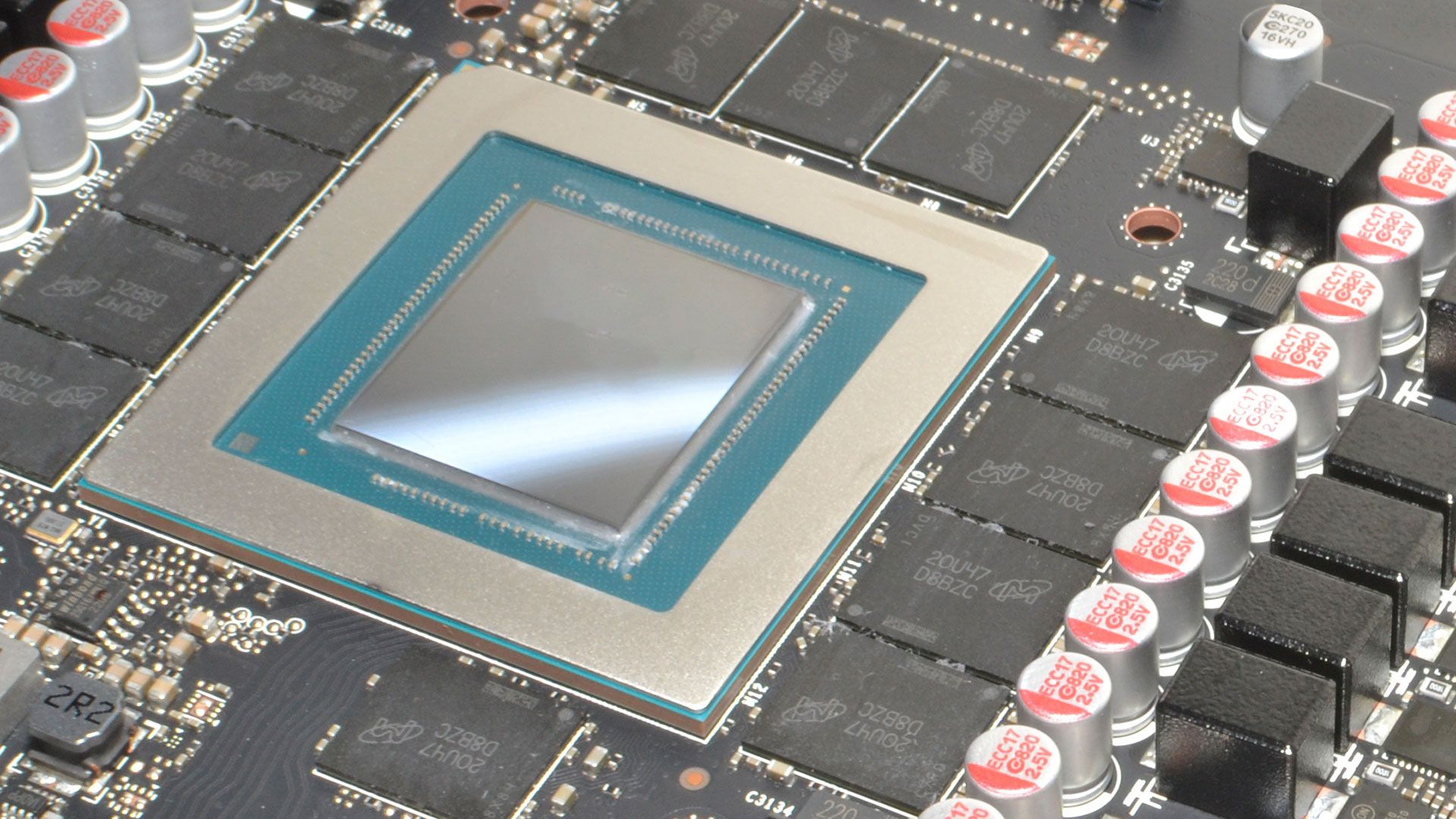

Nvidia is reported to have stopped bundling VRAM with GPU dies sold to add-in-board (AIB) partners, leaving vendors to source GDDR from memory suppliers (Samsung, Micron, SK Hynix) amid an AI-driven global memory shortage. If true, smaller AIBs could face margin compression and higher costs, potentially driving GPU price inflation and supply fragmentation, while Nvidia may forgo module markups—however the report remains an unverified rumor and implications for Nvidia revenue and supplier dynamics are uncertain.

Market structure: If true, memory OEMs (MU, SSNLF, 000660.KS) are primary beneficiaries from immediate upward price pressure on GDDR/DRAM while smaller AIBs (Zotac, Colorful, public peers like 2357.TW ASUS, 2376.TW Gigabyte) face margin compression and potential market share loss to large integrators. Nvidia (NVDA) retains product control and downstream pricing power for dies but may cede ancillary margin from bundled memory sales; expect SKU fragmentation and higher retail GPU ASPs (+10–30% possible in stressed memory scenarios over 1–3 months). Risk assessment: Tail risks include antitrust/regulatory action if Nvidia is seen to leverage supply to squeeze partners, a sudden memory capex surge that collapses GDDR pricing (histor DRAM cycle declines >40% within 12–18 months), or export controls that re-route supply. Short-term (days–weeks) volatility around leaks and partner statements, medium-term (3–9 months) margin re-pricing for AIBs, long-term (12–36 months) depends on memory capex and AI demand elasticity. Trade implications: Direct plays favor long positions in memory producers (MU) and selective long NVDA exposure on pullbacks (add on 8–12% dip) while trimming small-cap AIB equities and GPU-dependent consumer hardware names (e.g., CRSR) over 3–6 months. Use pair trades (long MU, short 2357.TW or 2376.TW) to isolate memory vs. board manufacturing risk; consider buying 3–6 month MU call spreads funded by selling short-dated NVDA covered calls if IV aligns. Contrarian angles: Consensus emphasizes NVDA hurt by vendor friction, but market may underprice NVDA’s leverage—if Nvidia refuses to bundle it preserves manufacturing cadence and can prioritize AI SKUs, protecting core revenue; conversely memory rallies are cyclical and can reverse sharply once suppliers increase fab allocation. Historical parallel: 2020–22 GPU/DRAM shortages saw 6–12 month overshoots followed by 30–50% DRAM price corrections; avoid one-way bets without capex/cycle confirmation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.42

Ticker Sentiment