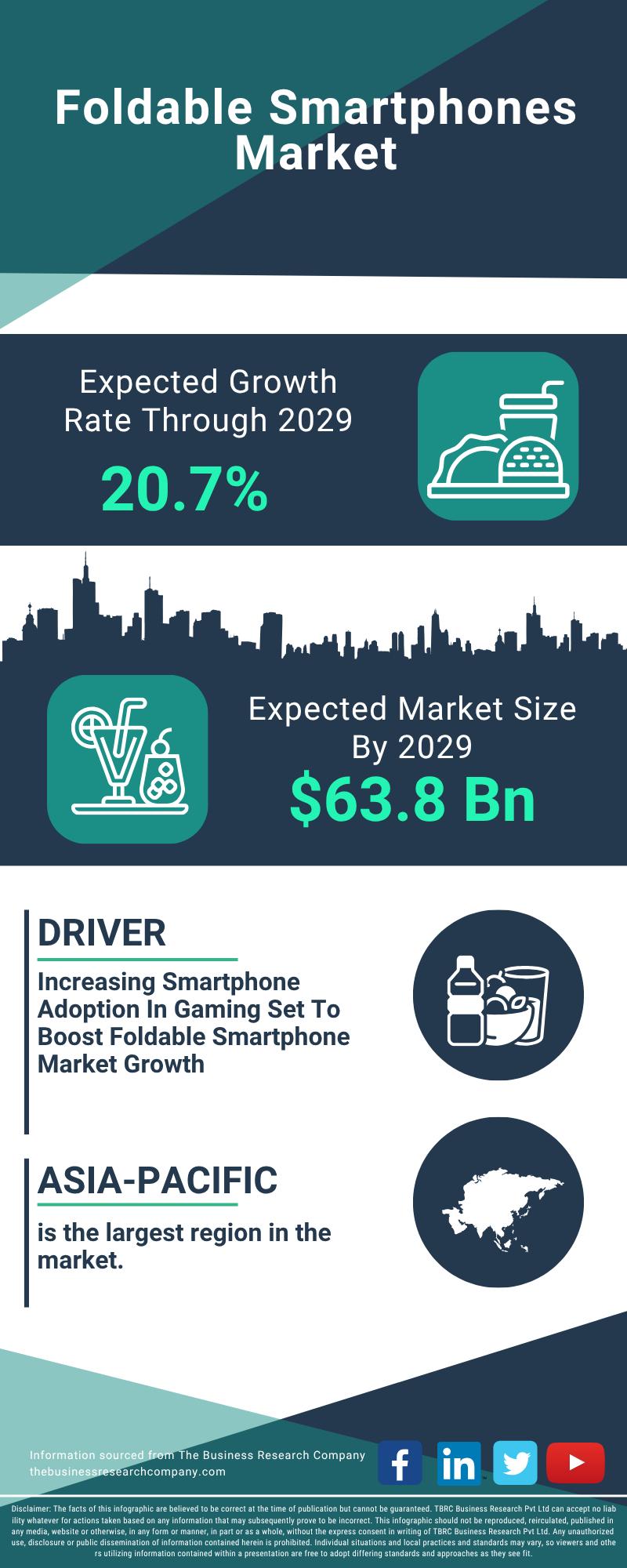

The foldable smartphones market is forecast to reach $63.8 billion by 2029 at a 20.7% CAGR, driven by hybrid work trends, AI integration, 5G rollout and demand for adaptable devices. Major OEMs including Samsung, Huawei, Xiaomi, OnePlus and Google are investing in software optimization and advanced hardware (e.g., Huawei's Sept 2024 Mate XT Ultimate Edition tri-fold with 10.2" OLED, 16GB RAM, up to 1TB storage and 5600mAh battery), while industry themes include multi-cloud adoption, data privacy/regulatory compliance and energy-efficient infrastructure. The report highlights segmented demand (inward/outward fold, OS, RAM tiers, sales channels) that can guide sector allocation but is unlikely to move broad markets immediately; it is more relevant for thematic and stock-level positioning in device makers, display and hinge suppliers.

Market structure: Foldables reallocate premium smartphone profits toward OEMs with scale in flexible OLEDs, hinge IP, and glass (Samsung, BOE/Visionox, Schott) while compressing mid‑tier smartphone margins that can’t justify +30–50% ASPs. Expect pricing power for proven suppliers to persist near term; as capacity ramps ASPs should decline ~15–30% over 24–36 months, shifting economics from margin expansion to volume-led growth. Risk assessment: Key tail risks are regulatory export controls (China/Taiwan), a component yield shock (display/hinge yield <80% for 2 consecutive quarters), or a high durability recall (>3% return rate) that would stall adoption. Immediate moves will be news‑driven (days); expect product cycle and holiday sales to drive performance in 1–6 months; structural adoption and supply‑chain capex play out over 2–5 years. Trade implications: Tactical long exposure to panel/glass suppliers and select SoC/memory names is favored ahead of 2H product ramps; hedge execution risk with options given binary durability headlines. Rotate into materials, panel fabs, and selected semiconductor vendors while trimming pure play midrange OEMs and tablets likely to face cannibalization. Contrarian view: Consensus assumes steady 20%+ CAGR — what’s missing is app/ecosystem lock‑in and return rates; if developer optimization and carrier subsidies lag, adoption could be 30–50% below consensus by 2026. Historically (early OLED phones) ASPs collapsed once yields improved; similar mean reversion could punish late entrants and overvalued component suppliers that ignore capex intensity.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment