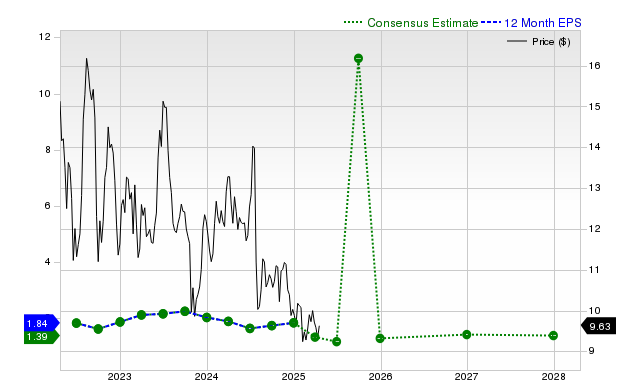

Zacks highlights mixed signals for Ford Motor: consensus EPS for the current quarter is $0.10 (-74.4% YoY) with the 30-day consensus down 22.7%, fiscal-year EPS of $1.07 (-41.9%) and a rebound to $1.40 forecast for next fiscal year (+30.1%). Revenue consensus for the current quarter is $40.67bn (-9.4%), while last reported quarter revenue was $47.19bn (+9.6%) and EPS was $0.45, each topping Zacks consensus (revenue surprise +10.6%, EPS surprise +18.4%). Zacks assigns Ford a Rank #3 (Hold) and a Value Style Score of A, signaling modest investor interest driven by valuation despite near-term earnings weakness.

Market structure: Ford’s near-term estimate shock (consensus qtr EPS -74.4%, 30-day revision -22.7%) favors short-duration players and value buyers. Direct winners: long-biased value funds and suppliers locked into long contracts; losers: leveraged retail-finance exposure and small-cap auto suppliers facing order pull-ins. Expect option IV and short-term credit spreads for auto names to widen ~10–50bps on earnings misses, while commodity demand (steel/aluminum) softens modestly if production is trimmed. Risk assessment: Tail risks include a sharper consumer credit squeeze that raises delinquencies in Ford Credit, large recall/EV battery event, or macro recession driving unit sales down >10% YoY — any would drop EPS materially beyond current cuts. Immediate (days) risk is earnings-driven volatility; short-term (weeks/months) hinges on dealer inventories and guidance; long-term (quarters/years) depends on EV margin conversion and captive finance health. Hidden dependencies: pension cash flows, supplier solvency, and incentives on retail pricing. Trade implications: Near-term trade is event-driven — avoid unhedged large longs into the next print; buy-the-dip longer-dated exposure if fundamentals hold. Use LEAP calls to capture the +30% next-year EPS thesis while selling short-dated calls to finance carry; implement 0.5–1.0% pair trades long F vs short GM to exploit relative valuation and surprise history. Rotate 2–4% from cyclicals into defensive staples if retail auto sales soften >5% over two consecutive months. Contrarian angles: Consensus focuses on near-term pain but may underprice recovery: FY+1 consensus EPS +30.1% to $1.40 implies 2026 upside if supply normalizes. Historical parallels (post-cycle auto recoveries) show strong incumbents rerating quickly once guidance improves; mispricing risk: if Ford Credit outperforms or revenue surprises recur, implied vols will compress and shares can gap +15–30% rapidly. Conversely, crowded buy-on-dip positioning could exacerbate losses if a credit or recall shock hits.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

-0.15

Ticker Sentiment