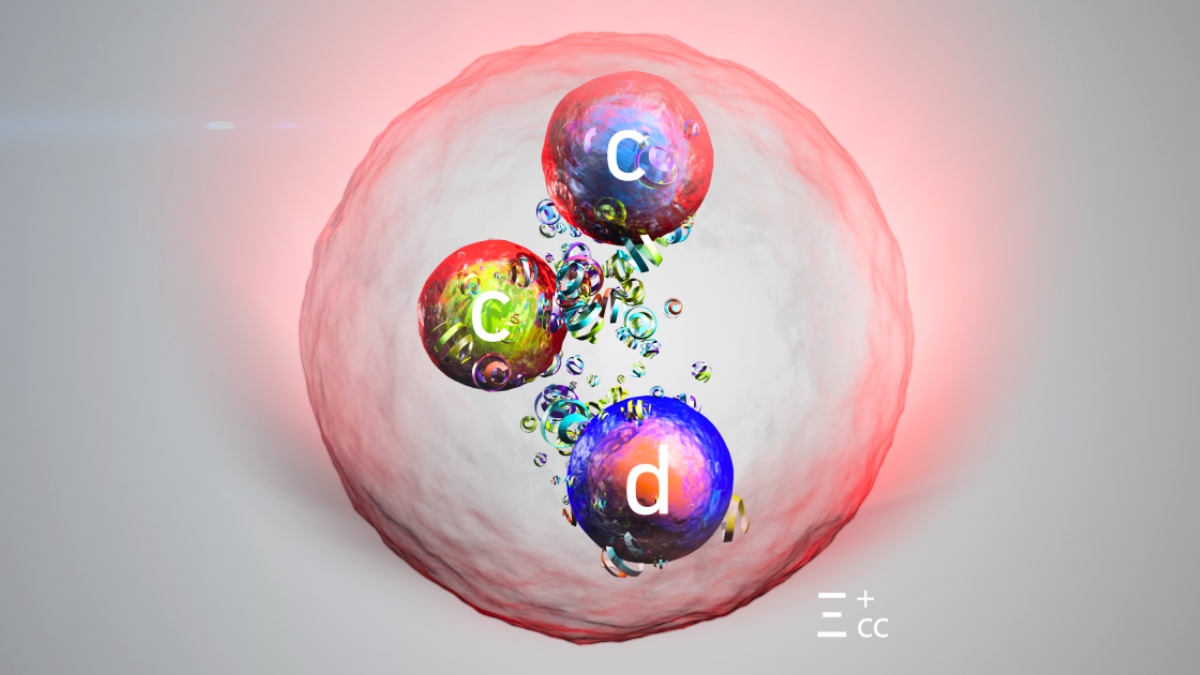

The Large Hadron Collider announced discovery of the 80th particle, the Xi-cc-plus, a baryon made of two charm quarks and one down quark and roughly four times the mass of a proton. It is the second observed baryon with two heavy quarks and the first new particle identified after LHCb detector upgrades completed in 2023; its expected lifetime is about six times shorter than a similar 2017 particle, making it harder to spot. This is a notable scientific/technology milestone with negligible direct market impact for financial portfolios.

Big-science discoveries operate less as consumer-demand drivers and more as multi-year procurement cascades that concentrate revenue into a small set of high-technology suppliers (precision magnets, cryogenics, vacuum systems, advanced lithography and bespoke sensors). Contracts are lumpy and bilateral; a single detector or collider subsystem can generate $10s–100s of millions of orders with 3–7 year lead times, turning well‑positioned suppliers into multi-year revenue streams rather than one‑quarter bumps. The main tempo of value capture will be in two waves: near-term (6–24 months) follow‑on work for detectors, data pipelines and HPC/AI infrastructure, and medium/long‑term (2–15+ years) spending tied to new accelerator projects and facility upgrades. Key catalysts are public funding approvals, procurement award announcements, and compute-contract rollouts for algorithmic reconstruction — each can re‑rate targeted suppliers quickly, while budget pullbacks or geopolitical reallocation of R&D spending are credible reversal drivers. Market consensus will likely headline broad technology winners (AI chips, semicap) but underrates narrow engineering margins and supplier concentration: a handful of suppliers capture most upside while the rest see little impact. That makes concentrated, size‑controlled exposure and option structures the optimal approach — avoid large exposure to broad cyclicals where the discovery is noise and prefer targeted names with clear procurement pathways and margin visibility.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.20