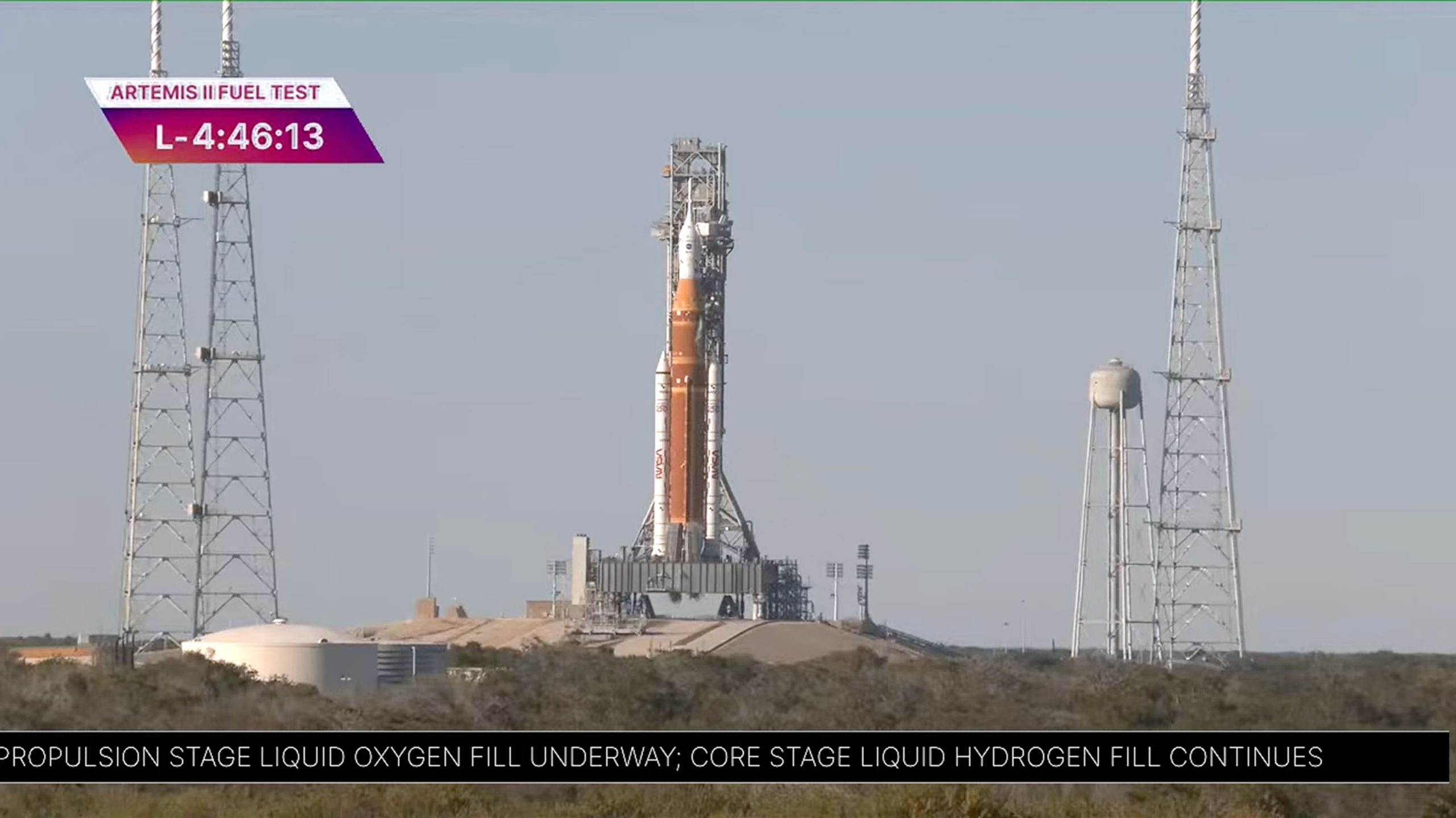

NASA conducted a critical Artemis 2 wet dress rehearsal fueling test, loading more than 700,000 gallons (2.65 million liters) of cryogenic liquid hydrogen and oxygen into the two-stage SLS on Pad 39B; teams paused LH2 loading twice to address small leaks at a tail service mast umbilical (TSMU) interface but quickly troubleshot and topped off the tanks. The wet dress remains underway with a Feb. 8 target launch for a 10-day crewed lunar flyby carrying four astronauts, making final confirmation contingent on completion of the test and favorable weather. For investors, the test represents incremental technical progress for NASA and its industrial contractors, while the recurring LH2 leak risk highlights residual schedule and programmatic uncertainty.

Market structure: A successful Artemis wet dress keeps incumbents — Boeing (BA), Lockheed Martin (LMT), Northrop Grumman (NOC), Aerojet Rocketdyne (AJRD) and Raytheon/RTX (RTX) — in prime position for sustained NASA contract flow; consider these as the direct beneficiaries while speculative small-cap commercial launchers (e.g., SPCE) face relative headwinds if political funding locks to SLS. Cryogenic LH2 leak issues highlight recurring O&M and hardware upgrade demand (valves, seals, cryogenics) which favors industrial suppliers (Parker PH, Linde LIN) and raises short-term aftermarket spend rather than shifting pricing power materially. Cross-asset: expect modest risk-on in aerospace equities, potential tightening of corporate spreads for large primes (bps-level), negligible FX impact, and no immediate commodity shock from LH2 volumes. Risk assessment: Tail risks include a scrub or in-flight anomaly leading to a 15–40% drawdown in small/mid-cap space names and 5–20% weakness in primes if program review/contract freezes occur; regulatory/safety inquiries could impose multi-quarter schedule risk. Time horizons: immediate (48–72 hours around Feb 3 briefing + Feb 8 launch); short-term (weeks–months for sentiment and order flow); long-term (2–5 years for program funding vs. commercial competition). Hidden dependencies: single-source suppliers, Congressional appropriations and SpaceX Starship progress are second-order determiners. Catalysts: Feb 3 press briefing, Feb 8 launch attempt, NASA Inspector General reports and FY2026 appropriations cycle. Trade implications: Tactical direct plays: establish 2–3% long positions in LMT and RTX on expectation of contract stability and defense allocation, add 1% long AJRD for leverage to propulsion wins with a 3-month +30% OTM call spread to cap premium. Pair trade: long LMT (2%) vs short SPCE (1%) to express incumbent vs speculative exposure; hedge portfolio tail risk with a 6–10 week put on XAR sized to 0.5–1% notional. Entry/exit: enter pre-press briefing or within 48 hours after a confirmed wet-dress success; trim 30% on +10% moves, stop-loss at -8% per position. Contrarian angles: Consensus may underprice sustained political support for SLS — a clean crewed Artemis 2 increases procurement stickiness and could lift primes’ backlog by several percent annually, an underappreciated multi-year upside. Conversely the market underestimates Starship’s threat: a successful Starship lunar demonstration within 18–36 months would materially re-rate long-duration SLS cash flows downward, so position sizing should reflect asymmetric obsolescence risk. Historical analog: Artemis-1 delays then technical success produced gradual, not immediate, equity appreciation; expect similar slow recognition here. Unintended consequence: a crewed success could shift funds away from commercial lunar LLM companies, pressuring their valuations despite overall sector hype.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25