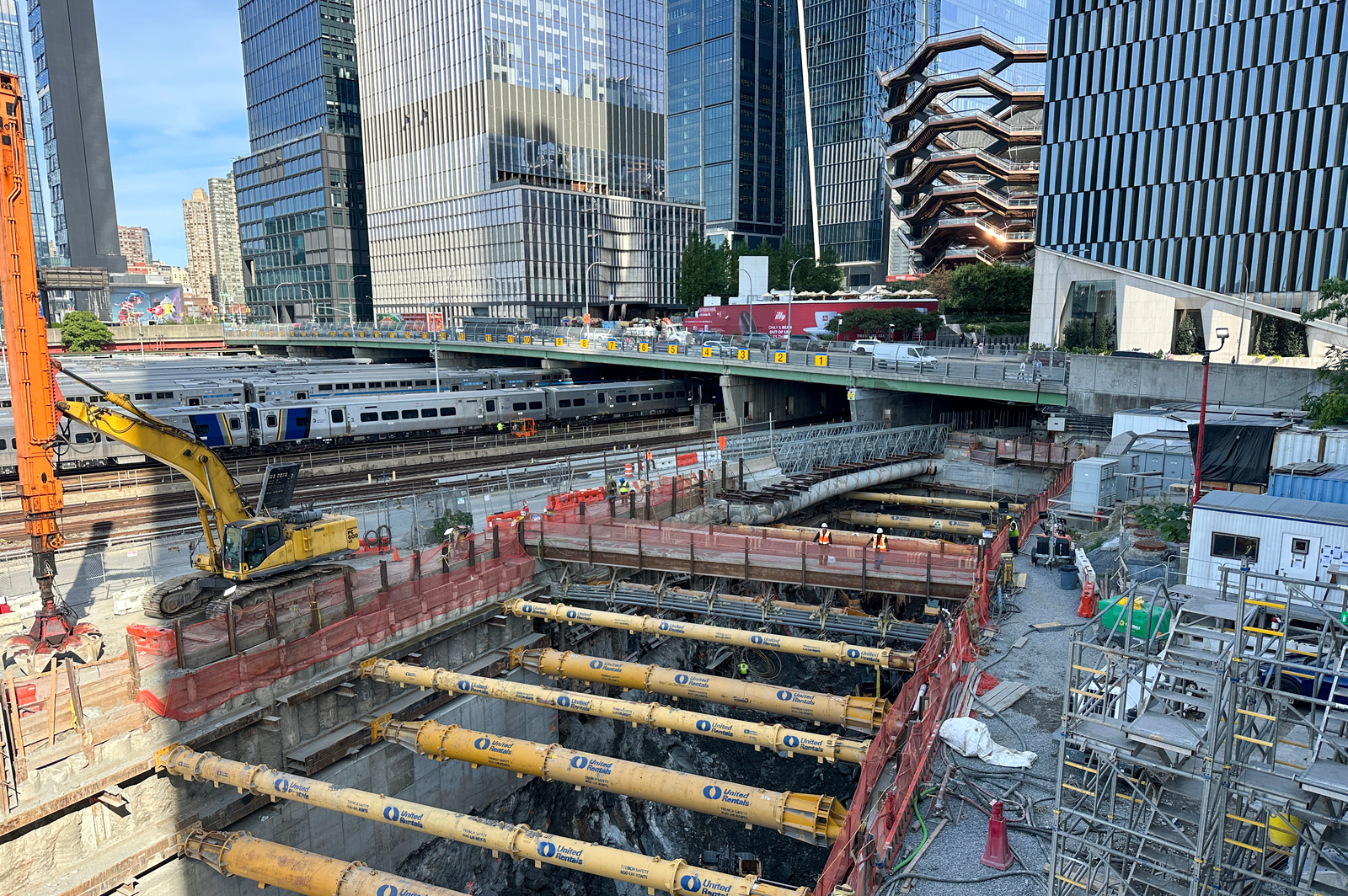

New York and New Jersey filed lawsuits after the Trump administration froze roughly $15–16 billion in federal funding for the Hudson River Gateway rail tunnel, alleging the U.S. Department of Transportation unlawfully withheld payments (including a contested ~$205 million tranche) and breached contractual obligations. With about $1 billion already spent, federal funding covering roughly three quarters of the $15 billion project, officials warn construction and tunneling work could halt within days, creating execution risk for contractors, potential job losses, and disruption for ~200,000 daily riders while courts weigh expedited relief.

Market structure: The immediate winners are smaller, bridge/tunnel contractors and engineering firms with existing Gateway contracts (Jacobs J, AECOM ACM, Caterpillar CAT via equipment demand) if funding is resumed; losers are NYC/NJ transit-adjacent real estate (SLG, VNO) and subcontractors facing stoppage. Pricing power shifts toward firms with secured federal claims — they can press for change orders or government compensation, increasing near-term working capital needs for others. Across assets, expect short-term safe-haven flows into Treasuries (push down 2s–10s) and a modest bid for industrials on reinstatement rumors; muni spreads for NY/NJ short paper could widen 10–30bp if states bridge financing gaps. Risk assessment: Tail risks include a multi-quarter contract termination (high-impact, <20% prob) that forces write-offs for contractors and orphaned sunk-costs of $1–3bn; another tail is a court injunction forcing immediate payments (30–40% chance within 30–90 days). Immediate window (days): construction cashflow crunch and idled labor; short-term (weeks–months): credit lines drawn by contractors and muni issuance; long-term (years): timeline slip increases capex and cost inflation + potential federal policy precedent. Hidden dependency: contractor margins tied to continuing federal reimbursements and union labor deals — stoppage increases renegotiation risk and claims. Trade implications: If you expect reinstatement within 3–6 months, buy selective 9–15 month call spreads on J and ACM sized 1–3% portfolio each (caps downside, levered upside). Hedge industrial exposure with a 1–2% notional 1–3 month put spread on XLI (buy ~3% OTM, sell ~8% OTM) to protect against funding cancellation. Increase short-term duration by overweighting 7–10yr Treasuries (IEF) by 2–4% for 1–3 months to capture risk-off downside in yields; establish a tactical 1–1.5% short in NYC-focused office REITs (SLG or VNO) for 3–12 months. Contrarian angles: The market underprices legal resolution probability — courts historically favor contract/appropriation enforcement in <90 days, so deep OTM long-dated calls on J/ACM (12–18 months) may be underpriced relative to binary upside. The reaction may be overdone for diversified engineering firms with non-Gateway backlog; their cash buffers could absorb a 60–90 day pause. Historical parallel: federal project funding fights (Big Dig-era disputes) produced short-term stops but eventual settlements with contractor claims paid; that favors disciplined, duration-aware long exposures over outright panic shorts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45