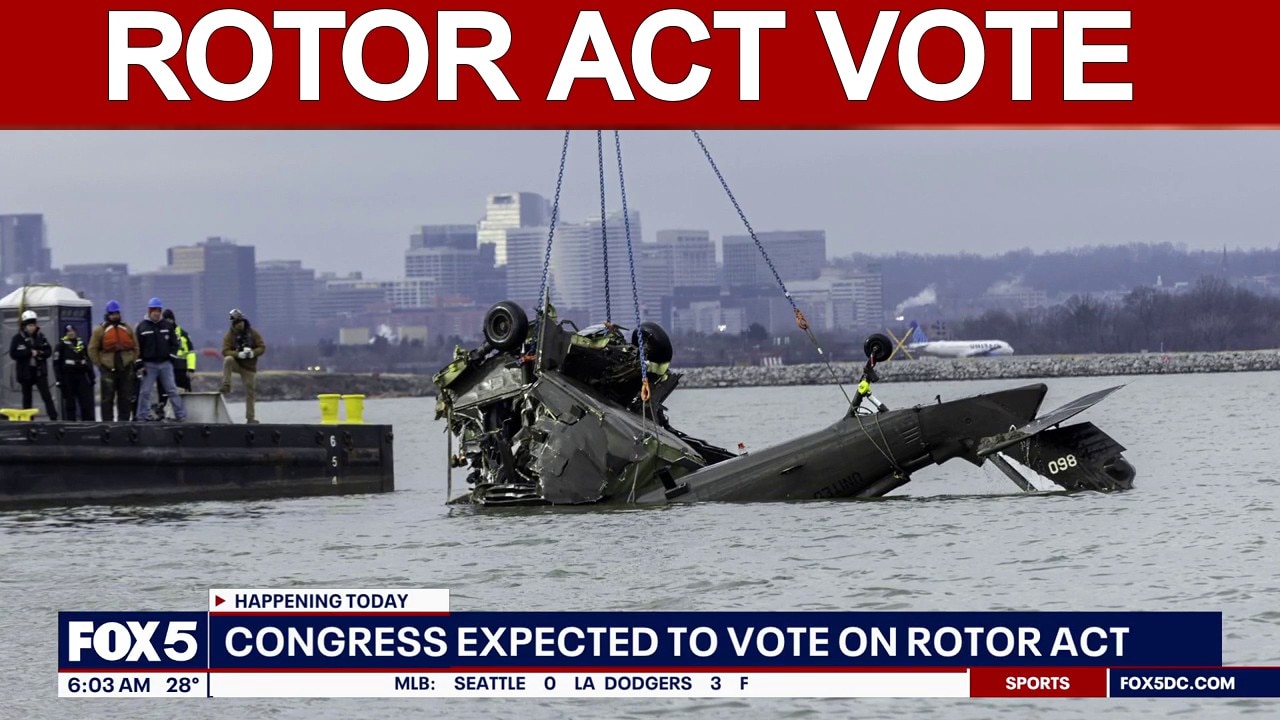

The House blocked the ROTOR Act in a 264-133 vote after the bill, which had already passed the Senate, failed to reach the greater-than-two-thirds threshold required under expedited procedures. The legislation would have mandated ADS‑B In aircraft locator systems around busy airports — technology the NTSB has recommended since 2008 and which investigators say could have prevented last year’s midair collision that killed 67 — but competing broader House legislation backed by airlines, the military and general aviation groups is expected to be advanced in committee soon. Lawmakers and victims’ families indicate continued debate on aviation safety reforms, leaving regulatory outcomes and industry compliance costs unresolved in the near term.

Market structure: Immediate winners are avionics and defense suppliers that would capture retrofit contracts (e.g., L3Harris LHX, RTX, Honeywell HON), which gain pricing power for hardware + integration services. Losers are legacy and regional carriers (example AAL) and insurers: mandated retrofits and potential increased liability could compress airline free cash flow by mid-single-digit percentage points annually if installed fleetwide within 2-3 years. Risk assessment: Short-term (days) the House vote removes an immediate regulatory overhang and should cap downside for airline equities; medium-term (weeks–months) committee markups and a competing, broader House bill are main catalysts that could reintroduce mandate risk; long-term (1–3 years) a final mandate could force industry capex in the low hundreds of millions to low billions aggregate (retrofit costs likely thousands–tens of thousands per airframe). Tail risks include a sudden bipartisan push that expands scope (military carve-outs fail) or large settlement judgments that widen airline credit spreads by 100–300bps. Trade implications: Favor selective long exposure to avionics/systems suppliers via defined-cost option structures and underweight or hedge airlines (AAL, JETS). Cross-asset: expect higher implied vols in airline options, modest widening in airline credit spreads, and positive flow into defense names; commodities/FX minimal impact. Contrarian angles: Consensus assumes either immediate mandate or nothing; the real outcome is binary and lumpy—delay increases probability that suppliers secure higher-margin retrofit contracts and capacity constraints (semiconductors, installers) could extend timelines and raise prices. If markets rally on the bill’s failure, that rally may be short-lived once committee activity resumes; asymmetric payoff favors early, limited-cost longs in suppliers and hedges against carriers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment