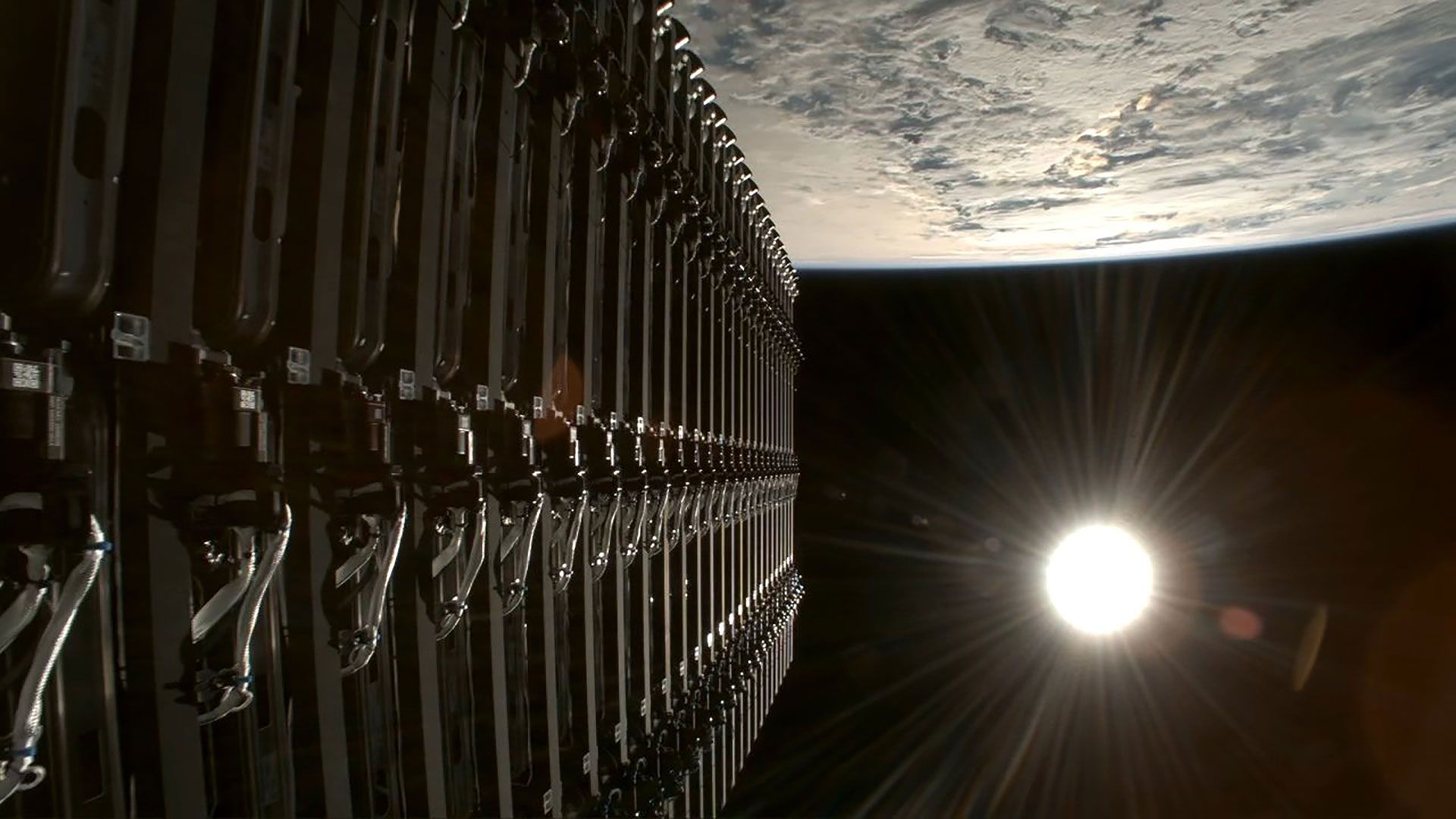

SpaceX will lower roughly 4,400 Starlink satellites from about 342 miles (550 km) to ~298 miles (480 km) over 2026 to reduce collision risk and speed deorbiting, particularly during the upcoming solar minimum; the move is expected to cut ballistic decay time by >80% (from more than four years to a few months in solar minimum). The relocation affects roughly half of Starlink's ~9,400 operational spacecraft, where the fleet currently has only two nonfunctional satellites in orbit, and is intended to improve constellation safety amid growing LEO congestion and new competing megaconstellations.

Market structure: SpaceX's decision to lower ~4,400 Starlinks in 2026 concentrates risk mitigation but also creates a predictable demand shock for propulsive maneuvers and replacements. Expect incremental launch/space-services demand equivalent to a conservative +10–30% of current small-launch manifest volume over 2026–2028 (roughly +100–300 extra rideshare-class missions) as fuel-use shortens operational lives and failed units deorbit faster. Risk assessment: Immediate market impact (days) is muted — public markets won't move SpaceX-specific risk directly — but short-term (weeks–months) watch for operational failures during the reposition phase; long-term (1–3 years) the biggest tail risk is a maneuver failure creating debris that spikes insurance premiums and regulatory constraints. Hidden dependency: fuel burn to lower orbits reduces satellite lifetime, creating steady replacement demand (positive for launch/propulsion suppliers, negative for satellite-equipment CAPEX cycles); catalyst risks include a major collision or an international regulatory restriction on constellations. Trade implications: Direct plays are in launch and spacecraft services vs. legacy GEO broadband. Favor launch/ESM suppliers (RKLB) and spacecraft subsystem primes (LHX, RTX) while selectively shorting legacy broadband vulnerability (VSAT). Use option structures to control timing risk: 6–9 month call spreads on RKLB to capture manifest growth, 3–6 month puts on VSAT to hedge competitive pressure from lower-latency Starlink. Contrarian angles: Consensus understates steady replacement-driven demand vs. one-off safety costs — markets are likely underpricing multi-year launch revenue from forced lifecycle compression. Historical parallel: Iridium Next drove multi-year launch tails; if Starlink de-orbits failures within months as stated (>80% reduction to “few months”), replacement cadence could double parts of the manifest, creating mispricings in small-launch equities and suppliers before broader recognition.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.10