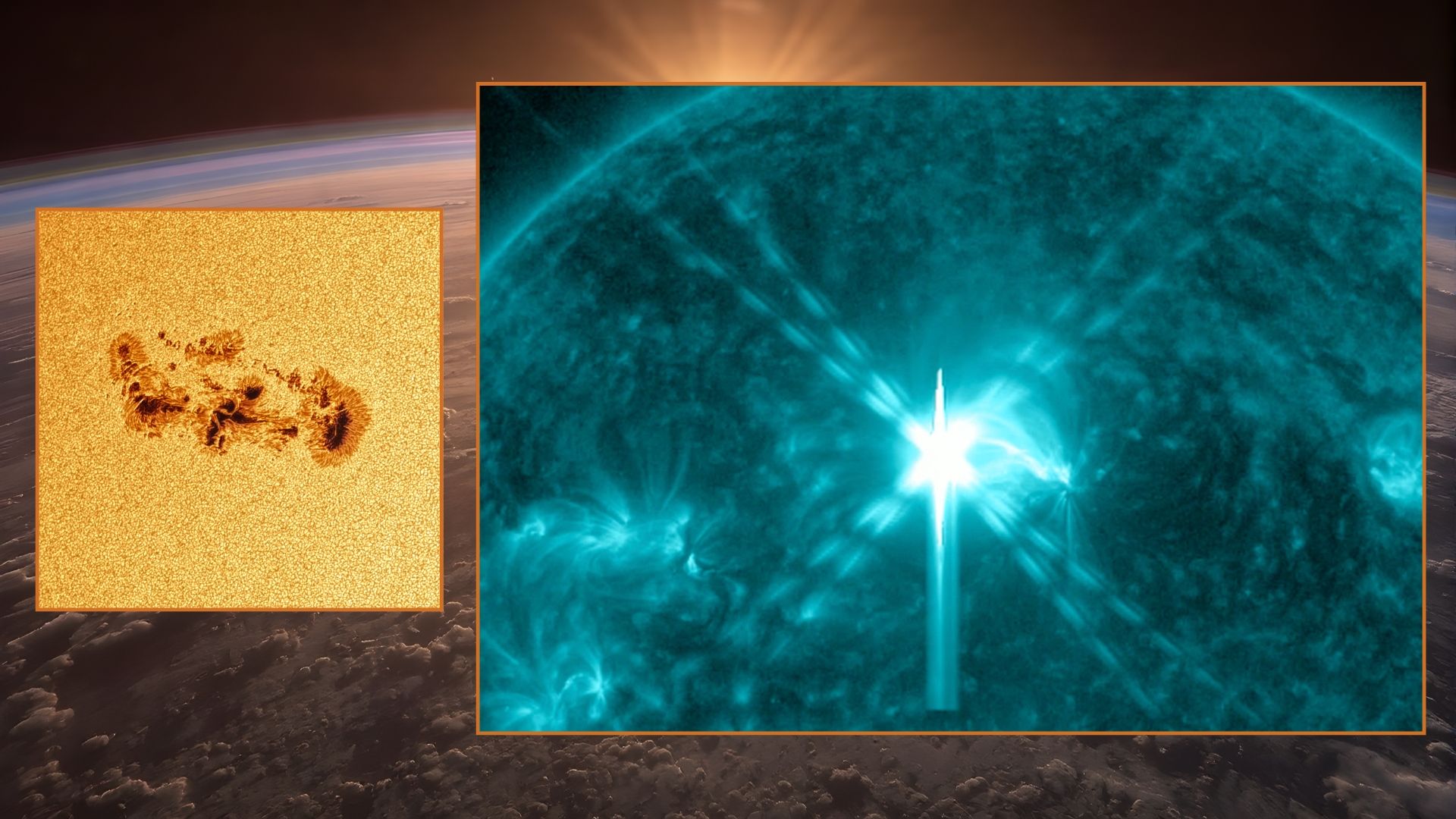

An impulsive X4.2 solar flare from sunspot region AR4366 peaked Feb. 4 at 7:13 a.m. EST, causing short-lived radio blackouts over western Africa and southern Europe. NOAA's Space Weather Prediction Center reports no CME signatures from this eruption, though an earlier X8.4 flare produced a slow-moving CME that delivered only a glancing blow and could produce minor (G1) geomagnetic activity; forecasters continue to monitor the active, magnetically complex region for further activity that could affect communications and infrastructure.

Market structure: Near-term winners are specialized satellite operators and space‑infrastructure contractors (Iridium IRDM, Viasat VSAT, Maxar MAXR, Eaton ETN for grid hardware) and defense primes with space portfolios (Lockheed LMT, Northrop NOC, RTX). Losers in the immediate window are HF‑radio and GPS‑dependent operators (airlines DAL/UAL, logistics FDX/UPS) through temporary routing/comms disruptions; pricing power shifts toward suppliers of hardened electronics and grid/GIC mitigation equipment over the next 12–36 months as budgets reallocate. Risk assessment: Tail risk remains low short‑term (no CME signature now) but non‑zero for a Carrington‑class event (historical probability ~0.5–1%/decade) with systemic loss scenarios >$100B–$1T to infrastructure; monitor Kp index (Kp≥5 = G1, Kp≥7 = G3) and NOAA SWPC CME flags in the next 72 hours. Hidden dependencies include long lead times for transformer replacements and single‑vendor concentration for satellite buses; a damaging CME would compress insurance capacity and force regulatory intervention within 1–6 months. Trade implications: Tactical plays: small, conviction‑weighted longs in space/hardening names (1–3% positions) and short dated protective puts on exposed airlines/logistics for 30–90 days; use calendar/vertical option structures to limit premium. Cross‑asset: brief flight‑to‑quality may lift 2‑yr Treasuries and gold (GLD) intraday; commodities and FX impact likely immaterial unless geomagnetic event disrupts supply chains for weeks. Contrarian angles: The market tends to overreact to X‑class flares absent CMEs — buying 5–10% pullbacks in IRDM/VSAT/MAXR on a non‑CME outcome is a tactical opportunity. Long‑run implication (12–36 months) is underpriced: expect a 3–7% re‑rating for suppliers of space‑weather mitigation if a series of glancing blows continues and governments accelerate resilience spend; downside is supply‑chain delays that will postpone revenue recognition.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.00