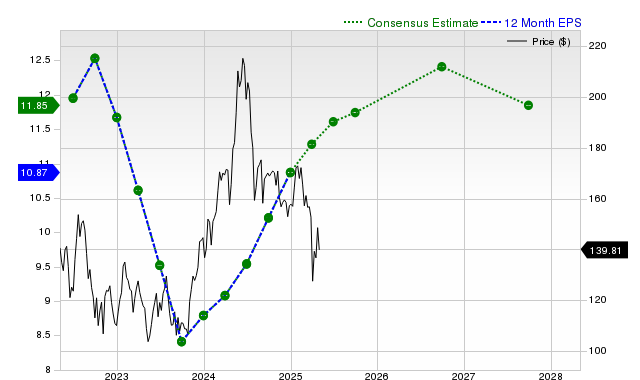

Qualcomm (QCOM) is heavily searched by investors, with shares returning +2.8% over the past month, lagging the S&P 500's +7.2% gain. The consensus earnings estimate for the current fiscal year is $11.81, a +15.6% increase year-over-year, while revenue is projected to grow by +11.8% to $43.54 billion; however, the Zacks Rank of #3 suggests near-term performance in line with the broader market. Qualcomm's valuation receives a grade of B, indicating it is trading at a discount to its peers.

Qualcomm (QCOM) is experiencing heightened investor interest, yet its shares have underperformed the broader market and its semiconductor industry peers over the past month, returning +2.8% compared to the Zacks S&P 500 composite's +7.2% and the Zacks Electronics - Semiconductors industry's +18.1%. The company's current fiscal year outlook indicates robust growth, with consensus earnings estimated at $11.81 per share, a +15.6% year-over-year increase, and revenue projected at $43.54 billion, up +11.8% year-over-year. However, earnings estimates for the current quarter, current fiscal year, and next fiscal year have seen minor downward revisions of -0.1% to -0.2% over the last 30 days. Notably, forecasted growth decelerates significantly for the next fiscal year, with revenue anticipated to increase by a modest +1.3% and EPS by +3.2%. Despite this, Qualcomm has a consistent history of exceeding analyst expectations, having beaten both consensus revenue and EPS estimates in each of the trailing four quarters; its last reported quarter delivered $10.84 billion in revenue (+15.4% YoY) and $2.85 EPS. The stock currently holds a Zacks Rank #3 (Hold), suggesting its near-term performance may align with the broader market, while its Zacks Value Style Score of B indicates it is trading at a discount relative to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment