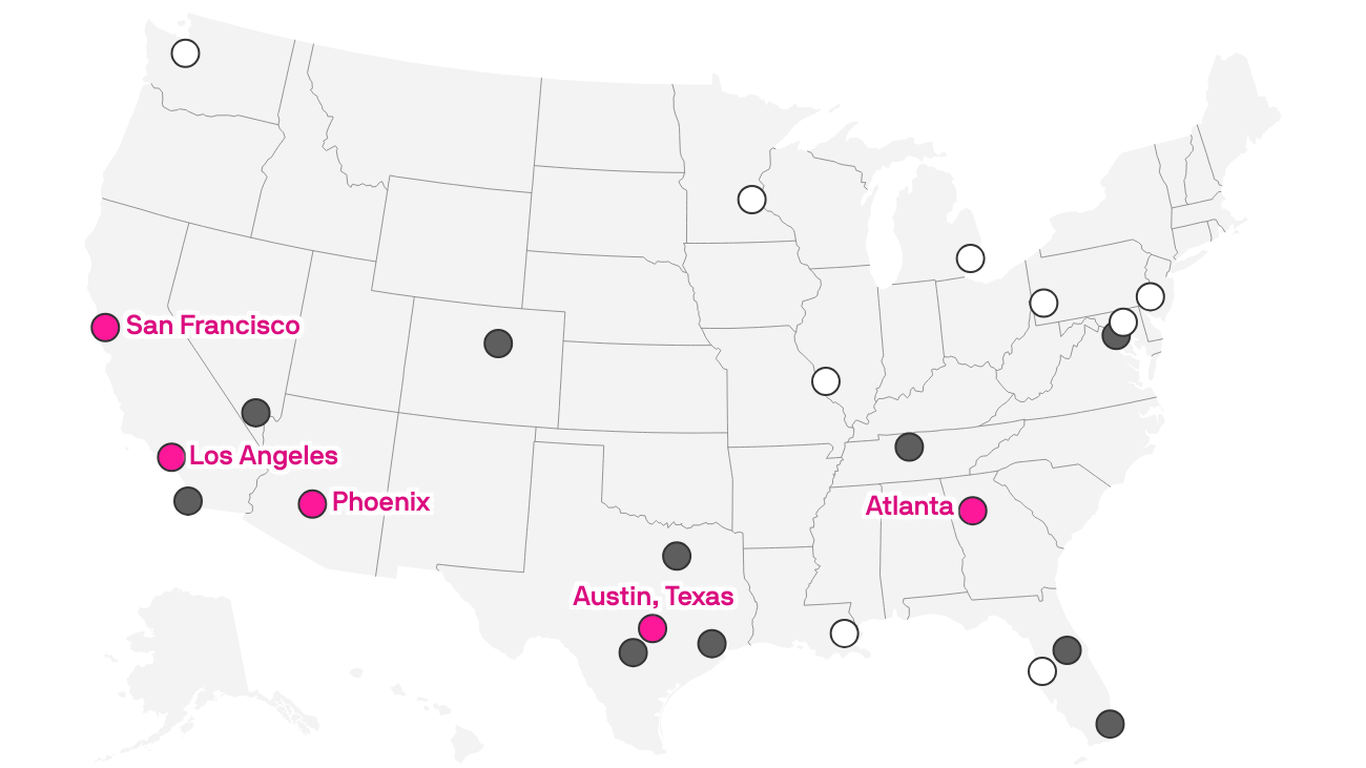

Waymo, operating roughly 2,500 robotaxis across five U.S. cities and claiming more than 100 million fully autonomous miles, is pursuing a rapid expansion into roughly 19 additional cities (four newly announced: Baltimore, Philadelphia, Pittsburgh and St. Louis) but is encountering significant local political and regulatory resistance. Several jurisdictions (e.g., New York, D.C.) require human operators or need legislative changes, while cities such as Boston, Seattle and Minneapolis are debating or proposing ordinances that could ban driverless operations; Waymo has replaced its global head of public policy and hired lobbyists as it seeks legal clarity and aims to be ready in D.C. by 2026. For investors, prolonged local legislative battles could materially delay commercialization timelines and chip away at Waymo's early market lead, introducing execution risk to Alphabet's longer-term autonomous-transportation exposure.

Market structure: Waymo’s regulatory friction hands short-term wins to incumbents (local taxi/rideshare networks, unions) and partners like UBER while delaying Waymo’s monetization curve by an estimated 12–36 months. That setback materially reduces Waymo’s incremental pricing power for robotaxi services (pushes unit economics breakeven later) but is unlikely to threaten Alphabet’s core ad/cloud cash flows in the next 12 months. Risk assessment: Tail risks include city/state bans or multi-jurisdiction litigation that could strand capital (write-downs in the high hundreds of millions) and trigger antitrust scrutiny if Alphabet responds with heavy-handed lobbying; likelihood medium with high impact over 6–24 months. Immediate (days) risk = PR-driven volatility; short-term (weeks–months) = municipal ordinance votes; long-term (1–3 years) = altered TAM and higher customer-acquisition costs. Trade implications: Tactical positions should hedge headline risk in GOOGL/GOOG while selectively increasing exposure to UBER as a relative beneficiary of Waymo delays. Use options to buy downside protection on Alphabet (3–6 month 5% OTM puts) and consider a pairs trade long UBER vs short GOOGL to target 15–25% relative outperformance over 6–12 months. Expect modest safe-haven flows into Treasuries if political fights intensify. Contrarian angles: The market underestimates that Waymo’s core business impact on Alphabet fundamentals is small this year (<1% revenue) so any sell-off can be overstated and mean-reverting. Historical parallel: Uber overcame early municipal bans and ultimately expanded — a similar outcome is plausible, meaning short-term regulatory scares can create buying opportunities in select AV supply chain names and in GOOGL if decline >7–10% on regulation news.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40

Ticker Sentiment