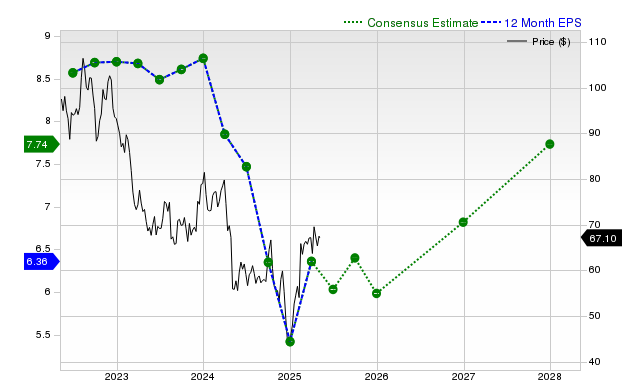

CVS Health (CVS) has recently underperformed, with shares down 4.7% over the past month against a rising S&P 500, yet it holds a Zacks Rank #2 (Buy) based on several positive indicators. Analyst consensus estimates project current fiscal year EPS growth of 12.9% to $6.12 and next fiscal year growth of 14.4% to $7.00, with recent upward revisions. The company also demonstrated strong operational performance, beating last quarter's revenue by 1.76% and EPS by 31.58%, and has consistently surpassed EPS estimates for four consecutive quarters. Furthermore, CVS is assessed as undervalued with a Zacks Value Style Score of 'A', suggesting potential for near-term outperformance despite its recent stock and industry underperformance.

Despite significant recent underperformance, with its stock declining 4.7% over the past month against a 4.5% gain in the S&P 500, CVS Health Corporation (CVS) exhibits strong underlying fundamentals that suggest a potential disconnect between market sentiment and operational reality. The company's last reported quarter showed robust results, with a 7% year-over-year revenue increase to $94.59 billion and an EPS of $2.25, representing a significant +31.58% surprise over consensus estimates. This continues a trend of the company beating EPS estimates for four consecutive quarters. Looking forward, while the current quarter's EPS is expected to decline 19.7% YoY, the outlook for the full fiscal year and the next remains positive, with projected EPS growth of 12.9% and 14.4%, respectively. These projections are supported by recent upward revisions from sell-side analysts and underpin the stock's Zacks Rank #2 (Buy). Furthermore, valuation appears attractive, as indicated by a Zacks Value Style Score of 'A', suggesting the stock is trading at a discount to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment