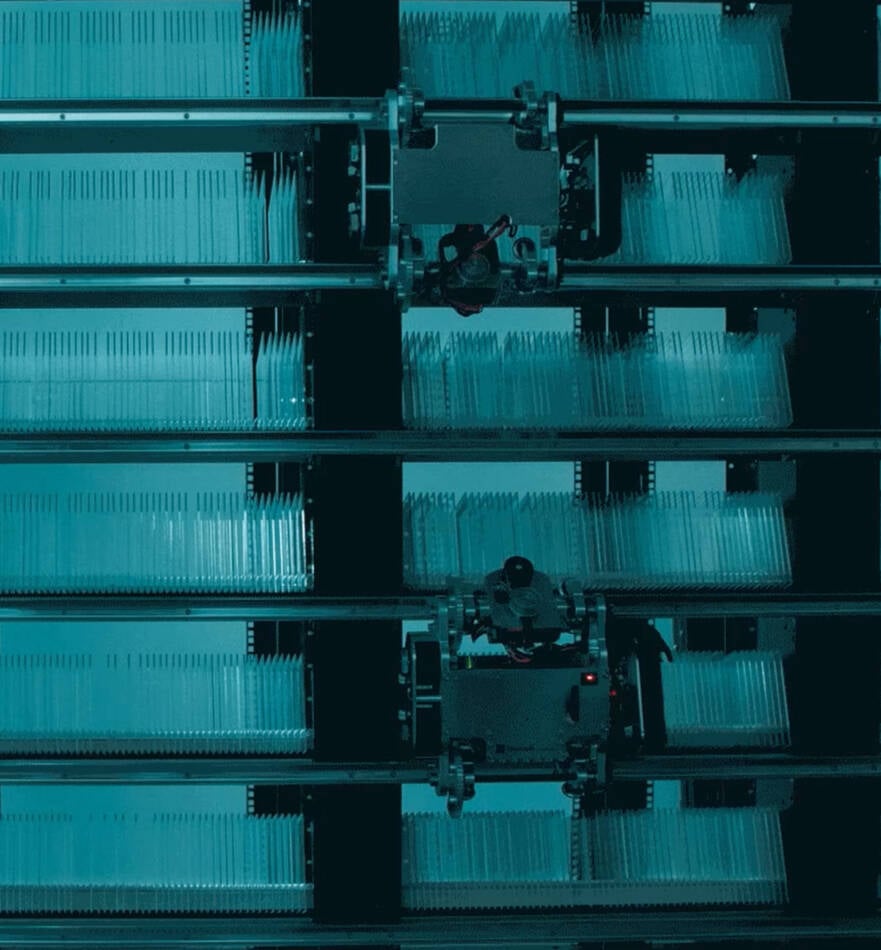

Microsoft's Project Silica researchers demonstrated archival data encoding in 2 mm borosilicate (Pyrex) glass, etching 258 layers totaling ~2.02 TB per plate with write speeds of 18.4–65.9 Mbps (1–4 beams) and a reported viable storage life extrapolated to over 10,000 years. The team moved from birefringent to phase-based voxels (single laser pulse) and increased parallel voxel writes, trading roughly half the density of fused silica (2.02 TB vs. 4.84 TB) for higher top write speed and lower cost; machine-learning models mitigate voxel interference. The research phase is described as complete, Microsoft retains IP and is considering productization options, but no commercial roadmap or timeline was announced.

Market structure: Microsoft (MSFT) gains valuable long-duration IP optionality — the research lowers cost barriers vs fused silica (2.02 TB @ 2 mm vs 4.84 TB) and boosts write speed (18.4–65.9 Mbps vs 25.6 Mbps), favoring cloud archival use-cases over 3–7 year adoption cycles. Winners include MSFT (licensing/enterprise), photonics/laser OEMs (IIVI, LITE, COHR) and niche archival service integrators; incumbents in tape/HDD cold-storage (STX, IRM) face gradual pricing pressure if commercial scale is proven. Cross-asset impact is modest now: expect ID-specific equity re-rating, asymmetric option flows on MSFT and suppliers, but negligible immediate FX or commodity moves unless silica supply or specialized optics bottlenecks emerge. Risk assessment: Key tail risks are non-productization (MSFT deprioritizes commercial launch), unresolved reader standardization, ML-based read errors causing correlated data loss, or IP/legal challenges — any of which could wipe optionality value. Time horizons: days—limited stock reaction; weeks–months—sentiment around partnerships or patents; years—real market disruption if scale and read ecosystem materialize (3–7+ years). Hidden dependencies include reader/write hardware supply, archival indexing/metadata standards, and regulatory issues over immutable data storage. Trade implications: Tactical alpha lies in owning MSFT optionality and photonics suppliers while hedging legacy-storage exposure. Direct plays: small-long MSFT (1–2%) and 2–3% combined exposure to IIVI/LITE/COHR over 3–12 months, scale on >5% pullbacks. Pair: long MSFT vs short STX or IRM (0.5–1% notional) to capture relative secular rotation; option strategy: 12–18 month MSFT call spreads to cap cost and capture commercialization events. Entry on news-driven buy triggers (supplier partnerships, DoD/cultural contracts) and exit on clear productization or 15–25% move. Contrarian angles: Consensus underestimates ecosystem friction — read-back standardization and liability for “permanent” data could delay adoption, so pure tape displacement is unlikely before 5+ years. The market may be underpricing vendors of lasers/ML tooling (short time-to-revenue) and overpricing immediate risk to IRM/STX. Historical parallels (M-Disc, holographic storage) show archival tech can be technologically superior yet commercially niche; unintended consequences include regulatory/legal pushback on immutable archives and key-management risks that could create new service-adjacent opportunities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28

Ticker Sentiment