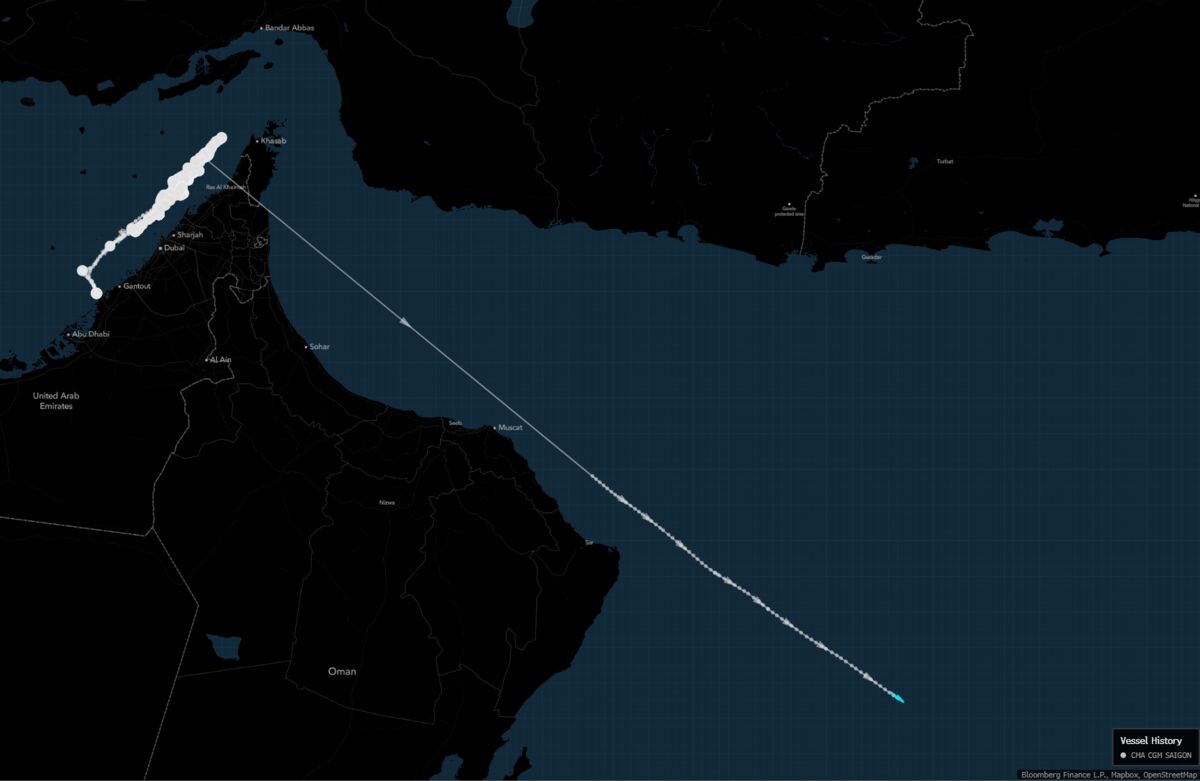

The French container ship CMA CGM Saigon was tracked making a rare crossing of the Strait of Hormuz and reappeared off Oman en route to Colombo, Sri Lanka. The movement is notable as an unusual passage by a Western European vessel through a geopolitically sensitive chokepoint, but the article reports no disruption, damage, or direct market reaction. The main relevance is to shipping routes and regional risk monitoring rather than an immediate price-moving event.

This is less about one ship and more about the signaling value of route choice under elevated maritime risk. A Western European carrier transiting the Strait of Hormuz, even with a small vessel, suggests commercial actors may be testing whether the risk premium on Gulf-to-Asia lanes is overstated or whether security normalization is beginning to price in. The second-order effect is that if insurers, charterers, and operators infer a lower-than-feared probability of interdiction, spot freight and war-risk premia can mean-revert quickly, especially on non-energy lanes where rerouting costs are a larger share of voyage economics.

The market implication is asymmetric for logistics equities with Asia exposure and weak pricing power: if Gulf transits normalize, rivals that have benefited from avoidance-routing can lose incremental days-on-water pricing. Conversely, carriers with diversified networks and stronger yield management can preserve margins by arbitraging capacity across regions. The bigger risk is not an immediate move in freight rates, but a slow bleed in risk premium embedded in forward contracts and insurance, which could unwind over weeks rather than days if no incident follows.

The contrarian read is that one crossing does not validate a durable safe-passage regime; it may simply reflect a single ship’s cargo urgency or insurer-specific tolerance. Consensus may be overestimating the persistence of headline risk while underestimating how quickly a single incident would reflate costs. That creates a low-probability, high-impact setup where the best trade is often to buy optionality rather than express a large directional view outright.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05