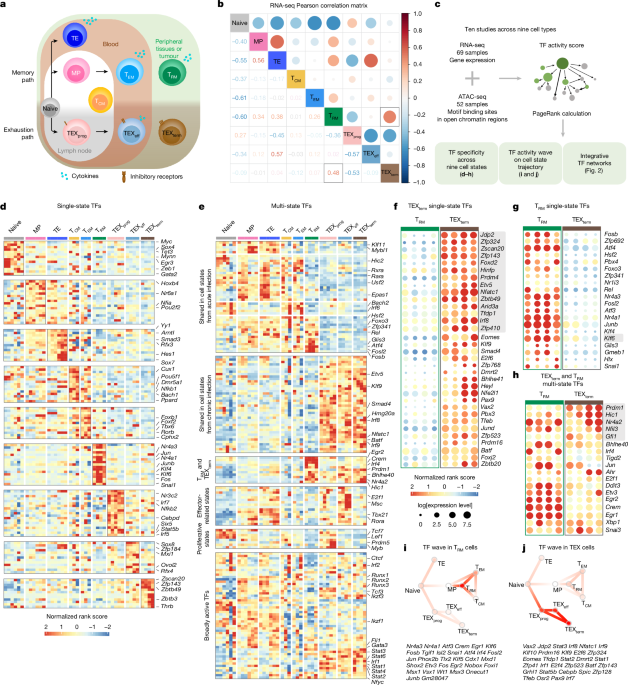

Researchers built a Taiji multi-omics atlas integrating 121 ATAC-seq/RNA-seq experiments across nine CD8+ T cell states and used in vivo Perturb-seq to map transcription factor (TF) activity driving terminally exhausted (TEXterm) versus tissue-resident memory (TRM) states. From a 19-gene CRISPR library they identified TEXterm-selective TFs (notably ZSCAN20 and JDP2) whose deletion reduced exhaustion, improved effector function, enhanced tumor control and synergized with anti-PD1, while KLF6 overexpression selectively expanded TRM cells without increasing exhaustion. Cross-species analyses showed conservation of many TF activities in human TIL datasets and KO in human CD8+ cells reduced inhibitory receptor expression and raised cytokine output, highlighting near- to mid-term translational targets for cell-therapy engineering and potential biotech development opportunities.

Market structure: Life-science tools and single-cell/CRISPR platform vendors are the primary near-term beneficiaries—expect incremental demand for scRNA/ATAC kits, transposases and RNP reagents to lift revenue growth for Thermo Fisher (TMO), Illumina (ILMN) and 10x Genomics (TXG). Pricing power should be strongest for proprietary assay/platform providers (TXG, ILMN) where lead times and switching costs are high; consumables players (TMO, A) capture recurring margin expansion. Demand shock timing: labs will drive revenue within 3–12 months as academic and translational groups adopt the Taiji/TaijiChat workflow and Perturb-seq pipelines. Risk assessment: Key tail risks are regulatory (FDA tightening on engineered-T cell INDs or CRISPR edits) and translational (human safety/efficacy failures) that can depress adoption for 12–36 months; manufacturing bottlenecks (viral vector, GMP slots) could constrain scale and spike reagent lead times 20–40%. Hidden dependencies include CMOs and centralized GMP capacity—if capacity remains constrained, revenue upside for tools vendors will be delayed. Catalysts: IND filings, phase I efficacy/safety readouts, and large pharma partnerships over the next 6–18 months will accelerate adoption; adverse safety signals or restrictive guidance within 0–9 months would reverse momentum. Trade implications: Direct plays: overweight TMO, ILMN and TXG via equity and call spreads to capture 10–25% re-rating over 6–12 months; prefer call-spread structures to cap premium. Relative ideas: rotate out of broad biotech beta (IBB) into tools—reduce IBB weighting by 2–3% and redeploy into TMO/ILMN/TXG to exploit differentiated revenue leverage. Options: buy 6–9 month call spreads on TXG and ILMN (ATM buy / 10–15% OTM sell) to capture adoption-driven upside while limiting theta risk. Contrarian/risks-to-consensus: The market may be underestimating time-to-clinic and reimbursement complexity—expect a 12–24 month lag between research adoption and commercial revenue, so acute valuation moves may be overdone. Historical parallel: early CAR‑T reagent booms saw a 30–50% correction when clinical logistics constrained uptake; guard for similar mean-reversion. Unintended consequence: targeting single-state TFs could produce narrower clinical populations and slower commercial uptake, capping near-term topline despite scientific promise.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment