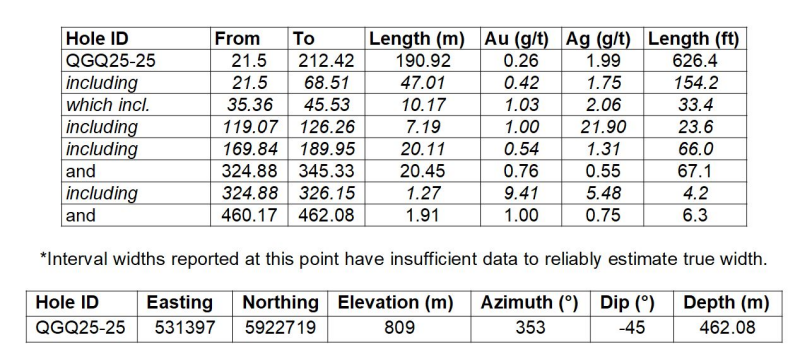

Golden Cariboo Resources reported diamond drill hole QGQ25-25 at its Quesnelle Gold Quartz Mine intersected 0.42 g/t Au over 47.01 m from surface within a broader 0.26 g/t Au over 190.2 m interval, plus higher-grade mineralization of 0.76 g/t Au over 20.45 m from 324.88 m and the hole ending in 1.00 g/t Au over 1.91 m. The hole is a 96 m step-out from a previous large intercept (QGQ24-20: 0.99 g/t Au and 9.77 g/t Ag over 236.88 m), extending the Halo zone along strike; the company highlights year-round drilling access, QA/QC protocols and PhotonAssay use to address coarse-gold nugget effects. Results suggest potential for resource expansion near-surface and at depth, which could influence investor interest in this junior exploration stock but are not, by themselves, material to broader markets.

Market structure: Golden Cariboo (GCCFF) is the immediate beneficiary — successful step-outs and wide, near-surface intercepts shift optionality from pure exploration toward bulk-tonnage potential, improving appeal to mid-tier acquirers (Osisko Development/ODV) and drill/service contractors in BC. Downstream losers are speculative explorers without district scale; the announcement is unlikely to move global gold supply/demand but can re-rate local corridor valuations if follow-up holes sustain >0.5 g/t over 100–200m. Cross-asset impact is muted: minor positive for junior mining equities, negligible for sovereign bonds and FX; increased idiosyncratic volatility could lift implied vol in small-cap junior miners for 1–3 months. Risk assessment: Tail risks include rapid equity dilution (typical for juniors — expect C$3–15M raises), permitting/First Nations delays of 12–36 months, and nugget-effect assay variability despite PhotonAssay — a single hole reversal could cut perceived continuity. Immediate (days) volatility will track news cadence; short-term (3–6 months) outcome depends on 3–6 additional step-outs; long-term (12–24 months) value requires a maiden resource/PEA and metallurgy. Hidden dependencies: cash runway, JV interest from ODV, and gold price staying above ~$1,700/oz to keep M&A optionality alive. Trade implications: For active portfolios, a small speculative long in GCCFF (1–3% of capital) with clearly defined add-on triggers (two consecutive step-outs >0.5 g/t over >20m within 3 months) captures asymmetric upside; hedge metal beta by shorting 0.5x notional of GDXJ for 3–12 months. Use ODV as a liquid corridor play via 6–9 month call spreads (buy ATM, sell 30–50% OTM) sized 1–2% of portfolio to limit downside while keeping takeover upside. Exit/stop rules: hard stop -40% on GCCFF or sell if share count increases >25% without >=C$3M cash. Contrarian angles: Consensus may underweight the PhotonAssay result which materially reduces nugget risk — positive for continuity — but overstates comparability to Spanish Mountain; market often prizes spectacle over metallurgy. The reaction is probably underdone in a tight float: sustained confirmation of bulk continuity could produce >100% gaps on thin liquidity, while failure to define continuity or heavy dilution can wipe out early gains. Historical parallels: many BC SHV projects showed wide low-grade intercepts that required long funding cycles and heavy dilution; prepare for binary outcomes and front-load strict sizing and dilution-based exit triggers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment