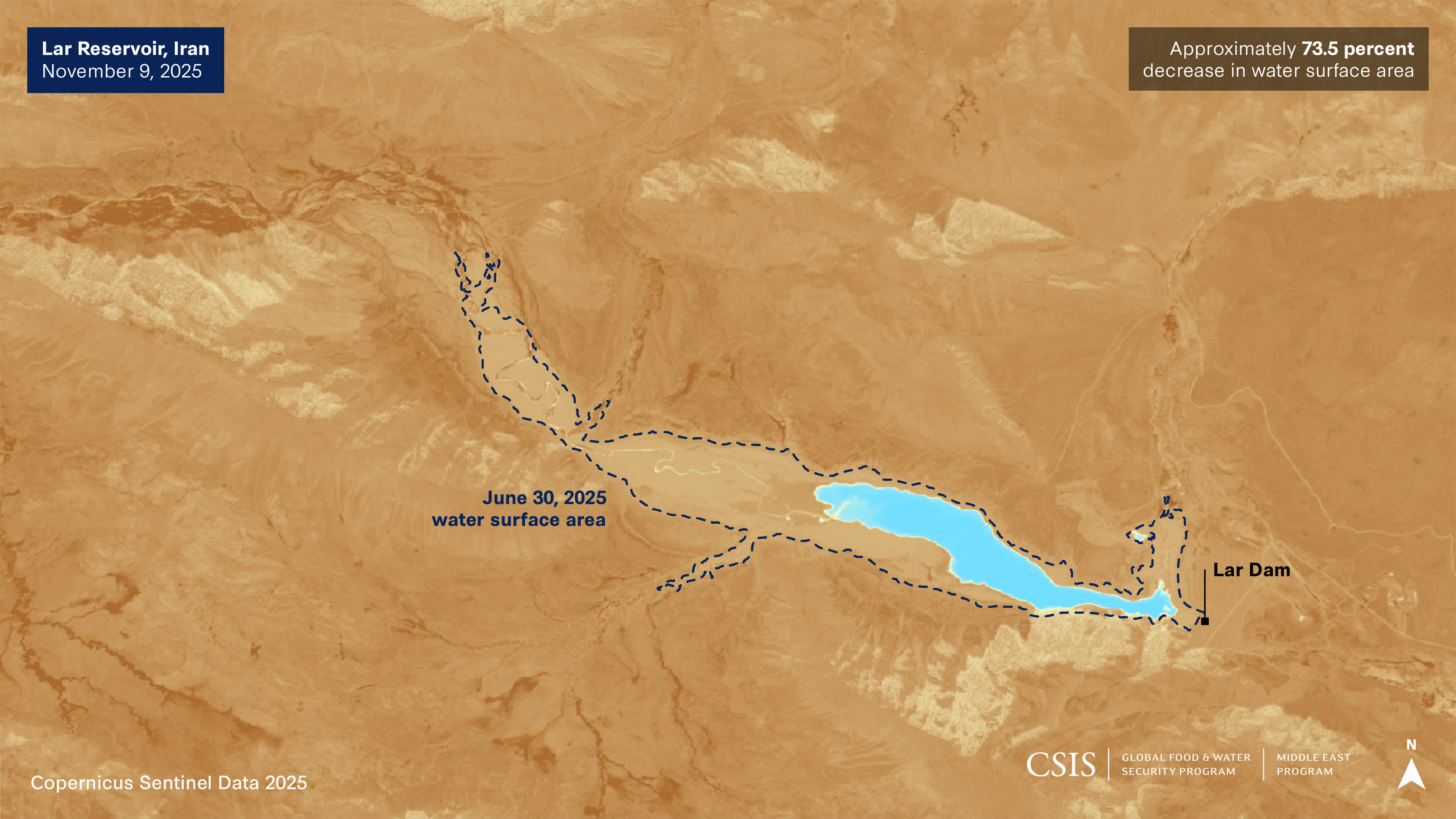

Tehran is facing an acute water crisis driven by prolonged drought, rapid urbanization and chronic mismanagement: surface extent in four of five major reservoirs fell sharply between June and November 2025 (Lar and Latyan down >70%; Taleqan −28%; Amir Kabir −20%; Mamloo −8.5%). The city’s population has doubled since 1979 (4.9m to 9.7m) while annual water use rose from 346m m3 (1976) to roughly 1.2bn m3 today; one-third of supply is lost to leaks/theft and groundwater is being depleted by ~101m m3/year. Authorities are imposing rationing and considering evacuations or even relocating the capital, but reforms (cutting subsidies, curbing agricultural and elite water use) risk social and political instability amid recent war-related pressures and snapback sanctions.

Market structure: Acute municipal water stress in Tehran favors firms and assets that monetize water scarcity — desalination, water utilities with regulated rate-bases, metering/leak-detection tech, and global soft-commodities (wheat/fertilizers) that face production shocks. Losers are Iranian real-estate, Tehran municipal bonds/credit, regional food exporters where production falls, and any local utilities starved of capex by subsidies. Expect pricing power to shift to water-capex vendors and suppliers of short-cycle crop inputs; wheat tightness could push spot/backwardation moves of +5–20% in stressed months. Risk assessment: Tail risks include mass migration/regime stress or a renewed regional conflict that could spike oil +$10–$30/bbl and roil EM credit spreads (days-weeks). Immediate (0–30 days) risk: social unrest from rationing; short-term (1–6 months): commodity swings and municipal defaults; long-term (1–5 years): sustained capex cycle in water tech and potential de-urbanization. Hidden dependency: water–energy nexus (less hydro -> higher gas/coal power use) amplifies commodity price cross-coupling. Catalysts: heavy winter precipitation (reversal), or decisive reforms (tariff hikes) that could reprice demand within 3–6 months. Trade implications: Favor a tactical overweight to listed water infrastructure/technology (12–24 month horizon) and short tail-risk exposure to Iran/nearby EM sovereigns; hedge with commodity long positions (wheat/fertilizer) for 3–12 months. Options: express asymmetric exposure with call spreads on wheat (WEAT or futures) and protective puts on EEM for EM contagion. Sector rotation: reduce financials/real-estate weights in MENA/EM ex-Asia; add industrials (water capex), agricultural inputs, and selective defense contractors for geopolitical risk. Contrarian angles: Consensus underprices the downstream capex opportunity — municipal desperation historically (e.g., Cape Town 2018) produced multi-year procurement and higher margins for water-tech firms. Reaction may be underdone in water equities and overdone in broad EM sell-offs; prices could re-rate if policies force tariff increases (10–30% effective consumer price hikes). Unintended consequence: tariff-driven social unrest could shorten policy windows, creating volatile stop-start capex cycles — favor liquid ETFs and option-defined risk structures.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60