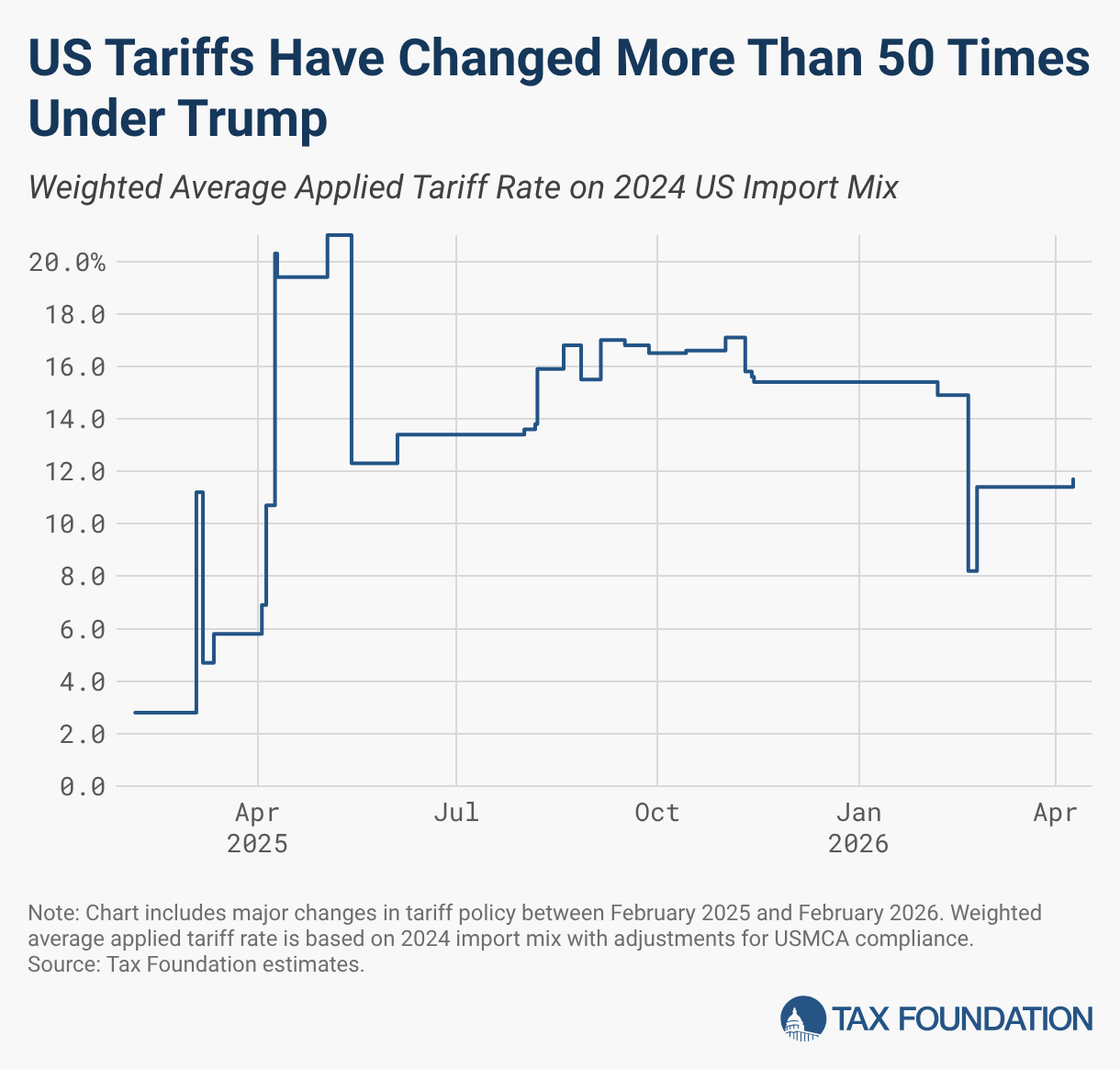

Tariff actions generated $264 billion in customs duties in 2025 (≈4.9% of tax receipts) and roughly $166 billion from IEEPA tariffs before the Supreme Court struck down that authority; applied US tariff rates peaked at 21.5% and fell to 13.6% by end-2025. FDI totaled $288.4 billion in 2025 (below the 10-year average of $320.7 billion), manufacturing employment fell by 89,000 between Apr 2025 and Feb 2026, and tariff pass-through to retail prices reached ~24%, contributing ~0.76 percentage points to CPI—evidence the tariffs failed to deliver promised investment, jobs, or debt reduction and instead raised prices and weighed on activity.

The visible policy churn has produced an underappreciated wedge between headline investment intentions and the marginal economics of new projects: companies facing higher and uncertain trade frictions are raising their internal hurdle rates by an estimated 150–300bps, which disproportionately kills long-cycle capex (semiconductor fabs, chemical plants) while leaving short-cycle, asset-light services largely unscathed. That dynamic favors firms with near-term free cash flow and flexible sourcing over highly leveraged industrial builders; expect valuation multiple dispersion to widen between the two over 6–18 months. A second-order beneficiary set is the near-shore manufacturing nodes and logistics firms that enable rapid switching — think Mexico and Southeast Asian supply-chain enablers — which gain pricing power as lead times and retooling costs rise. Container and intermodal demand volatility will compress global freight margins but create idiosyncratic winners among third-party logistics providers with scale and dual-hub footprints; monitor companies with >40% exposed volumes to Mexico/SE Asia for outsized margin expansion. Monetary and fiscal interactions are the overlooked transmission mechanism: policy-induced price shocks that persist will keep real rates higher for longer, compressing equity multiples and re-pricing long-duration growth stocks. The principal catalyst to reverse this regime is political/legal stabilization of trade authorities or a rapid, credible rollback of tariffs — absent that, prepare for a multi-quarter premium on risk-free rates and elevated realized volatility across cyclical names.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly negative

Sentiment Score

-0.65