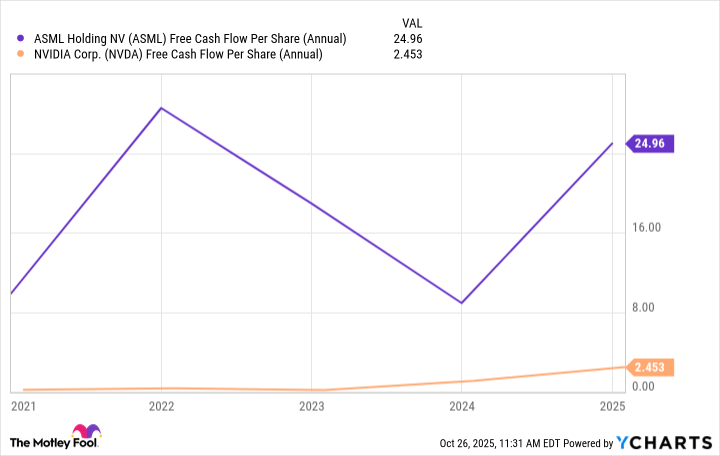

The article posits that ASML (ASML) currently offers a more compelling investment opportunity than Nvidia (NVDA), despite Nvidia's strong position in AI semiconductors. ASML maintains a critical, monopolistic advantage as the sole manufacturer of Extreme Ultraviolet (EUV) lithography machines, which are indispensable for advanced microchip fabrication. Financially, ASML demonstrates a superior free cash flow yield of 2.4% compared to Nvidia's 1.6%, and its current valuation at 38 times trailing earnings is considered attractive relative to its five-year average of 39.6x, suggesting a better value proposition for investors seeking exposure to foundational semiconductor technology.

ASML holds a critical, monopolistic position as the sole manufacturer of Extreme Ultraviolet (EUV) lithography machines, which are indispensable for advanced microchip fabrication. This technological exclusivity significantly differentiates ASML within the semiconductor industry, providing a robust competitive moat. The company's EUV systems simplify complex manufacturing processes for its customers, underscoring its indispensable role in the production of sophisticated microchips. While Nvidia demonstrated substantial free cash flow growth from $26.9 billion in fiscal 2024 to $60.7 billion in fiscal 2025, ASML also reported impressive growth, with free cash flow rising from 3.2 billion euros in 2023 to 9.1 billion euros in 2024. Crucially, ASML exhibits a superior trailing-12-month free cash flow yield of 2.4% compared to Nvidia's 1.6%. Furthermore, ASML's current valuation at 38 times trailing earnings is attractive relative to its five-year average P/E of 39.6x, suggesting a more compelling value proposition. The article posits ASML as a more opportune investment currently, despite Nvidia's dominant role in AI semiconductors and significantly higher revenue ($130.5 billion for Nvidia in FY25 vs. 28.3 billion euros for ASML in 2024). ASML's unique market position combined with its stronger free cash flow yield and relatively appealing valuation supports a bullish outlook for the stock. This suggests a foundational play in the semiconductor supply chain rather than a direct AI beneficiary.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.85

Ticker Sentiment