium, coupled with lagging competition in autonomous robotaxis, implies a high risk of correction if future product timelines or market adoption disappoint.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.65

Ticker Sentiment