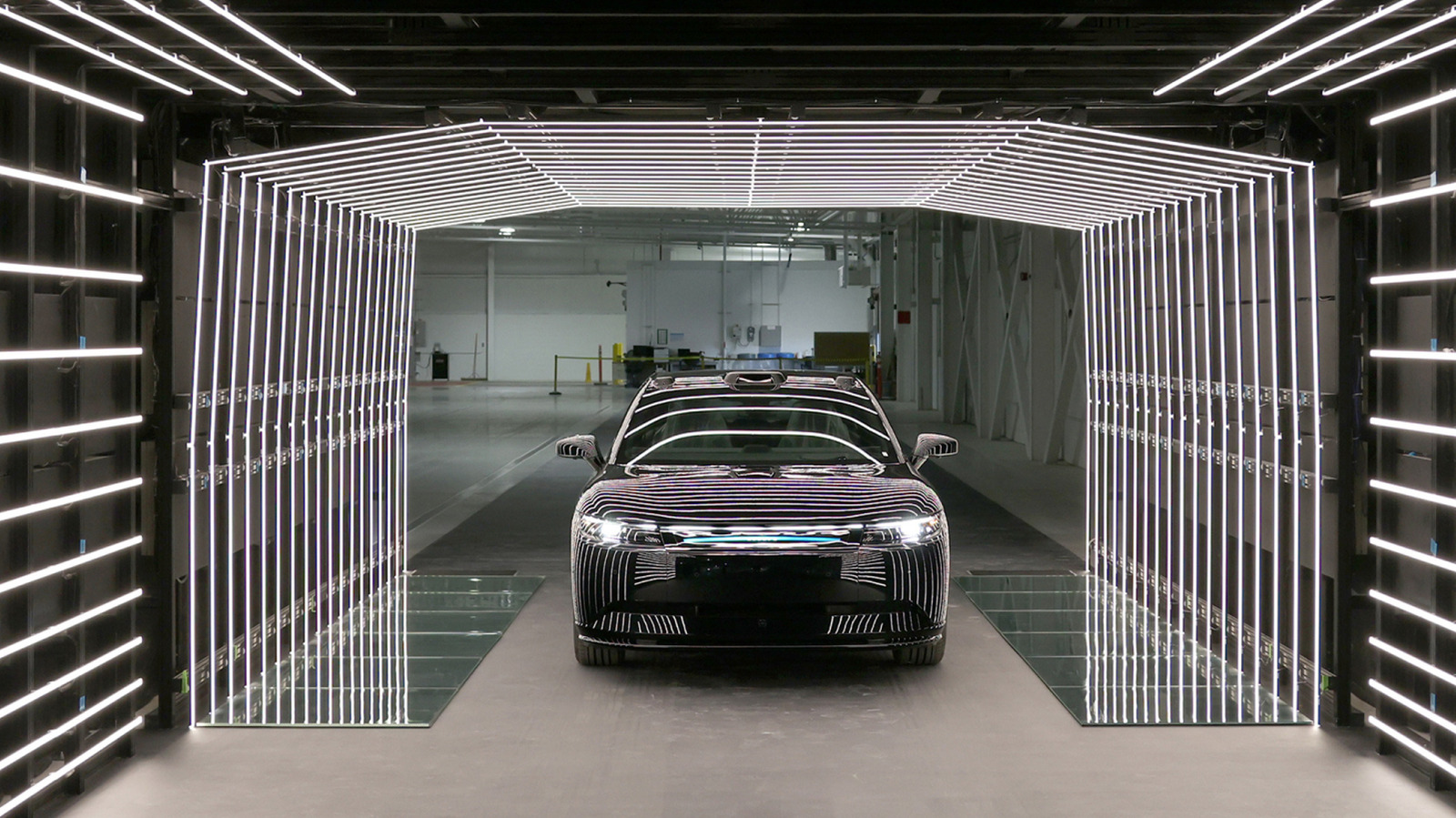

Sony Honda Mobility has completed a trial production run of the Afeela 1 at Honda’s East Liberty, Ohio plant, incorporating a dedicated ‘Quality Gate’ for function and exterior inspections ahead of planned U.S. deliveries starting mid-2026. The Signature trim starts at $102,900 (Origin to follow at $89,900 in 2027) and offers dual-motor AWD with 483 hp, a 91‑kWh battery, an EPA-estimated max range of about 300 miles and 150 kW DC fast-charging; sales are initially limited to California with a $200 refundable reservation. Given the high price, limited availability and relatively weak charging and range specs versus much cheaper or better-performing rivals (e.g., Hyundai Ioniq 5, Lucid Air), demand and competitive positioning look challenged despite strong tech integration (PlayStation features, ~40 sensors, AI).

Market structure: The Afeela launch tightens the luxury-tech EV niche but will have negligible volume impact on global EV supply — Signature at $102,900 vs Origin $89,900 (2027) and California-only delivery constrains TAM to <<100k units/year initially. Technically the car is weak on economics (91 kWh, 150 kW DC, ~300 mi) versus competitors (Hyundai Ioniq 5 ~$39k; Lucid Air Touring ~$90k with far more range), so pricing power is limited and margin recovery will depend on software/recurring revenue, not hardware alone. Risk assessment: Tail risks include large warranty/recall bills from ADAS/infotainment failures, regulatory pushback on in-cabin entertainment/autonomy, or a production ramp freeze — any of which could induce a multi-month reputational hit to SONY's auto remit. Timeline: days – minimal market move; weeks–months – media/regulatory scrutiny spikes around CES and mid-2026 delivery window; quarters–years – profitability hinge on software monetization and scaled production at East Liberty. Trade implications: Favor concentration on firms whose product economics win (Lucid, charging/battery infra) and hedge Sony exposure since SHM is a small but headline-risky asset on SONY. Use option structures to express view (defined-risk spreads) rather than naked directional bets; expect alpha to materialize over 6–18 months as deliveries approach and specs/pricing are market-tested. Contrarian angles: Consensus underweights the potential for Sony to monetize PlayStation/entertainment subscriptions in-vehicle (recurring ARPU could justify a higher valuation multiple if conversion >5–10% of buyers). Conversely, the market may be underestimating execution risk — if the crossover/compact variants (cheaper, higher-range) materialize in 12–24 months, SHM could surprise to the upside, creating a re-rating event for the auto-software mix.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.52

Ticker Sentiment