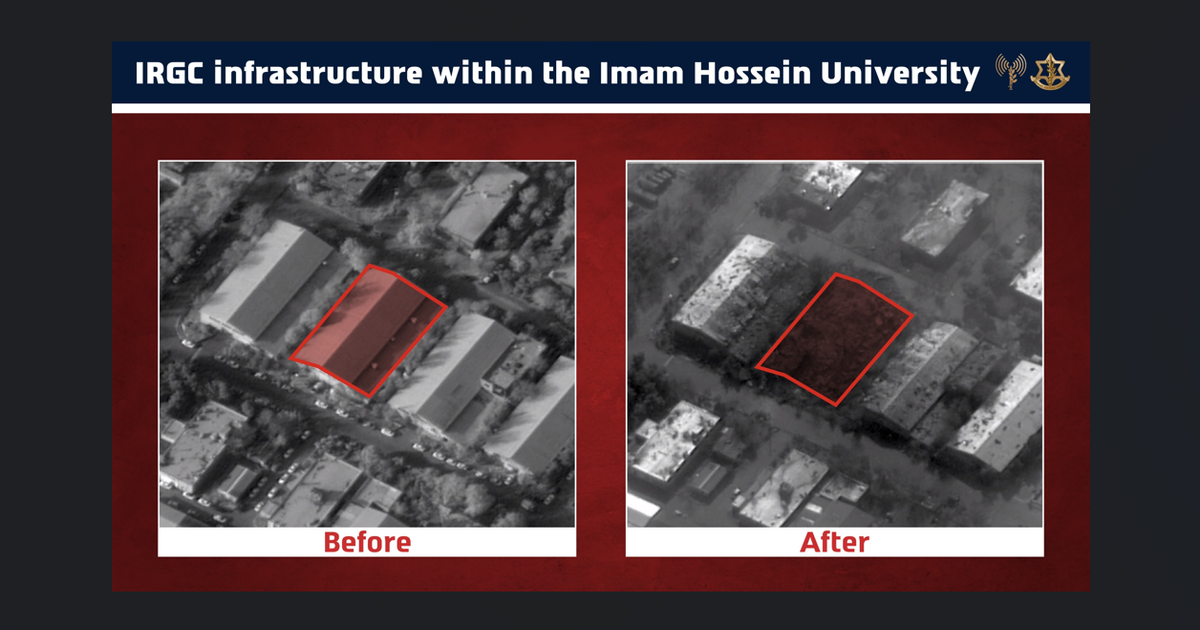

Israel struck Imam Hossein University in Tehran, citing IRGC-linked weapons development targets (wind tunnels, chemistry center, engineering facilities). Former US President Trump threatened strikes on Iranian energy and water infrastructure if the Strait of Hormuz is not reopened, elevating the risk of attacks on oil assets and broader escalation. Iran’s envoy’s refusal to leave Lebanon amid political pushback increases regional political friction and heightens downside risk for markets, likely driving risk-off flows and upward pressure on energy prices.

Markets are re-pricing an elevated probability of regional disruption to energy flows and state-backed escalation, which acts as an insurance premium on oil, freight and political-risk-sensitive assets for the next several weeks. Around 20% of seaborne crude transits chokepoints; even a short-duration insurance or routing shock can lift spot tanker rates and war-risk premia by multiples within 7–30 days, transmitting to refined product spreads and EM FX volatility. The mid-term (1–6 months) winners are those with high operating leverage to spot crude and freight — unconstrained US tight oil can respond only on a months cadence, so majors and shipping owners capture the near-term surplus margin while shale re-enters over a longer timeframe. Reinsurers/insurers and select defense contractors stand to see order and pricing tails, but their revenue recognition lags; expect 6–12 month earnings flow-through rather than immediate EPS shocks. Key catalysts that will govern direction are diplomatic de-escalation talks (trackable via Pakistan/China/Russia backchannels), tactical attacks on export infrastructure (which would materially change export capacity) and coordinated SPR releases; Brent trading above ~$95 historically triggers policy interventions within 30–90 days. Conversely, rapid diplomatic progress or credible assurances for Strait-of-Hormuz transit should compress these premia quickly, delivering mean reversion in oil, freight and risk assets. The consensus risk-off trade may be overdone in duration: the physical oil market has short-duration choke points but ample floating and OECD inventories to blunt a multi-quarter supply shock unless exports from key terminals are physically disabled for months. Position sizing should reflect a high-probability 2–12 week premium capture with disciplined stops for diplomatic resolution or SPR relief that would likely reset prices toward a $70–85 range in 3–6 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.75