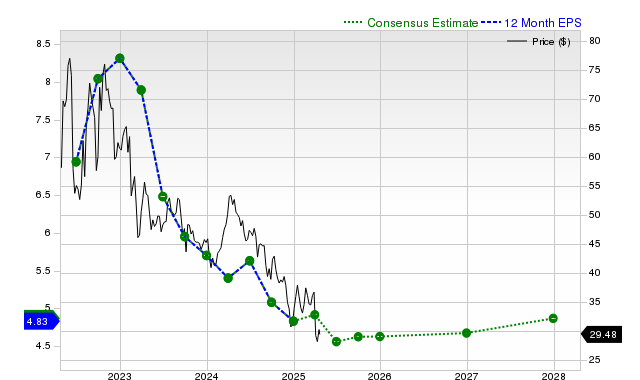

Devon Energy (DVN) is attracting investor attention, though its shares have underperformed the S&P 500 over the past month. While the company has consistently beaten revenue estimates in the last four quarters and holds a favorable 'A' Zacks Value Style Score indicating it trades at a discount to peers, consensus earnings estimates for the current quarter and fiscal year have seen downward revisions of -4.6% and -1.1% respectively. This trend has resulted in a Zacks Rank #3 (Hold), suggesting the stock may perform in line with the broader market in the near term.

Devon Energy (DVN) presents a mixed fundamental picture, characterized by a conflict between historical performance, current valuation, and forward-looking earnings estimates. The company has a strong track record of execution, having surpassed revenue consensus estimates in each of the last four quarters, including a +6.75% surprise in the most recent period. Furthermore, its 'A' grade on the Zacks Value Style Score indicates it is trading at a discount relative to its peers. However, this is counterbalanced by a deteriorating near-term earnings outlook. Sell-side analysts have revised current quarter earnings estimates down by 4.6% over the last 30 days, with expected EPS representing a 13.6% decline year-over-year. Similarly, the consensus estimate for the current fiscal year points to a 15.4% earnings contraction. These negative revisions are the primary driver for the Zacks Rank #3 (Hold), suggesting the stock, which has already underperformed the S&P 500 over the past month (+0.7% vs +2.7%), may continue to perform in line with the broader market in the near term. A slight positive revision of +0.5% to the next fiscal year's earnings estimate, which projects 3.7% growth, offers a potential long-term positive but is insufficient to outweigh current headwinds.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment