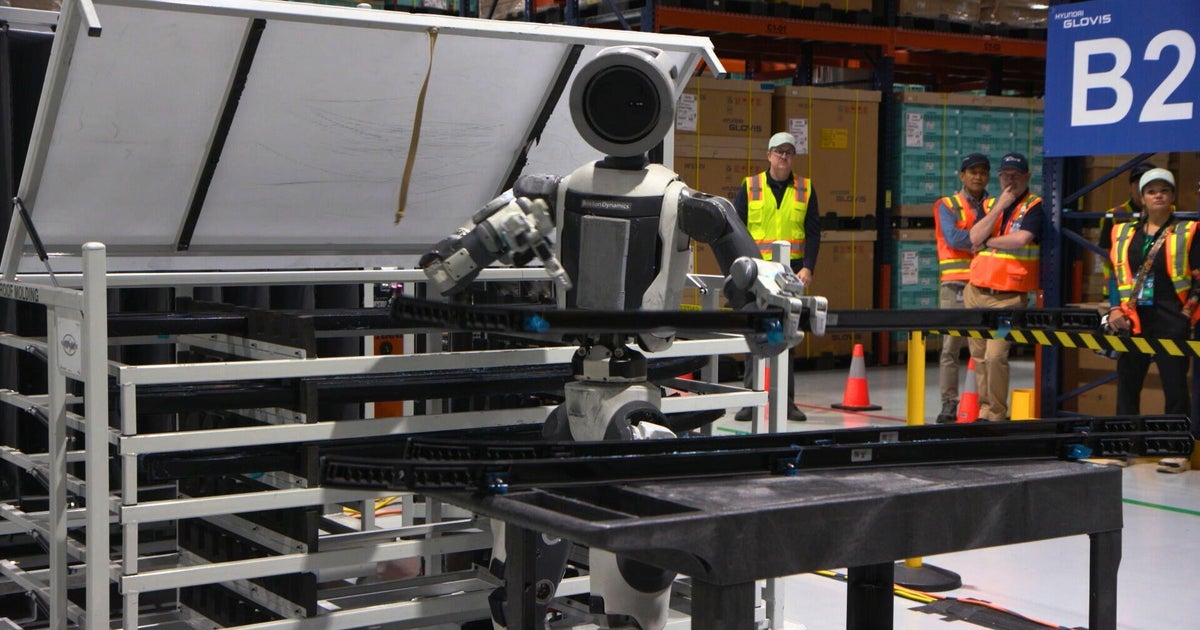

Boston Dynamics is field-testing its AI-powered humanoid Atlas — a 5'9", 200 lb robot — at Hyundai's new Georgia factory after a year of development, using Nvidia chips and large-scale simulation and teleoperation to teach tasks such as autonomous parts-sorting. Hyundai, which holds an 88% stake in Boston Dynamics (company valued at over $1 billion), presented Atlas as a multi-year effort toward automating repetitive, hazardous factory work while emphasizing continued human roles in building, training and servicing robots. Goldman Sachs projects a humanoid market of $38 billion within a decade, and Boston Dynamics faces intense competition from U.S. startups and state-backed Chinese firms, making this a strategic technology and industrial investment story rather than an immediate earnings catalyst.

Market structure: The immediate winners are AI compute providers (NVDA) and integrators that can bundle hardware+software (Boston Dynamics/Hyundai ecosystem, industrial automation firms). Goldman Sachs’ $38bn humanoid TAM by ~2033 implies incremental demand for high-margin GPUs and sensors, potentially adding a low-single-digit percent to NVDA revenue annually over 3 years if adoption accelerates; low-skill labor in repetitive manufacturing is the most exposed. Increased robot deployment raises OEM bargaining power for compute and sensors, tightening pricing power for best-in-class suppliers while pressuring commodity hardware margins. Risk assessment: Tail risks include regulatory limits on worker-displacing robots, export controls on AI chips (US-China), and high-profile operational failures triggering liability suits; any of these could cut adoption by >30% versus base. Time horizons differ: market sentiment and NVDA options react in days–months to demos/earnings; real factory substitution plays out over 1–5 years. Hidden dependencies: supply of precision actuators, battery density, and local service networks — failure in any adds cost+delay. Trade implications: Direct actionable bias is long NVDA (capture compute moat) and selective long exposure to industrial automation integrators; tactically short/underweight TSLA on humanoid execution risk. Use 6–12 month call spreads on NVDA to buy upside while funding with OTM sells; pair trade: long NVDA vs short TSLA to isolate compute vs execution risk. Rotate portfolios into Industrials/Capital Goods (automation equipment) and away from low-margin labor-heavy discretionary names over 3–18 months. Contrarian angles: Consensus underestimates integration complexity — widespread humanoid deployment may take 5–10 years, not 1–2, compressing near-term monetization and leaving NVDA exposed to margin normalization as GPUs commoditize. Historical parallel: industrial robotics adoption was multi-decade; expect boom-bust capex cycles, spiking demand for maintenance/insurance services — consider service-heavy names and after-market plays as durable beneficiaries.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment