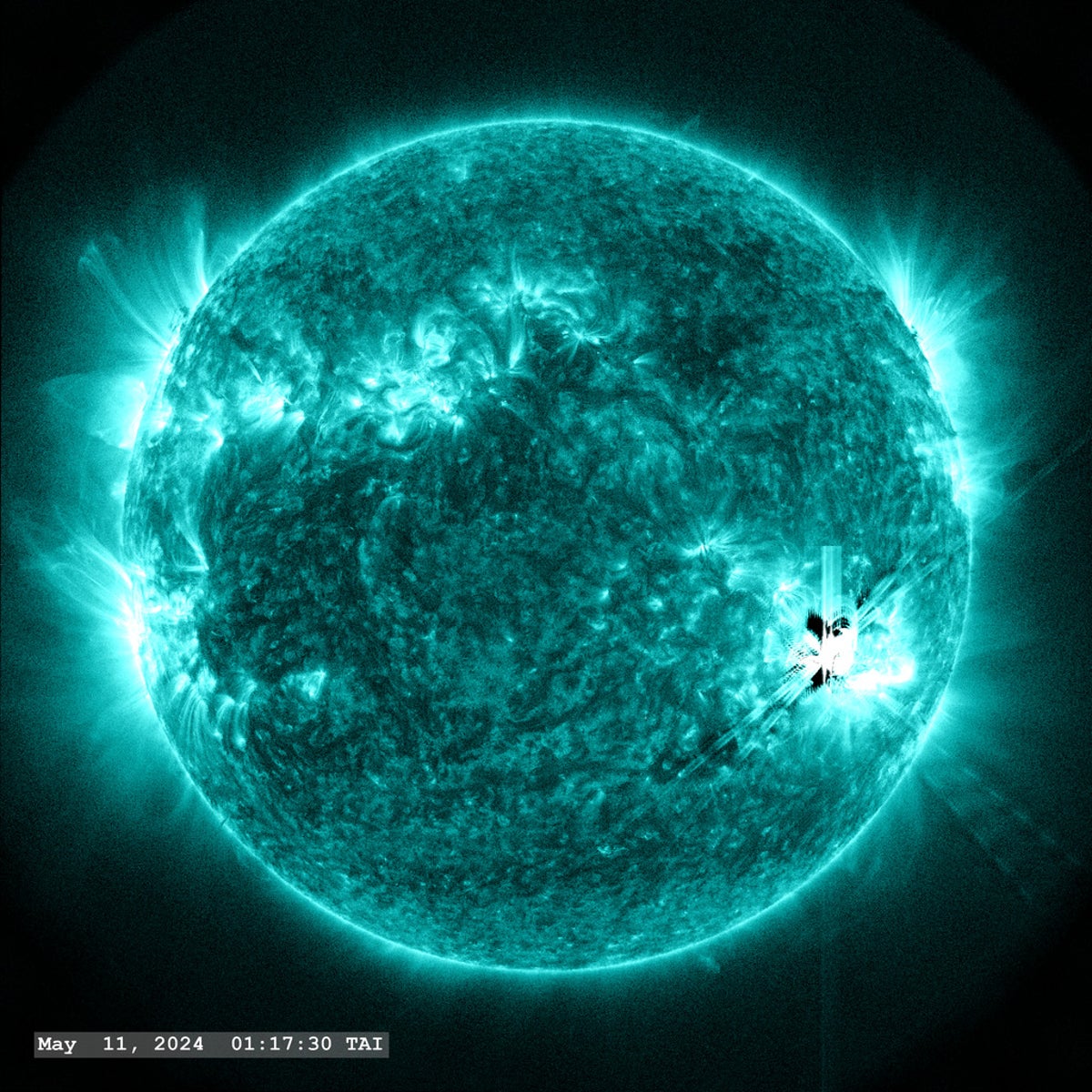

A series of solar flares from active region NOAA 13664 produced some of the worst geomagnetic storms in over 20 years in May 2024, disrupting satellites, GPS, power grids and even railway signalling while casting aurora as far south as Florida. ESA’s Solar Orbiter provided a continuous 94-day observation—the longest-ever for a single active region—tracking NOAA 13664 from a far-side emergence on April 16, 2024 until it rotated out of view after July 18, 2024; the dataset could improve forecasting but underscores ongoing operational risks to utilities, satellite operators, insurers and transport networks.

Market structure: Major near-term winners are grid hardening and defense/space-infrastructure suppliers (transformer/HV equipment makers, satellite sensor contractors) while commercial satellite operators, GPS-dependent logistics and some insurers face revenue and loss volatility. Pricing power shifts toward suppliers of specialized hardware/software (ABB, ETN, LHX, RTX, LMT) because a single large geomagnetic event can force accelerated capex; demand for monitoring/forecasting data rises but remains lumpy. Cross-asset: expect short-lived risk-off flows into US Treasuries and gold on major storms, USD strength intraday versus EM, and spikes in implied volatility for aerospace/satellite equities and related options. Risk assessment: Tail risks include a Carrington-level event (>~$50–100B insured loss) or cascading transformer failures, which would force multi-year utility capex and regulatory intervention; probability low (<1%/year) but fiscal implications large. Immediate horizon (days) is elevated operational risk to satellites/GPS; 1–12 months sees contract awards and insurance repricing; multi-year horizon (2–5 years) supports sustained capex in grid resilience. Hidden dependencies: GPS outages compound logistics/FX settlement, and insurance re-underwriting could tighten capital for satellite operators. Catalysts: NOAA/ESA funding announcements, a repeat storm, or a high-loss insurance payout within 90–180 days. Trade implications: Direct plays: overweight industrials/defense suppliers with proven space-weather product lines (ABB/ETN/LHX/RTX/LMT) for 6–24 month rehabbing cycle; underweight or hedge commercial GEO satellite operators (VSAT, MAXR exposure) for 0–12 months. Options: buy 3-month ATM straddles on small-cap satellite operators (VSAT) if IV <80% expecting event-driven spikes, and buy 9–18 month LEAPS calls on ETN/ABB as asymmetric long. Sector rotation: shift 3–6% portfolio weight from consumer discretionary/airlines to industrials, utilities and defense over next 3 months. Contrarian angles: The market underestimates regulatory acceleration—if a mid-sized event (> $5B insured) occurs, capex timelines compress and winners outperform by 20–40% over 12–24 months; conversely, over-allocating to satellite names post-storm is risky because replacement cycles and insurance limits can depress returns. Historical parallels: post-1989 and 2003 storms saw multi-year utility investment cycles; current low interest rates are gone, so financing cost will temper speed. Unintended consequence: defense/space names may face procurement delays from budget politics—stagger entries and size positions to event/catalyst triggers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30