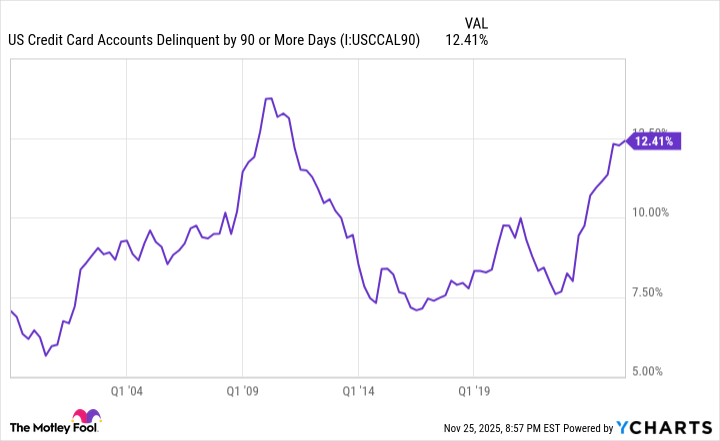

Major U.S. equity indexes have hit record highs on AI excitement and expectations of Fed rate easing, but several credit indicators show growing stress: CMBS delinquencies reached 11.76% (Oct 2025), subprime auto 60+ delinquencies hit 6.65% (Oct 2025) with outstanding auto debt at $1.66 trillion (end Sept), and credit card 90+ day delinquencies rose to 12.41% in Q3 2025 amid record >$1.2 trillion card balances. These trends point to weakening consumer and commercial real estate fundamentals that could undercut the market rally if delinquencies and related credit losses accelerate, warranting a cautious, risk-off stance for portfolio managers.

Market structure: AI hardware/software leaders (NVDA, MSFT, GOOGL, AMD) continue to capture revenue share as capex for model training and inference ramps; expect 15–30% revenue leverage for dominant GPU/AI-stack firms over next 12 months. Losers are concentrated: office-heavy CRE and leveraged subprime consumer lenders (regional banks, auto and credit-card-focused issuers) face rising delinquencies and funding costs that compress NIMs and push cap rates wider, pressuring REIT and bank equity valuations. Risk assessment: Tail risks include a CMBS-triggered regional banking stress or a correlated widening of ABS/HY spreads that forces capital raises (5–15% probability over 12 months) with >30% downside to exposed equities. Near-term (days–weeks) volatility will cluster around Fed minutes, bank earnings and quarterly CMBS/Fitch updates; medium-term (3–12 months) risks are driven by unemployment and consumer credit trends; long-term (12–24 months) a mild recession could materialize if delinquencies continue climbing. Trade implications: Favor concentrated long exposure to AI/semiconductor leaders with protective hedges while buying insurance against credit widening: implement 2–3% longs in NVDA/MSFT for 6–12 months, offset with 3–6 month put spreads on VNQ and KRE to hedge CRE/bank downside. Rotate 3–5% into U.S. Treasuries (IEF) as convex hedge if spreads blow out; use pair trades (long NVDA, short VNQ) to keep market beta neutral. Contrarian angles: Consensus underestimates Fed/FDIC willingness to backstop localized bank stress which would compress downside on shorts—short squeezes are possible if regulators act quickly. Conversely, industrial/logistics REITs (PLD) and high-quality multifamily may be oversold; selective 1–2% buys here could outperform if capital markets stay open. Historical parallels (1990s tech spikes amid localized credit stress) suggest asymmetric reward to concentrated innovation bets plus disciplined hedging.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45