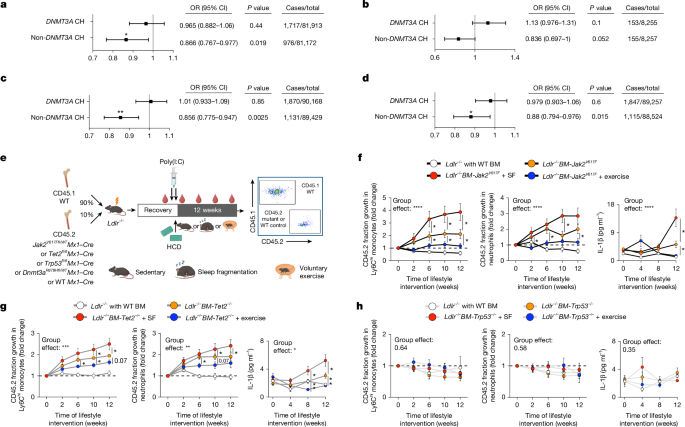

The study finds that moderate-to-vigorous physical activity and uninterrupted sleep can reduce clonal hematopoiesis clone expansion and atherosclerosis in mutation-specific ways, especially for Jak2V617F and Tet2 loss-of-function, but not Dnmt3aR878H. In humans, higher physical activity was associated with lower prevalence of non-DNMT3A-driven clonal hematopoiesis. The work is scientifically positive for cardiovascular risk understanding, but it is early-stage and unlikely to have immediate market impact.

This reads as a precision medicine signal, not a broad “wellness” trade. The marketable implication is that CH is increasingly likely to bifurcate into mutation-specific risk buckets, which matters because the economically important downstream endpoint is not clone size alone but inflammatory plaque activity. That favors companies with exposure to IL-1, innate immune, and myeloid-inflammatory pathways, but only if they can show mutation-enriched responder populations; otherwise the clinical noise floor remains high. The second-order effect is that sleep/exercise may become confounders in CH and ASCVD trials, especially those enriched for JAK2/TET2/TP53 carriers. That raises the bar for endpoints and patient stratification across cardiometabolic and hematology programs, and it could slow unstratified readouts for broad anti-inflammatory agents while improving the odds of success for therapies that intercept IL-1β/innate sensing or adrenergic signaling in macrophages. Dnmt3a appears comparatively resistant, which is a reminder that “clonal hematopoiesis” is not a single biology and that basket-style CH trials risk diluting effect sizes. Contrarian takeaway: the biggest near-term market misread is probably assuming this is a lifestyle-only story. The real monetizable angle is biomarker-guided selection, because mutation-specific sensitivity creates a path to higher absolute risk reduction in a subset that is already overrepresented in atherosclerotic cohorts. Over 6-24 months, this should increase attention to companion diagnostics for CH genotyping, but it also means any company betting on a one-size-fits-all anti-inflammatory label expansion may be overearning current optimism. For public equities, the read-through is modestly positive for names with credible inflammation franchises and diagnostics leverage, but not enough to justify a wholesale rerating absent human interventional data. In the nearer term, expect incremental support for sleep/exercise-adjacent consumer health and wearables demand, yet the more durable effect is likely in trial design rather than end-market revenue. The risk is that the biology proves hard to translate outside high-inflammatory, mutation-enriched populations, which would compress the commercial opportunity back to niche precision-medicine use cases.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment