The article evaluates the utility of Average Brokerage Recommendations (ABR) for investment decisions, using Delta Air Lines (DAL) as a case study, which currently holds a 'Strong Buy' equivalent ABR of 1.29 from 21 firms. It cautions against sole reliance on ABRs due to inherent positive bias and potential for being outdated, advocating instead for the Zacks Rank, a quantitative model driven by timely earnings estimate revisions. For DAL, a 2.4% increase in the Zacks Consensus Estimate to $5.76 over the past month has resulted in a Zacks Rank #2 (Buy), indicating a legitimate basis for potential near-term stock appreciation, with the ABR serving as a corroborating factor.

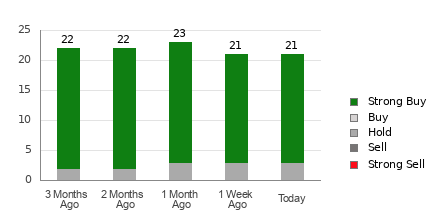

Delta Air Lines (DAL) exhibits strong bullish sentiment from sell-side analysts, evidenced by an Average Brokerage Recommendation (ABR) of 1.29, which falls between a 'Strong Buy' and 'Buy'. This consensus is based on 21 brokerage firms, of which 18, or 85.7%, rate the stock a 'Strong Buy'. However, the more significant driver for a positive near-term outlook is the trend in earnings estimate revisions. The Zacks Consensus Estimate for DAL's current-year earnings has increased by 2.4% over the past month to $5.76, signaling growing analyst optimism regarding the company's fundamental earnings prospects. This upward revision underpins the stock's Zacks Rank #2 (Buy), a quantitative rating identified as having a stronger correlation with future price performance than potentially biased ABRs. The alignment of the broad sell-side consensus with this more objective, earnings-driven quantitative signal provides a robust foundation for the current positive outlook on the stock.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.60

Ticker Sentiment