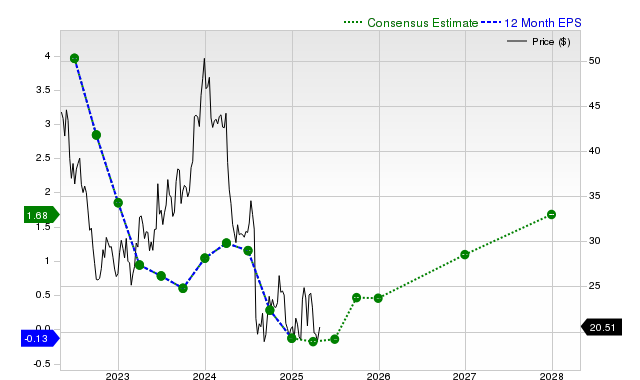

Intel's stock has been trending on Zacks.com, with shares declining 2.6% over the past month while its industry gained 18.8%. Current quarter earnings are projected to be $0.01 per share, a 50% year-over-year decrease, while revenue is expected to be $11.87 billion, down 7.5% year-over-year; however, fiscal year estimates point to significant EPS growth of +323.1% and +164.7% for the current and next years, respectively, albeit with recent downward revisions. The stock holds a Zacks Rank #3 (Hold), suggesting near-term performance in line with the broader market.

Intel (INTC) has recently underperformed, with its shares declining 2.6% over the past month, starkly contrasting with the S&P 500's 4.6% gain and the Zacks Semiconductor - General industry's 18.8% rally. The company's near-term financial projections present a mixed picture: current quarter earnings are anticipated at $0.01 per share, a significant 50% year-over-year decrease, and revenue is forecasted at $11.87 billion, down 7.5% YoY. Despite these immediate headwinds, consensus estimates for the current fiscal year project a substantial EPS increase of 323.1% to $0.29, and a further 164.7% rise to $0.77 for the next fiscal year. However, these estimates have seen recent downward revisions across all periods (current quarter -0.7%, current fiscal year -0.9%, next fiscal year -2.5% over the last 30 days). Current fiscal year revenue is expected to decline by 4.3% to $50.8 billion, before a projected 4.1% growth to $52.88 billion next year. Intel's last reported quarter showed revenue of $12.67 billion (-0.5% YoY) and EPS of $0.13, surpassing consensus estimates by +2.8% and +1200% respectively. The stock currently holds a Zacks Rank #3 (Hold) and a Value Style Score of C, indicating it trades at par with its peers, suggesting that the market may be pricing in both the challenges and the recovery potential.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.10

Ticker Sentiment