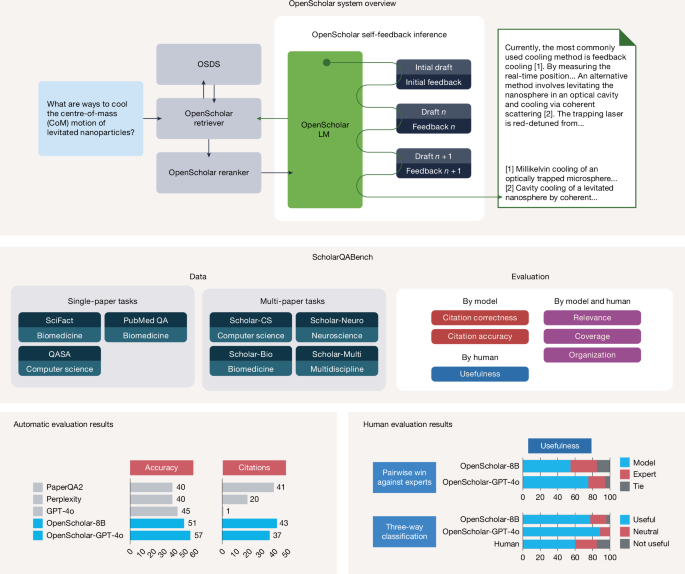

OpenScholar is a new open-source, retrieval-augmented language model and pipeline built on an OpenScholar DataStore of 45 million papers (236 million passage embeddings) that produces citation-backed literature syntheses. In benchmark and expert evaluations OpenScholar-8B outperforms GPT-4o by ~6.1% and PaperQA2 by ~5.5% on multi-paper synthesis tasks, OpenScholar-GPT-4o improves GPT-4o correctness by ~12%, and the system achieves win rates of ~70% (GPT-4o backend) and ~51% (8B) versus expert-written answers while markedly reducing hallucinated citations (GPT-4o alone fabricated 78–90% of cited titles). The team open-sourced code, models and data, launched a public demo that has handled >30,000 users and ~90,000 queries, and reports substantially lower retrieval costs than comparable proprietary pipelines.

Market structure: OpenScholar materially raises the competitiveness of open-source, retrieval-augmented LLM stacks (45M-paper datastore, demonstrable parity with proprietary outputs). Winners are infra and model hosts (cloud providers, GPU suppliers) and firms leveraging faster literature synthesis (biotech R&D, AI product teams); losers are margin-dependent proprietary-API businesses if usage shifts to self-hosted stacks. Expect downward pressure on per-query API pricing over 12–24 months and upward demand for datacenter GPUs (implied +10–30% annualized demand for inference/embedding capacity). Risk assessment: Tail risks include regulatory/copyright rulings (EU/US) that could restrict open-access corpora or raise licensing costs, and clinical-liability from hallucinations in healthcare—these could cause sharp repricings if rulings occur within 90–180 days. Short-term (days–weeks) impact is adoption noise (demo: 30k users, 90k queries), medium-term (3–12 months) is enterprise proof-of-concept & procurement cycles, and long-term (1–3 years) is structural margin compression for API incumbents. Hidden dependencies: many “open” deployments still rely on proprietary LMs (OpenScholar-GPT-4o), so vendor risk persists until full-stack open parity is proven. Trade implications: Favor equities with direct exposure to GPU/datacenter demand (semis/cloud) and platform owners of open LLM ecosystems (Meta), while hedging pure-play API/margin models. Use defined-risk options to express acceleration in GPU demand and covered-income structures on large-cap cloud names to monetize steady cashflows. Rebalance a portion of biotech exposure higher (R&D productivity beneficiaries) while protecting against regulatory headline shocks with short-dated hedges. Contrarian angles: Consensus underestimates the speed at which open stacks reduce variable API spend—if organizations save 20–40% of AI OPEX, adoption could accelerate beyond current forecasts, benefiting Meta/OSS ecosystems and NVDA more than MSFT’s API-linked upside. Conversely, the market may be underpricing legal/regulatory risk; a single major publisher injunction could force index retraining costs +10–25% and pause enterprise rollouts. Historical parallel: open-source Linux vs. proprietary UNIX—initially seen as niche, then dominant; if governance & licensing are solved, expect similar structural shifts over 2–5 years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment