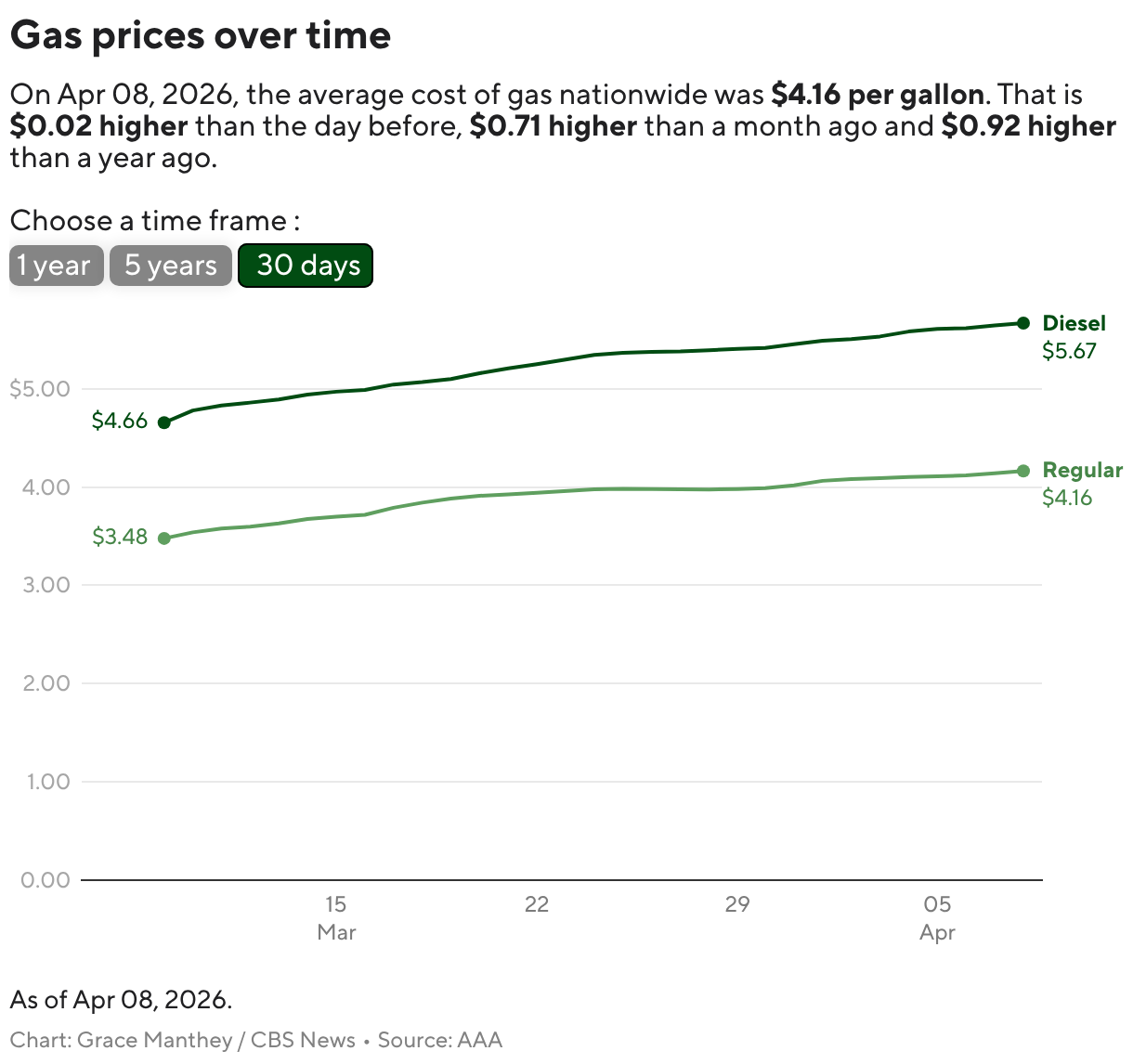

An eleventh-hour U.S.-Iran ceasefire has eased tensions and helped global crude fall below $95/bbl; the U.S. national average for regular gasoline is $4.16/gal (up from $2.98 pre-conflict) and diesel averages $5.67/gal. Analysts (GasBuddy, Oxford Economics, Moody's) say pump prices could drop by a few cents immediately and potentially fall below $4/gal within a couple of weeks if the ceasefire holds; Moody's Mark Zandi projects ~$3.75/gal if oil stabilizes around $90/bbl and ~$3.50/gal by year-end if oil drops to ~$80/bbl. Significant downside risk persists—reports of Strait of Hormuz disruptions and the possibility the deal unravels could quickly reverse any price declines.

The market's immediate normalization of headline risk will shave the crisis risk premium from crude very quickly, but retail gasoline is several mechanical steps removed from that move — refinery runs, wholesale gasoline inventories, and rack-to-retail distribution lags dominate timing. Expect meaningful retail relief only after two operational cycles: one to mop up elevated wholesale prices in rack markets and a second to transmit lower refinery crack spreads into convenience-store pricing; that cascades over weeks, not days. Winners in a sustained de-escalation are domestic refiners with flexible feedstock hubs and export capability (they capture incremental crack expansion), coastal storage/terminal operators that can reposition barrels for Atlantic arbitrage, and regional convenience chains that can flex gross margin. Losers on a durable calm include tanker owners (shorter tanker rates if Strait traffic resumes), oil-risk insurance providers, and any merchant exporters who had benefited from wide basis differentials during the flare-up. Tail risk remains asymmetrical: a re-escalation through the Strait of Hormuz would re-inflate risk premia within 48–72 hours, compress supplies to key refining hubs and spike inland gasoline basis differentials; conversely, a sustained diplomatic détente combined with modest SPR releases or OPEC incremental crude could see Brent settle back toward structural mid-cycle levels over 3–6 months. The consensus is underestimating at-the-pump frictions and overestimating how quickly headline calm converts into consumer relief; position sizing should reflect a short-dated headline risk and a longer-dated operational risk window.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.05