The article highlights a divergence in outlook for Rio Tinto (RIO), with its Average Brokerage Recommendation (ABR) of 1.80, approximating a 'Strong Buy,' contrasting sharply with a Zacks Rank #4 (Sell). This discrepancy stems from a 1.5% decline in RIO's current year consensus EPS estimate to $6.01 over the past month, indicating growing analyst pessimism. The piece argues that ABRs often carry a positive bias and are less reliable than the Zacks Rank, a quantitative model based on timely earnings estimate revisions, suggesting investors should view the optimistic brokerage ratings with caution given the potential for near-term price pressure on RIO.

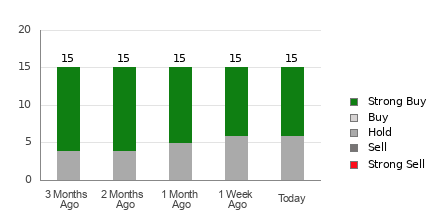

A notable divergence in analyst sentiment exists for Rio Tinto (RIO), creating a conflicting picture for investors. On one hand, the consensus view from sell-side analysts is firmly positive, reflected in an Average Brokerage Recommendation (ABR) of 1.80, which sits between a 'Buy' and 'Strong Buy'. This is supported by nine of the 15 contributing firms issuing 'Strong Buy' ratings. However, this optimism is directly challenged by a more cautionary quantitative signal. The Zacks Consensus Estimate for RIO's current-year earnings per share has been revised downward by 1.5% over the past month to $6.01. This negative revision, indicating growing pessimism about the company's near-term earnings power, has resulted in a Zacks Rank of #4 (Sell). The core of this analysis suggests that earnings estimate revisions are a more timely and empirically correlated predictor of future stock performance than potentially biased brokerage recommendations, implying that the recent negative trend in estimates poses a material risk for near-term price depreciation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40

Ticker Sentiment