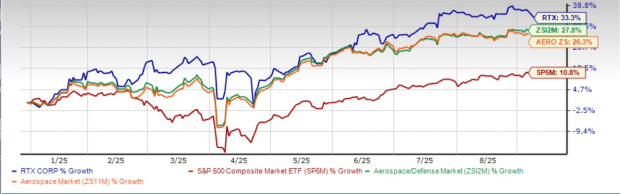

Raytheon (RTX) recently secured a $205 million contract for its Phalanx CIWS, contributing to a robust Q2 2025 defense booking of $12 billion and a $92 billion backlog by June 30, 2025. Despite strong liquidity and a 33.3% YTD stock gain outperforming benchmarks, the company faces risks from persistent supply-chain disruptions, potential global trade turmoil due to tariffs, and a premium valuation of 24.07x forward P/E. Furthermore, near-term earnings estimates have seen recent downward revisions, suggesting a cautious outlook for new investors despite long-term growth prospects.

RTX Corporation demonstrates a robust operational and financial position, underscored by a recent $205 million contract for its Phalanx CIWS. This award contributes to significant momentum, with Q2 2025 defense bookings reaching $12 billion and elevating the total defense backlog to a substantial $92 billion as of June 30, 2025, providing strong future revenue visibility. The company's financial health is solid, evidenced by a cash position of $4.78 billion against $3.72 billion in current debt and a current ratio of 1.01. This fundamental strength is reflected in its stock performance, which has gained 33.3% year-to-date, outperforming both its industry peers and the S&P 500. However, this positive outlook is tempered by several material risks. The stock trades at a premium forward P/E of 24.07x compared to its peer group's average of 23.91x, and near-term earnings estimates have seen downward revisions over the past 60 days, signaling declining analyst confidence. Furthermore, RTX faces persistent supply-chain disruptions in its commercial aerospace business, which could delay revenue recognition, and is exposed to global trade risks from tariffs and retaliatory measures.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment