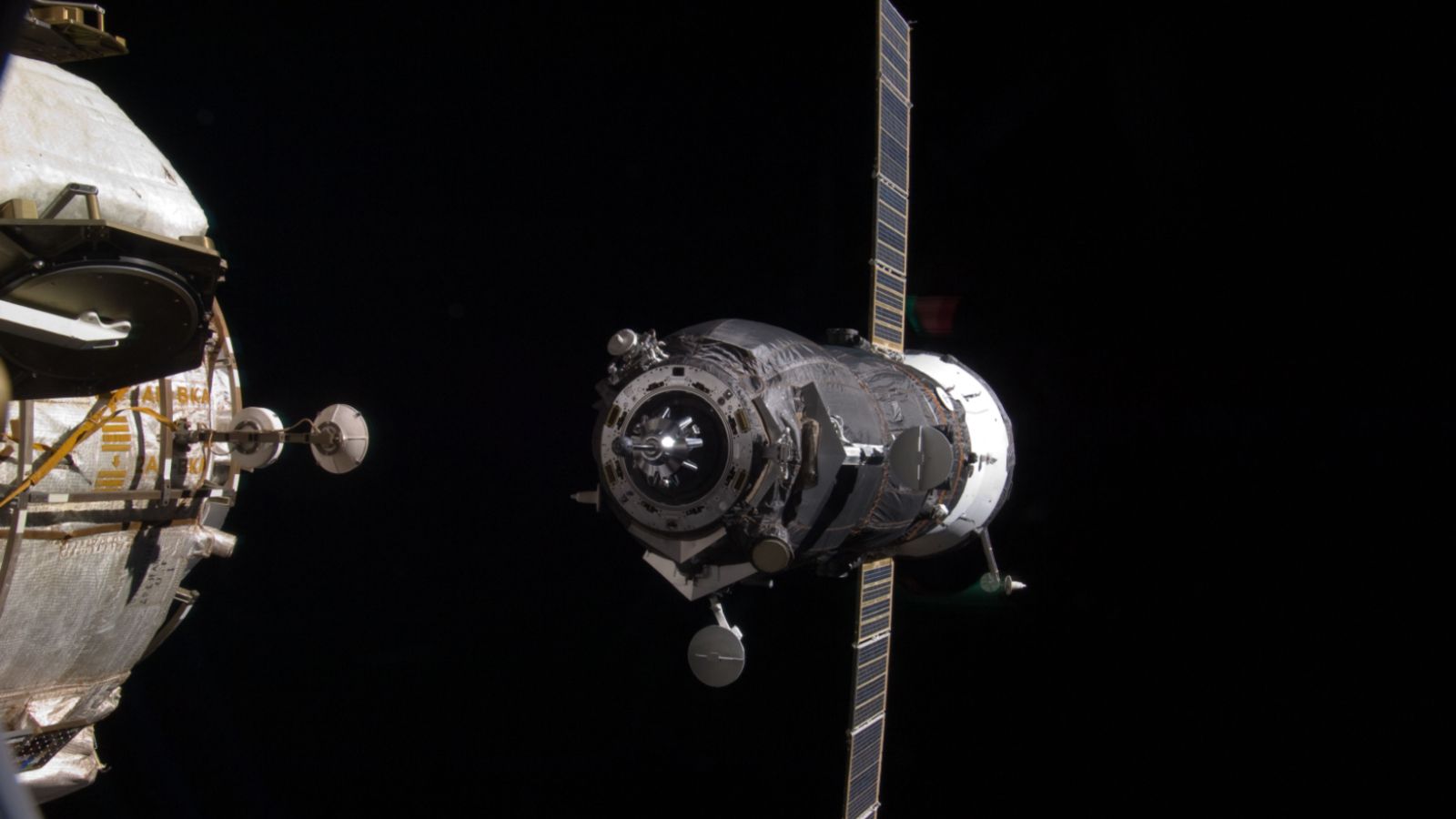

Progress 94 (Progress MS-33) carrying ~5,500 lb (2,500 kg) of cargo failed to deploy an antenna ~40 minutes after liftoff on Mar 22, disabling its planned autonomous docking for Mar 24 (~9:30 a.m. EDT). Roscosmos cosmonaut Sergey Kud-Sverchkov may manually pilot the freighter via a backup system; all other systems are reported nominal and the docking attempt will proceed, implying a localized operational disruption with minimal market impact.

A localized reliability failure in a partner's orbital logistics chain materially raises the probability that mission planners and procurement officers will reprice counterparty risk for station resupply and LEO services. Expect procurement share to shift meaningfully toward commercial Western providers: a 10–25 percentage-point move in awarded cargo/servicing volume over 12–24 months is plausible as agencies prioritize redundancy and predictable SLAs. This reallocation will compress revenue growth visibility for incumbents reliant on single-source contracts and lift firms with modular, certificable flight hardware.

Insurance and indemnity economics are the overlooked transmission mechanism. A cluster of marginal failures increases launch and payload insurance rates by single-digit percentage points, which quickly wipes 1–3% off addressable margins for small-sat operators and squeezes lower-margin launchers — creating a procurement sweet spot for integrators that internalize risk (defense primes and systems houses). Reinsurers will react in weeks; contract repricing follows in 3–9 months as agencies test alternative providers.

Strategically, this accelerates demand for human-in-the-loop rendezvous/docking interfaces, redundant comms suites, and certified rendezvous avionics — durable hardware upgrades with multi-year procurement cycles. Firms that can fast-track flight-proven, modular components stand to capture outsized share because agency selection favors low-integration-risk, COTS-adaptable systems. Conversely, national launch infrastructure that requires heavy rebuild capex faces multi-year underutilization risk if customers shift to lower-friction commercial alternatives.

The market’s likely knee-jerk reaction (short-term bid for “risk-off” aerospace names) underestimates two countervailing forces: (1) accelerated budgetary flows to certified integrators over 6–18 months, and (2) a modest permanent uplift in demand for on-orbit servicing and docking hardware. If you time exposure to capture contract repricing and insurance-driven supplier consolidation, asymmetry is favorable; if you front-run a full geopolitical decoupling narrative, you overpay for downside protection.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00