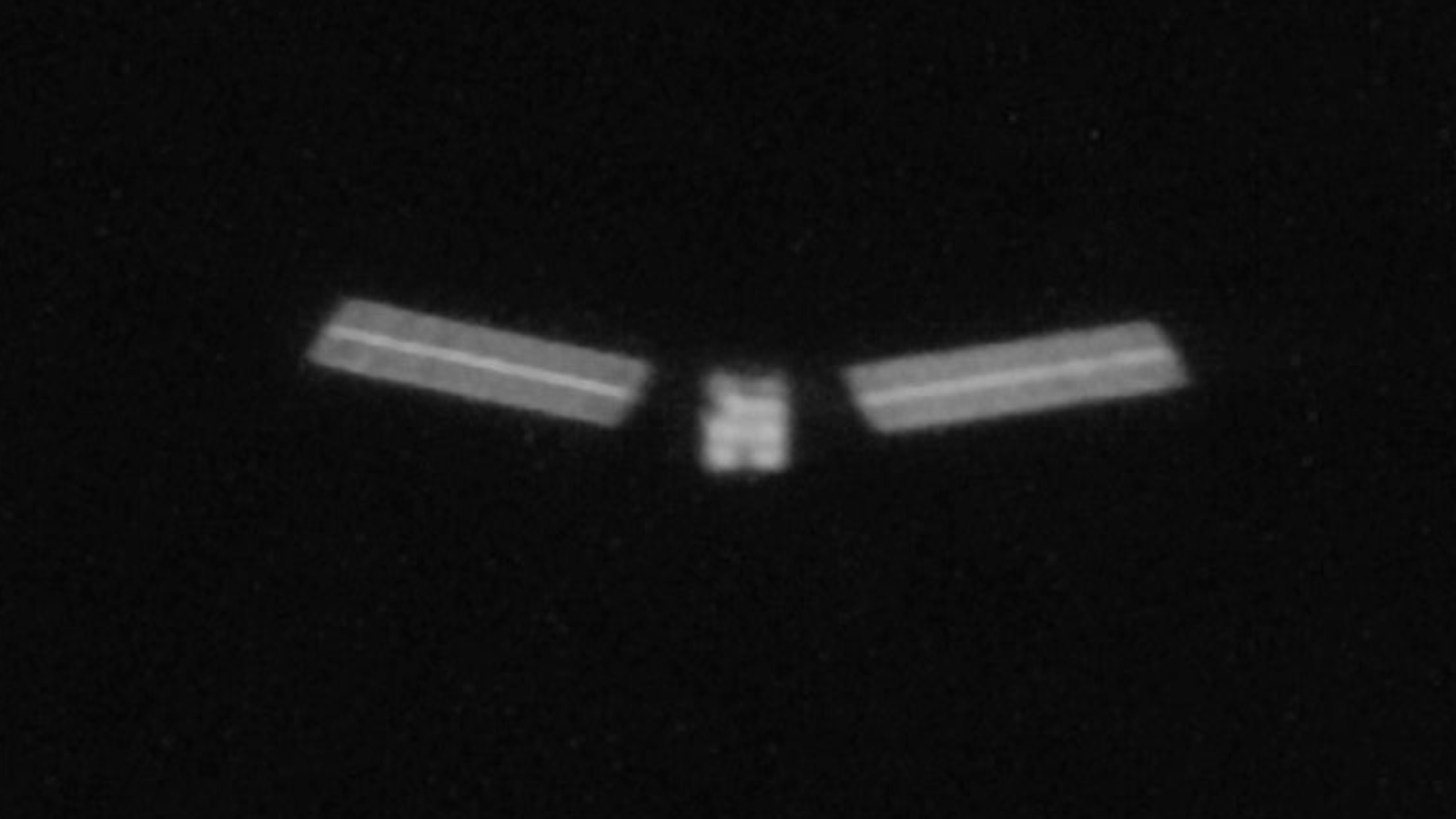

Starlink satellite 34343 experienced a fragmentation event on March 29, 2026 at ~560 km altitude, resulting in loss of communications; SpaceX says analysis shows no new risk to the ISS, its crew, or NASA’s Artemis II and is coordinating with NASA and the US Space Force. The event posed no new risk to the Transporter-16 mission; SpaceX and Starlink teams are monitoring trackable debris and investigating the root cause. HEO Robotics imaged the satellite on Feb. 14, 2026 and is attempting to image its current state. Market impact is minimal but monitor for any operational or regulatory follow-ups that could affect launch scheduling.

The operational and economic externalities from on-orbit fragmentation disproportionately penalize low-margin constellation operators and raise the marginal cost of running LEO networks. Increased collision-avoidance burns and more frequent replacement launches translate into a meaningful rise in OPEX and capex for fleets that optimized for low-cost, short-lived units; model a 1–3% annual incremental propellant burn per satellite and a 10–20% rise in replacement cadence over the next 12–24 months for vulnerable architectures. Regulatory and insurance markets will respond faster than hardware cycles: expect accelerated SSA (space situational awareness) contracting, tighter licensing conditions for mass-deploy constellations, and a near-term re-pricing of launch/satellite insurance. Insurers will likely widen premiums and reduce capacity for higher debris-risk orbital bands, compressing economics for smaller entrants and increasing working capital needs as pre-launch insurance becomes costlier by an estimated 20–50% for marginal programs. The easiest, underpriced lever is sensing and remediation: governments and primes will fund telescopes, RF/optical trackers, and maneuverable tug/propulsion retrofits on 6–18 month timelines, creating an asymmetric opportunity for SSA-capable primes and launch providers with flexible manifest capacity. The tail risk is a cascade (Kessler-like) that would materially disrupt LEO operations — low probability but multi-year impact — which makes optionality (long calls on SSA/defense names, insured upside exposure) more attractive than outright leveraged long on constellation equities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00