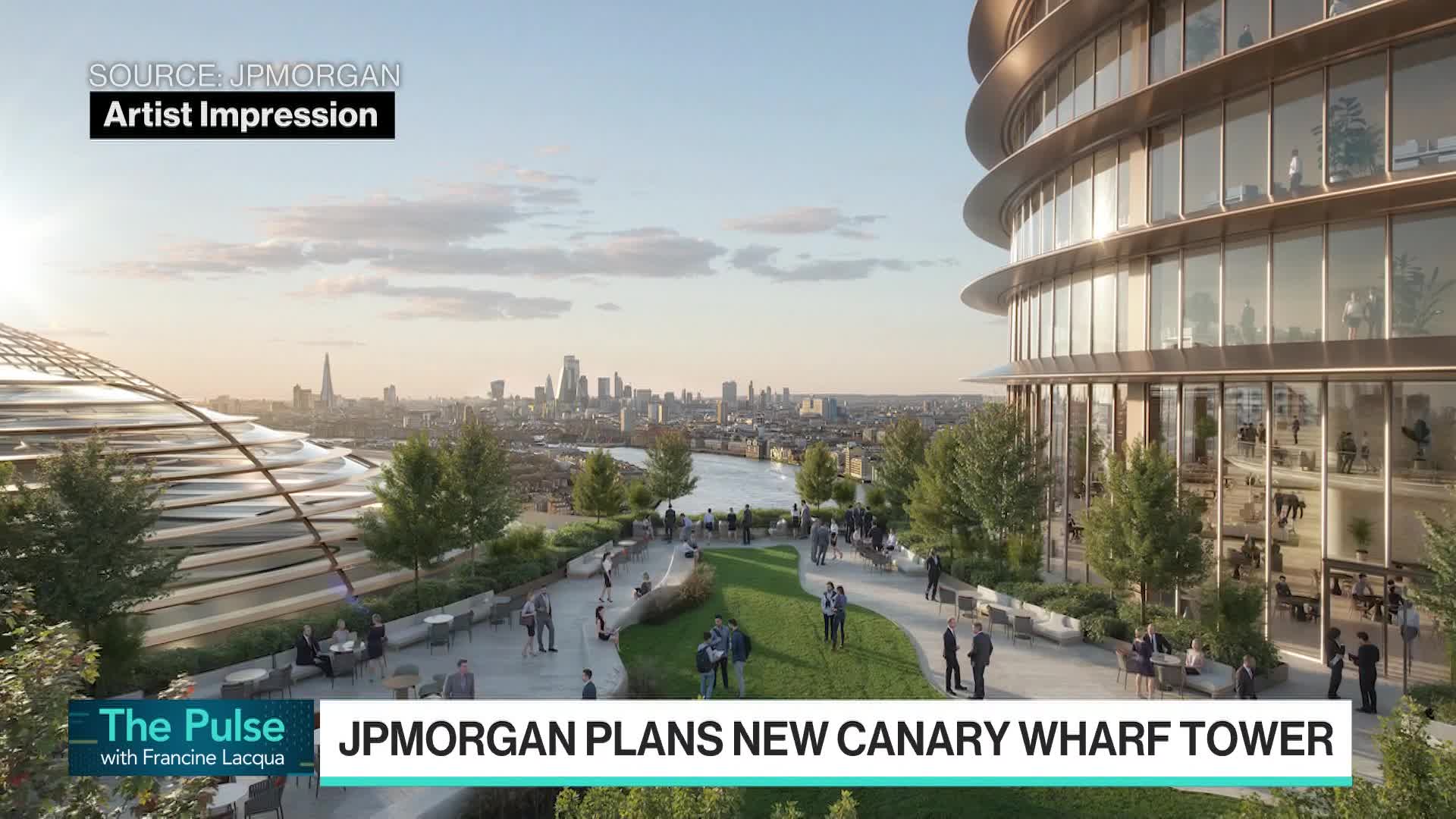

J.P. Morgan has announced plans to establish its principal UK headquarters in Canary Wharf, proposing a new development that would house up to 12,000 workers and is expected to contribute nearly £10 billion to the local economy over six years. The project — described as likely London's largest office building and a multi-year build (around six years) — signals a major corporate commitment to Canary Wharf and highlights the scarcity of large, modern office stock in London, with potential upside for local commercial real estate activity and adjacent retail and hospitality revenue streams.

Market structure: JPMorgan’s decision materially tightens demand for trophy-grade large-floorplate offices in London and signals renewed corporate appetite to cluster in Canary Wharf. Winners: owners/operators of prime London commercial real estate and large-cap construction contractors; losers: small regional office REITs and lower-grade retail landlords that compete for tenant capex. Expect a 5–15% relative rerating over 12–24 months for prime-office landlords if this crystallises into more large leases. Risk assessment: Tail risks include planning/cost overruns, a UK political change that withdraws incentives, or a sharp rate shock pushing cap rates wider — any of which could erase >30% of expected NAV gains. Immediate effects (days) will be local positive sentiment; short-term (3–6 months) depends on contract awards and financing; long-term (3–6 years) is rental growth and re-pricing of prime stock. Hidden dependencies: construction capacity, skilled labour bottlenecks, and ESG/operational decarbonisation costs that can inflate capex by 10–25%. Trade implications: Tilt into UK prime-office landlords and contractors while underweight retail and secondary office landlords. Use concentrated, time-boxed exposures (6–24 months) and defined-risk option structures to capture upside from re-rating while protecting against funding/permits delays. Expect modest FX/gilt implications: GBP could firm 0.5–1.5% and 5–10bp compression in gilts tied to improved confidence, but these are second-order and fragile. Contrarian angles: Consensus treats this as uniformly bullish for London real estate; missing is the risk that scarcity boosts rents only for very large, modern floorplates while accelerating vacancy and discounting for small/old stock — a bifurcation opportunity. Also, construction cost inflation and higher-for-longer rates could compress developer IRRs, so long positions should be sized and hedged; historical parallels (post-2008 trophy asset flight-to-quality) show sharp bifurcation over 12–36 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45