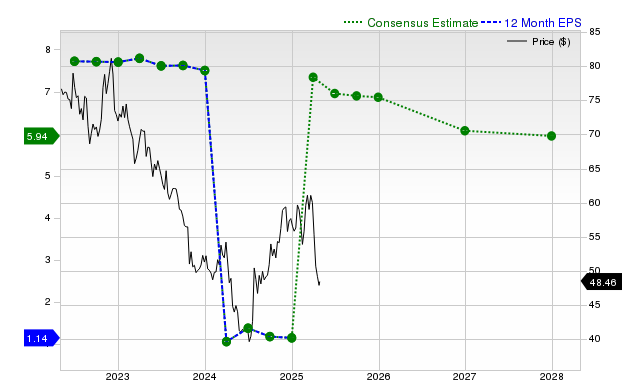

Bristol Myers Squibb (BMY) has recently outperformed its peers, with shares up +6.7% over the past month, and reported a significant beat on Q4 revenue and EPS, marking its fourth consecutive quarter of exceeding consensus estimates for both. However, forward-looking consensus estimates project a decline in current quarter EPS by -8.3% year-over-year to $1.65, alongside anticipated revenue contractions for the current and next fiscal years. Despite a favorable 'A' valuation grade indicating undervaluation relative to peers, BMY holds a Zacks Rank #3 (Hold), suggesting near-term performance in line with the broader market.

Bristol Myers Squibb (BMY) has demonstrated significant recent share price momentum, with a +6.7% return over the past month that outpaces both the S&P 500 composite's +1.6% and its industry's +2.5% gain. This performance is supported by a strong history of exceeding expectations, as seen in the last reported quarter where revenues of $12.27 billion and EPS of $1.46 represented surprises of +7.66% and +36.45% respectively, marking the fourth consecutive quarter of beating consensus on both metrics. However, this backward-looking strength is contrasted by a weakening forward outlook. Consensus estimates project a current quarter EPS decline of -8.3% and revenue contractions of -2.4% for the current fiscal year and -8.2% for the next. While the consensus EPS estimate for the current fiscal year has been revised up by +3.7% over the last 30 days, estimates for the current quarter have been revised down -1.4%. Despite these headwinds, the stock's valuation appears attractive, earning a Zacks Value Style Score of 'A'. The resulting Zacks Rank #3 (Hold) indicates that the negative forward guidance is largely offsetting the positive valuation and recent performance, suggesting the stock may perform in line with the market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.15

Ticker Sentiment