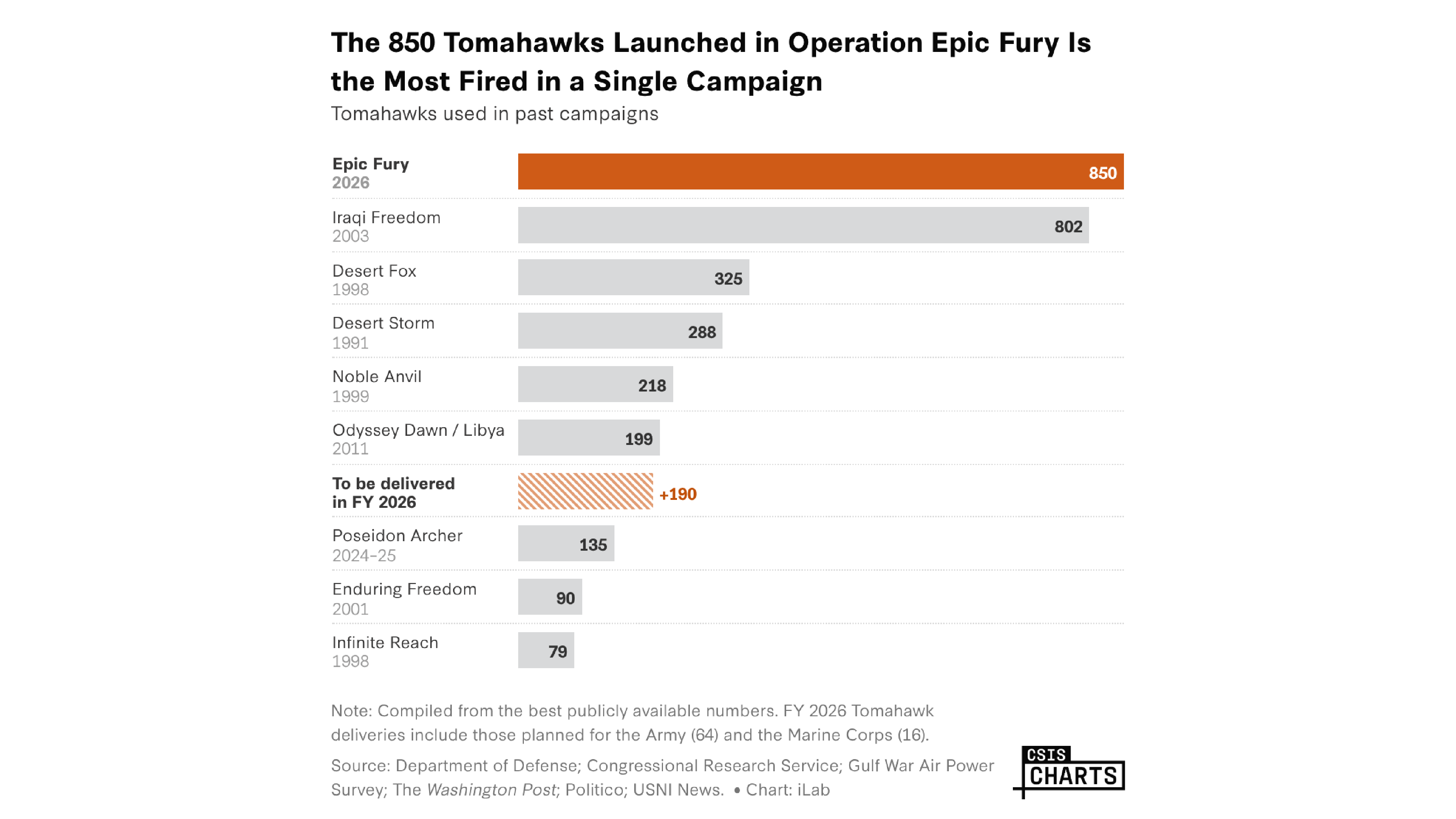

850 Tomahawk missiles were fired in the first four weeks of Operation Epic Fury. At ~$3.6M per missile, the expenditure is roughly $3.06B and represents about half of available regional launchers, depleting at-sea strike capacity that cannot be reloaded. The Navy is slated to receive 110 Tomahawks in FY2026 and stockpiles are in the low-3,000s, but the high burn rate raises near-term risks to U.S. deterrence and operations—particularly in the Western Pacific.

Sustained high-tempo missile use forces a logistics and industrial reset that shows up as non-linear opportunity costs: platforms absent for reload/maintenance create multi-week to multi-month presence gaps in regions where deterrence is finely balanced, raising asymmetric geopolitical risk without needing additional force generation. That operational hole will be filled either by accelerated procurement and surge industrial output or by redistribution of assets from other theaters, each with distinct market winners and losers over different horizons.

On the supply side, the vendor ecosystem for propulsion, guidance sensors, and warhead integration is where pricing power and bottlenecks will concentrate; firms that own scarce precision components can convert backlogs into multi-quarter outsized margins, while commodity assemblers face margin pressure if primes push down prices to scale. Expect lead-times for key subsystems to determine which contractors win follow-on awards — this is a 6–24 month play, not a two-week headline trade.

Near-term fiscal mechanics favor prime contractors and shipyards: emergency buys and port-based reloading/repair work flow into revenue sooner than new-build platforms, so companies with service/repair footprints capture cash quickly. Conversely, a strategic pivot toward lower-cost loitering munitions by buyers would be a structural headwind for producers of high-end cruise missiles over 2–5 years, creating asymmetric downside that’s underpriced by markets focused on immediate replenishment orders.

Catalysts that will reverse the trade are political: rapid allied transfers, diplomatic de-escalation, or a decision to offload inventory from partner stocks would blunt procurement momentum within weeks; supply-side upside is capped if DoD opts for lower-cost substitutes or if key component suppliers hit capacity constraints that force program slowdowns. Watch classified award notices, emergency procurement memos, and Congressional appropriation language as the real short-term drivers of valuation re-rating.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35