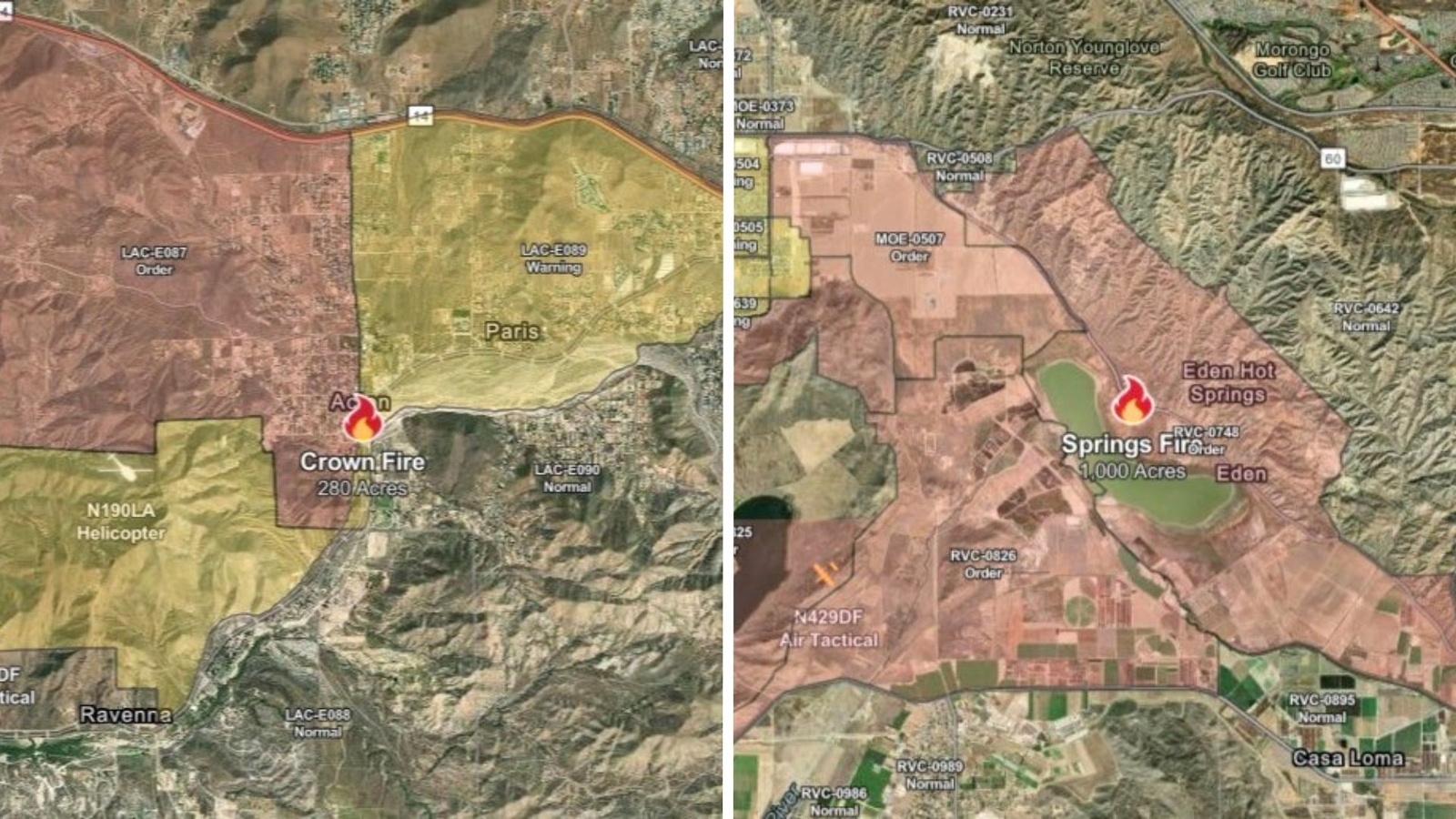

Two wildfires — the Springs Fire (ignited near Gilman Springs Road in Moreno Valley) and the Crown Fire (ignited near Crown Valley and Soledad Canyon Road in Acton) — have triggered evacuation orders and warnings in Riverside and Los Angeles counties. Local evacuations may disrupt residents and transportation routes but are unlikely to have material market-wide or sector-level impact.

Local wildfire events act as stress-tests for three linked asset clusters: utilities with distribution exposure, logistics real estate concentrated in Southern California, and short-tail property insurers/reinsurers. Within 0–30 days expect route and terminal congestion to raise spot freight rates and delivery premiums; that flow benefits last-mile carriers and fuels suppliers on margins while increasing working capital for retailers operating just-in-time inventory. Over 3–12 months, repeated fire seasons accelerate regulatory and insurance repricing — utilities face higher capital and operating scrutiny that can compress equity returns while municipalities absorb emergency expenditures and potential tax base damage. The dominant transmission mechanism is physical damage to distribution infrastructure and the precautionary operational responses (de-energization, road closures), not just burn footprint: small outages cascade into supplier rerouting costs and inventory write-downs for high-turn retailers. Insurers are likely to accelerate underwriting tightening and raise rates regionally, which implies earnings volatility for P&C names and a multi-quarter window for repricing to show up in premiums written. Conversely, capital-light firms providing mitigation services (clearing, brush management, remote sensing software) get higher recurring demand and potential municipal contracting tails. Tail risks include a large, concentrated industrial loss (warehouse cluster damage) that would crystallize multi-billion dollar claims and force broader reinsurance repricing for several quarters; that outcome is low probability but high impact and would pressure regional REITs and insurers for 6–18 months. A reversing catalyst is significant, quick rainfall or regulatory supply of emergency funds that accelerates rebuilding and contract flows to heavy equipment suppliers, shortening the disruption window to weeks. Monitor near-term indicators: grid operator de-energization notices, port/terminal gate throughput, and county permit filings for emergency contracting — each offers a 24–72 hour lead on marketable impacts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00