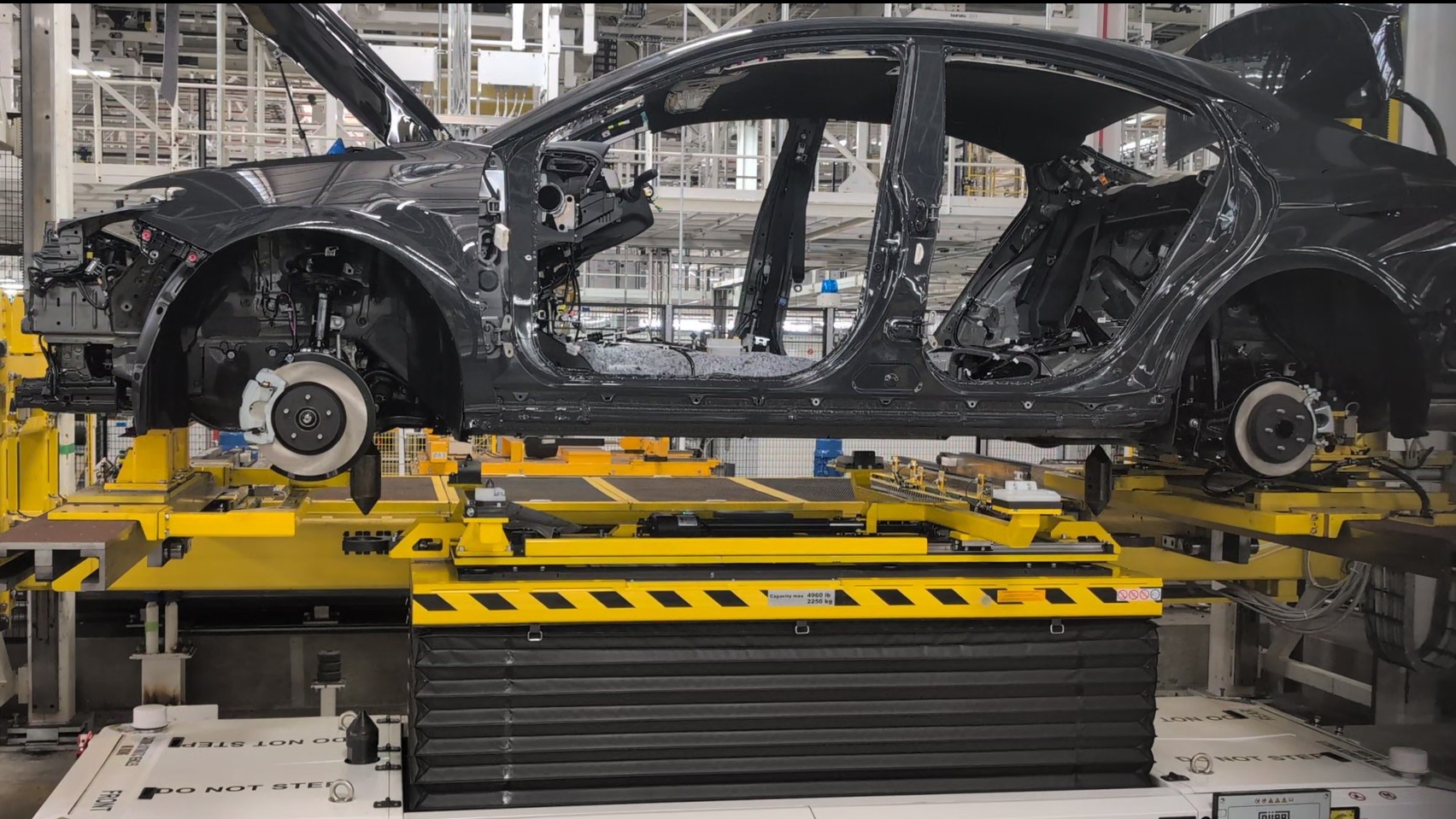

Toyota will invest $1.0 billion in its Kentucky and Indiana plants to increase production of Grand Highlander SUVs and to build three EV models, announced March 23, 2026. The capital boost expands U.S. manufacturing capacity, supports Toyota's EV transition and regional supply-chain activity, and is likely to be modestly positive for Toyota shares and local economic activity.

A U.S.-centric vehicle production tilt materially reweights the supply-chain map: tier-1 power-electronics, battery assembly and chassis suppliers located in the Midwest and Southeast gain faster order visibility and shorter inventory cycles, while overseas component exporters face longer lead-times and higher landed costs. That reallocation tends to compress working capital for domestic suppliers (improving ROIC) and increases bargaining power for regional labor and real-estate providers — anticipate 6–18 month headwinds for global logistics suppliers as OEMs requalify local sources.

High-performance vehicle compute drives an underappreciated bump in non-semiconductor hardware spend — advanced cooling, heavier gauge wiring, and higher-capacity DC/DC conversion each add incremental BOM cost measured in the low hundreds to low thousands per vehicle, not insignificance for sub-$40k models. That mechanism creates a follow-on upgrade cycle for Tier-1s and specialized thermal vendors (unit economics scale with compute), even if some OEMs elect lower-power, alternative chips for cost parity.

The semiconductor architecture debate is the key gating factor for winners over the next 12–36 months: incumbents that lock design wins for whole-vehicle integration (compute + powertrain + thermal co-design) capture outsized margin; standalone compute suppliers face a longer path unless they subsidize cooling or co-develop power electronics. Tail risks — battery supply shocks, macro-driven demand softness, or a sudden OEM pivot to cheaper, more thermally-efficient accelerators — can reprice automotive compute TAM quickly, pushing revenue into later years and compressing near-term multiples.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment