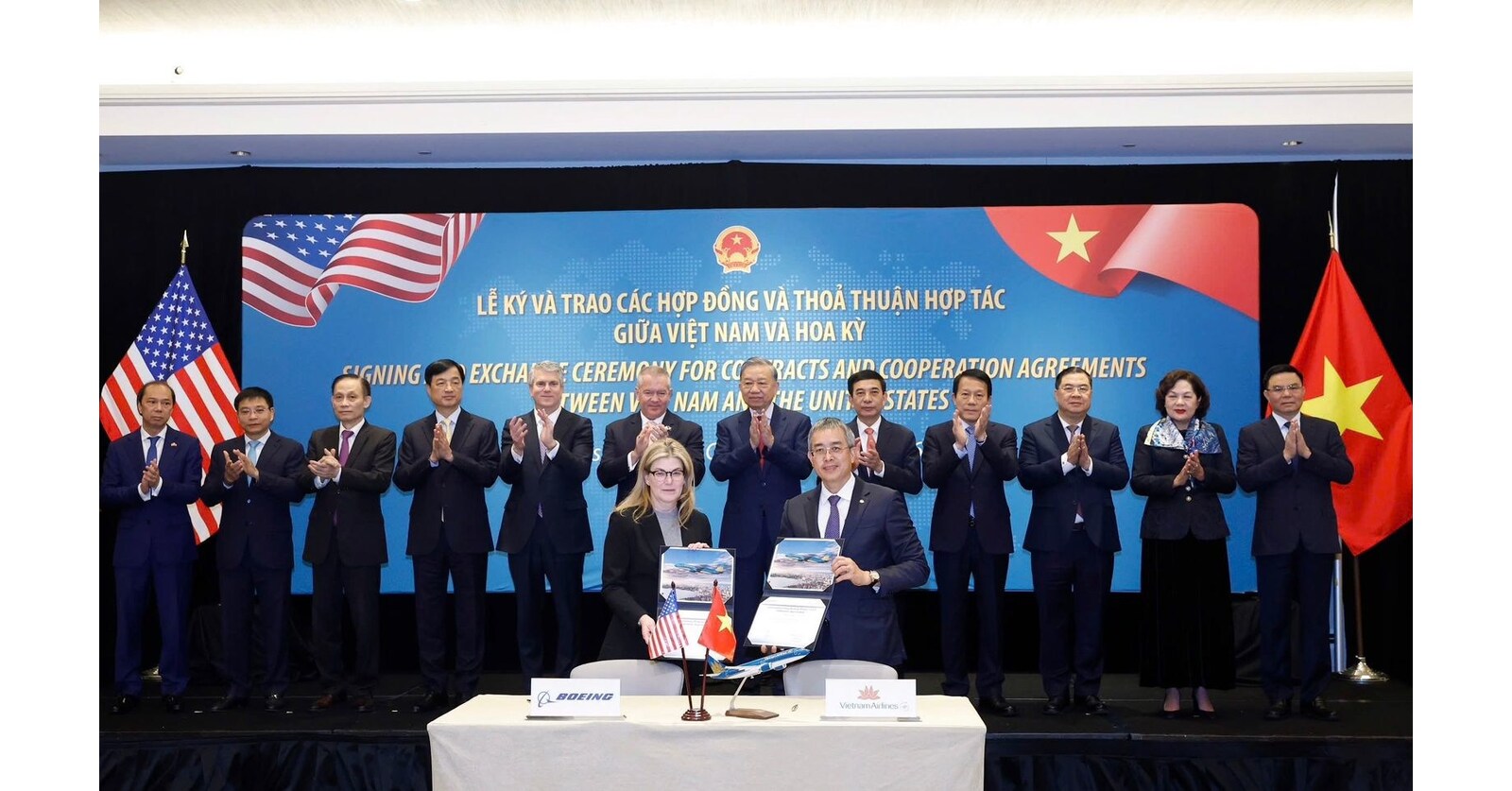

Boeing (NYSE: BA) announced a firm order from Vietnam Airlines for 50 737-8 (737 MAX) single-aisle aircraft to support the carrier's domestic and regional expansion as Vietnamese air traffic is expected to double to over 75 million annual passengers in the next decade. The 737-8, which carries up to ~200 passengers with a range of ~3,500 nm, will complement Vietnam Airlines' 17 787 Dreamliners and is cited to deliver 20–25% fuel-use improvements versus replaced types, reinforcing fleet modernization, lower unit operating costs and deeper Boeing commercial and supply-chain engagement in Vietnam.

Market structure: Vietnam's 50-aircraft 737‑8 order is a modest but concrete win for Boeing (BA) and Tier‑1 narrowbody suppliers (Spirit AeroSystems SPR, Hexcel HXL) with an estimated list value ~ $5–6B (discounted in practice). It raises Boeing's near‑term narrowbody backlog utilization and aftermarket/MRO revenue potential in Southeast Asia as pax demand there is forecast to double to ~75m over 10 years. Airbus (AIR.PA / EADSY) faces incremental competitive pressure on regional share, but impact on global pricing is limited — this is demand expansion, not a price war yet. Risk assessment: Near term (days–weeks) expect a modest BA share bounce; short term (months) execution risk centers on delivery cadence, financing terms and engine supplier (CFM) capacity; long term (years) upside depends on Vietnam hitting fleet growth targets. Tail risks: renewed MAX regulatory probes, supply‑chain bottlenecks, or Vietnam budget/FX stress delaying financing (high impact, low prob). Hidden dependency: political signaling (U.S.–Vietnam ties) may have negotiated offsets or industrial offsets that change cash timing. Trade implications: Tactical: initiate a modest 1.5–3% portfolio long in BA via a 9–15 month call spread to capture 20–40% upside while limiting capital at risk; size 1–2% long positions in SPR and HXL (beneficiaries of production ramp). Pair trade: long BA / short AIR.PA (equal notional) to isolate Boeing execution vs Airbus exposure. Enter within 2–6 weeks; trim if BA rises >30% or if Boeing revises delivery schedule downward by >20%. Contrarian angles: The market underestimates timing risk — orders often stagger over 3–7 years, so revenue recognition is slow; the headline can overstate near‑term cash flow. Conversely, consensus may underprice aftermarket and training revenue (higher margin) that accrues over the life of each aircraft. Historical parallels: large state‑backed airline orders have frequently been delayed or restructured (2010s), creating both latency and pricing opportunities; watch for MRO/MRO supply stress as a choke point that could flip positive headlines into execution risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment