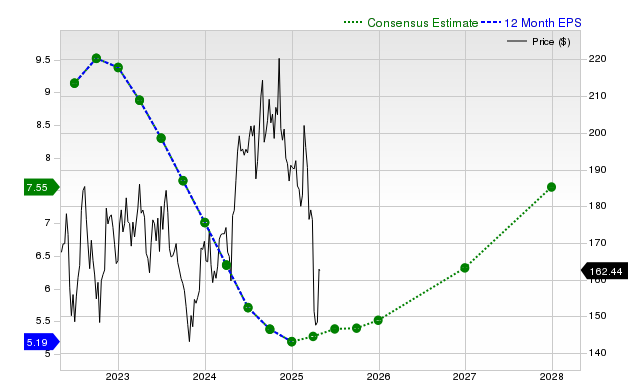

Texas Instruments (TXN) shares have recently underperformed, declining 4.8% over the past month against the S&P 500's 2.4% gain and its industry's 2.4% loss. Despite this, the chipmaker has consistently beaten consensus revenue and EPS estimates in its last four quarters, with its most recent report showing a 16.4% year-over-year revenue increase to $4.45 billion and a 6.82% EPS surprise. While current and next fiscal year earnings and revenue estimates project continued growth, they have remained stable over the past 30 days, and TXN's 'D' Zacks Value Style Score indicates it trades at a premium to peers, resulting in a Zacks Rank #3 (Hold) suggesting expected near-term market-perform.

Texas Instruments (TXN) presents a mixed profile, characterized by strong operational performance juxtaposed with recent stock underperformance and valuation concerns. The company's shares have declined 4.8% in the past month, lagging both the S&P 500's 2.4% gain and its own semiconductor industry's 2.4% loss. This price action contrasts with a robust history of execution, including beating consensus revenue and EPS estimates for the last four consecutive quarters. In its most recent report, TXN posted revenue of $4.45 billion, a 16.4% year-over-year increase and a 3.22% surprise, while EPS of $1.41 exceeded estimates by 6.82%. Forward-looking consensus estimates remain positive, projecting 12.9% revenue growth and 7.7% EPS growth for the current fiscal year, with next year's EPS expected to grow by 14.8%. However, these estimates have remained unchanged for the past 30 days, contributing to a Zacks Rank of #3 (Hold) and suggesting a lack of immediate upward catalysts. This neutral outlook is further compounded by a rich valuation, as indicated by a Zacks Value Style Score of 'D', which signifies the stock is trading at a premium to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment